Chapter 23 Answers

Chapter 23 Answers

Download as pdf or txt

You might also like

- Electricity Bill June 2023Document2 pagesElectricity Bill June 2023Eric CartmanNo ratings yet

- ASAL Business CB Chapter 21 AnswersDocument7 pagesASAL Business CB Chapter 21 AnswersDewald Alberts100% (1)

- Bill of Lading No.: Mediterranean Shipping Company S.ADocument1 pageBill of Lading No.: Mediterranean Shipping Company S.Aaliaga14No ratings yet

- Introduction To Books of Prime Entry and LedgersDocument12 pagesIntroduction To Books of Prime Entry and Ledgersdianime OtakuNo ratings yet

- Caie Igcse Business Studies 0450 Definitions v1Document8 pagesCaie Igcse Business Studies 0450 Definitions v1Ashley Kyaw100% (1)

- Caie A2 Level Business 9609 Model Answers v1Document12 pagesCaie A2 Level Business 9609 Model Answers v1Jude ChamindaNo ratings yet

- Chapter 10 AnswersDocument3 pagesChapter 10 AnswersThe Nightwatchmen100% (1)

- As Eco Guess Paper-2Document2 pagesAs Eco Guess Paper-2QamarBalochNo ratings yet

- Exam Style Questions Page 266Document2 pagesExam Style Questions Page 266Arounny Corwin100% (2)

- 4AC1 02 Que 20210505Document12 pages4AC1 02 Que 20210505Abdul WahabNo ratings yet

- Cambridge International AS & A Level: Economics 9708/12Document3 pagesCambridge International AS & A Level: Economics 9708/12faiq khan vlogsNo ratings yet

- Cambridge International As - A Level Accounting Executive PreviewDocument63 pagesCambridge International As - A Level Accounting Executive PreviewivanNo ratings yet

- 9706 - m24 - QP - 32 - Acc p3 Feb March 24Document12 pages9706 - m24 - QP - 32 - Acc p3 Feb March 24Shaamikh Rilwan100% (1)

- Capacity Utilisation and OutsourcingDocument3 pagesCapacity Utilisation and OutsourcingJared OtienoNo ratings yet

- Pdfcaie Igcse Accounting 0452 Theory v2 PDFDocument24 pagesPdfcaie Igcse Accounting 0452 Theory v2 PDFrumaisaaltaf287No ratings yet

- 0450 - 1.3 Enterprise, Business Growth and SizeDocument15 pages0450 - 1.3 Enterprise, Business Growth and SizeCheryl100% (2)

- Cambridge Assessment International Education: Business 9609/13 May/June 2019Document12 pagesCambridge Assessment International Education: Business 9609/13 May/June 2019AbdulBasitBilalSheikhNo ratings yet

- 9708 2023Document6 pages9708 2023Jenney TatNo ratings yet

- Week 5 AS 11gr HomeworkDocument4 pagesWeek 5 AS 11gr Homeworkaisaverdieva04No ratings yet

- 6.1 International Trade and Specialization: Igcse /O Level EconomicsDocument10 pages6.1 International Trade and Specialization: Igcse /O Level EconomicsAvely AntoniusNo ratings yet

- FebMarch 2021 AnswersDocument20 pagesFebMarch 2021 AnswersRania GamalNo ratings yet

- Stephen - Business Studies Exam Style Question 1 Page 196Document1 pageStephen - Business Studies Exam Style Question 1 Page 196api-348960952No ratings yet

- 0455 Example Candidate 0455-Responses For Examination From 2014Document79 pages0455 Example Candidate 0455-Responses For Examination From 2014Mohamed Tarek100% (1)

- 0 - Business 9609 A2 NotesDocument84 pages0 - Business 9609 A2 Notesiman100% (1)

- Worksheet 1.3 Introducing Trail BalancesDocument3 pagesWorksheet 1.3 Introducing Trail Balancesaysilislam528No ratings yet

- IGCSE Business Studies Essential Book Answers For Unit 5Document6 pagesIGCSE Business Studies Essential Book Answers For Unit 5emonimtiazNo ratings yet

- IGCSE-OL - Bus - CH - 23 - Answers To CB ActivitiesDocument4 pagesIGCSE-OL - Bus - CH - 23 - Answers To CB ActivitiesOscar WilliamsNo ratings yet

- Cambridge International AS & A Level: ECONOMICS 9708/01Document14 pagesCambridge International AS & A Level: ECONOMICS 9708/01bhabi 03No ratings yet

- Cambridge International AS & A Level: Economics 9708/12Document12 pagesCambridge International AS & A Level: Economics 9708/12faiq khan vlogsNo ratings yet

- AS Level Economics Paper-2 (Qamar Baloch)Document2 pagesAS Level Economics Paper-2 (Qamar Baloch)Sarmad ShafiqueNo ratings yet

- Cambridge International AS & A Level: AccountingDocument17 pagesCambridge International AS & A Level: AccountingTehreem FatimaNo ratings yet

- Cambridge International General Certificate of Secondary EducationDocument15 pagesCambridge International General Certificate of Secondary Education1932godfreyNo ratings yet

- Caie A2 Level Business 9609 Definitions v1Document8 pagesCaie A2 Level Business 9609 Definitions v1Jude ChamindaNo ratings yet

- 1.1 - Business Activity - IGCSE AIDDocument1 page1.1 - Business Activity - IGCSE AIDlydia.cNo ratings yet

- Accounting FormatsDocument21 pagesAccounting FormatsAsima ZubairNo ratings yet

- Section 1: The Basic Economic ProblemDocument10 pagesSection 1: The Basic Economic ProblemfarahNo ratings yet

- Economics Textbook AnswereDocument100 pagesEconomics Textbook Answereom100% (1)

- IGCSE 1.5 Business Objectives and Stakeholder ObjectivesDocument30 pagesIGCSE 1.5 Business Objectives and Stakeholder Objectivesayla.kowNo ratings yet

- Sample Question and Answers: Business Studies 0450/0986 Worksheet 1 Business ActivityDocument3 pagesSample Question and Answers: Business Studies 0450/0986 Worksheet 1 Business ActivityAbdullah HassanNo ratings yet

- Cambridge IGCSE: 0450/21 Business StudiesDocument13 pagesCambridge IGCSE: 0450/21 Business StudiesMpp VlogNo ratings yet

- Pdfcaie Igcse Business Studies 0450 Theory v1 PDFDocument36 pagesPdfcaie Igcse Business Studies 0450 Theory v1 PDFneil jhamnaniNo ratings yet

- IGCSE-OL - Bus - Sec - 1 - Answers To Case Study - Enhanced - 1ADocument7 pagesIGCSE-OL - Bus - Sec - 1 - Answers To Case Study - Enhanced - 1Aryan inasuNo ratings yet

- Reyhan Huseynova Activity 4.4 Business ManagementDocument6 pagesReyhan Huseynova Activity 4.4 Business ManagementReyhanNo ratings yet

- CH 5 Business Objectives and Stakeholder ObjectivesDocument18 pagesCH 5 Business Objectives and Stakeholder ObjectivesFiona Tauro100% (1)

- Worksheet 2.1 Introducing Business DocumentsDocument3 pagesWorksheet 2.1 Introducing Business Documentsaysilislam528No ratings yet

- ASAL Business CB Chapter 31 AnswersDocument12 pagesASAL Business CB Chapter 31 Answers-shinagami-No ratings yet

- Correction of ErrorsDocument32 pagesCorrection of ErrorsAdil IqbalNo ratings yet

- 1 3 Enterprise Business Growth and SizeDocument7 pages1 3 Enterprise Business Growth and Sizeaboudd30100% (1)

- IGCSE Business 6 QuestionDocument1 pageIGCSE Business 6 QuestionVerify MeNo ratings yet

- G.ix. Chapter 1.1 & 1.2 WorksheetDocument5 pagesG.ix. Chapter 1.1 & 1.2 WorksheetMangesh RahateNo ratings yet

- Irrecoverable Debts Practice Question AnsDocument7 pagesIrrecoverable Debts Practice Question Ansprathawinchester0309No ratings yet

- 0452 s03 Ms 2Document6 pages0452 s03 Ms 2lie chingNo ratings yet

- Economics R.kitDocument227 pagesEconomics R.kitWesleyNo ratings yet

- Unit 2 The Allocation of Resources: How The Market Works Market FailureDocument12 pagesUnit 2 The Allocation of Resources: How The Market Works Market FailureJada CameronNo ratings yet

- Cash Book Revision o LevelDocument10 pagesCash Book Revision o Levelnajla nisthar0% (1)

- f3 Accounting Study Pack Term 2 Week 6 Lesson 1-2021Document13 pagesf3 Accounting Study Pack Term 2 Week 6 Lesson 1-2021Iss MeNo ratings yet

- Business Studies Exam Style QuestionsDocument6 pagesBusiness Studies Exam Style QuestionsBryan MendozaNo ratings yet

- Grade 9 Accounting Syllabus Overview 2020-2021Document5 pagesGrade 9 Accounting Syllabus Overview 2020-2021Kelvin CalvinNo ratings yet

- Cambridge International As and A Level Accounting Coursebook Answer SectionDocument2 pagesCambridge International As and A Level Accounting Coursebook Answer Sectionhenry100% (2)

- MAY / JUNE 2006 P1 Short Answer EssayDocument20 pagesMAY / JUNE 2006 P1 Short Answer EssayNafisa MeghaNo ratings yet

- Chapter 8 IGCSEDocument48 pagesChapter 8 IGCSEtaj qaiserNo ratings yet

- Chapter 16 Answers 240113 205926Document6 pagesChapter 16 Answers 240113 205926Ejaz TariqNo ratings yet

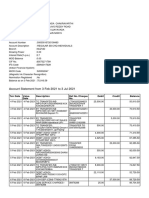

- Account Statement - 2022 04 01 - 2022 04 30 - en GB - 72261aDocument6 pagesAccount Statement - 2022 04 01 - 2022 04 30 - en GB - 72261acaitiewhiteman1993No ratings yet

- World Trade Organisation (WTO)Document22 pagesWorld Trade Organisation (WTO)ISHFAQ ASHRAFNo ratings yet

- Morkalan BillDocument2 pagesMorkalan Billsardar amanat aliHadian00rNo ratings yet

- Cheat Sheet For ValuationDocument4 pagesCheat Sheet For ValuationRISHAV BAIDNo ratings yet

- Tariff & Non-Tariff BarriersDocument29 pagesTariff & Non-Tariff BarriersSanjivSIngh0% (1)

- Custom Clearance Procedure PDFDocument70 pagesCustom Clearance Procedure PDFManish Chaurasia92% (24)

- Role of Foreign Direct Investment (Fdi) in India's Economic Development-An AnalysisDocument13 pagesRole of Foreign Direct Investment (Fdi) in India's Economic Development-An Analysispandurang parkarNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)PV VimalNo ratings yet

- Tax Invoice (Credit) : Katla Bazaar, Madanganj-Kishangarh GSTIN/UIN: 08AADHS5286D2ZY State Name: Rajasthan, Code: 08Document2 pagesTax Invoice (Credit) : Katla Bazaar, Madanganj-Kishangarh GSTIN/UIN: 08AADHS5286D2ZY State Name: Rajasthan, Code: 08Surajmal TansukhraiNo ratings yet

- International Business Report 1Document14 pagesInternational Business Report 1api-401427082100% (1)

- Retail Management ProjectDocument52 pagesRetail Management ProjectAnand Yamarthi100% (2)

- Green Modern Analysis of Results PresentationDocument12 pagesGreen Modern Analysis of Results PresentationGautamNo ratings yet

- Tax 304 - Vat Compliance RequirementsDocument5 pagesTax 304 - Vat Compliance RequirementsiBEAYNo ratings yet

- Rasha M. ElakkadDocument19 pagesRasha M. ElakkadHunal Kumar MautadinNo ratings yet

- 19510100000753Document2 pages19510100000753Afshan MojahidNo ratings yet

- Transportation and Logistics in Mena Complete ReportDocument63 pagesTransportation and Logistics in Mena Complete ReportAyaz Ahmed KhanNo ratings yet

- Growth Drivers of Retail in IndiaDocument10 pagesGrowth Drivers of Retail in IndiaRajshreeNo ratings yet

- Learning Outcomes:: SolutionDocument4 pagesLearning Outcomes:: Solutiondreamfever0323No ratings yet

- TescoDocument13 pagesTescoDat BoiNo ratings yet

- CurrentDocument15 pagesCurrentmonmon kimNo ratings yet

- Account Statement - 2024 02 01 - 2024 02 15 - en GB - 5fb6b4Document7 pagesAccount Statement - 2024 02 01 - 2024 02 15 - en GB - 5fb6b4mercedesjankobonusNo ratings yet

- Repayment ReceiptDocument1 pageRepayment ReceiptTarak BeheraNo ratings yet

- Public Finance MCQDocument23 pagesPublic Finance MCQHarshit Tripathi100% (1)

- 2020 Unit 2 SAC 2 Question BookDocument7 pages2020 Unit 2 SAC 2 Question BookSarita SinghNo ratings yet

- Ip SC MOghht 9 Sooj YDocument14 pagesIp SC MOghht 9 Sooj YUsha SaliNo ratings yet

- International Finance MCQ With Answers PDFDocument5 pagesInternational Finance MCQ With Answers PDFMijanur Rahman0% (1)

- Intermediate & Final Timetable & Brochure-1Document2 pagesIntermediate & Final Timetable & Brochure-1Hamis KandomeNo ratings yet

- IH NotesDocument2 pagesIH NotesSuryansh AggarwalNo ratings yet