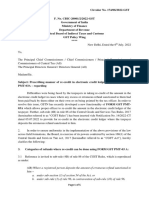

Circular No.59

Circular No.59

Download as pdf or txt

You might also like

- Bank StatementDocument5 pagesBank Statementmayur pol100% (1)

- RR 2-98 Section 2.57 (B) - CWTDocument3 pagesRR 2-98 Section 2.57 (B) - CWTZenaida LatorreNo ratings yet

- Dutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshDocument2 pagesDutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshNur NobiNo ratings yet

- Circular Refund 147-1.5 Times RefundDocument5 pagesCircular Refund 147-1.5 Times Refundbanerjeeankita13No ratings yet

- Cir 174 06 2022 CGSTDocument5 pagesCir 174 06 2022 CGSTNM JHANWAR & ASSOCIATESNo ratings yet

- SOP For ScrutinyDocument5 pagesSOP For Scrutinyacgstdiv4No ratings yet

- Circular CGST 125Document29 pagesCircular CGST 125N.V.No ratings yet

- Circular-No-227-2024Document3 pagesCircular-No-227-2024My gamesNo ratings yet

- Page 1 of 8Document8 pagesPage 1 of 8Faiqa HamidNo ratings yet

- Cir 147Document7 pagesCir 147sachinNo ratings yet

- Taxguru - In-Madras HC Permits Re-Submission of Form GSTR-3BDocument9 pagesTaxguru - In-Madras HC Permits Re-Submission of Form GSTR-3BChittiNo ratings yet

- Taxguru - In-Assessee Permitted To Make Changes in Form GSTR-3B For July 2017 March 2018Document11 pagesTaxguru - In-Assessee Permitted To Make Changes in Form GSTR-3B For July 2017 March 2018ChittiNo ratings yet

- Circularno 24 CGSTDocument4 pagesCircularno 24 CGSTHr legaladviserNo ratings yet

- Cancellation CircularDocument3 pagesCancellation CircularpeyushNo ratings yet

- Circular No 70 - NewDocument3 pagesCircular No 70 - NewHr legaladviserNo ratings yet

- Royal Industries_Reply to SCN_May'23_AK - FinalDocument44 pagesRoyal Industries_Reply to SCN_May'23_AK - Finalcajagadeesh222No ratings yet

- Vin Motors 2017-18 73Document10 pagesVin Motors 2017-18 73chandan patilNo ratings yet

- 2022 12 30 Circular No 183 15 2022 GST F No Cbic 20001 2 2022 GST Clarification To Deal With DiDocument3 pages2022 12 30 Circular No 183 15 2022 GST F No Cbic 20001 2 2022 GST Clarification To Deal With Diswanay.mohantyNo ratings yet

- CBIC Instruction 02-2023 dtd 26052023 SOP ScrutinyDocument6 pagesCBIC Instruction 02-2023 dtd 26052023 SOP Scrutinyrange47ajmerNo ratings yet

- Circular No.60Document4 pagesCircular No.60Hr legaladviserNo ratings yet

- 4 . Inverted Duty Structure under GST An OverviewDocument15 pages4 . Inverted Duty Structure under GST An Overviewbhagwati prasad singhNo ratings yet

- ITC Utilization in DRC-03 For GSTR-9 Amp GSTR-9CDocument6 pagesITC Utilization in DRC-03 For GSTR-9 Amp GSTR-9CChaithanya RajuNo ratings yet

- Maharashtra Trade Circular 21T of 2024 Dated 13 08 2024 1724248069Document7 pagesMaharashtra Trade Circular 21T of 2024 Dated 13 08 2024 1724248069updates.receiveNo ratings yet

- 003 ITC Mismatch in GSTR 2A Vs 2BDocument7 pages003 ITC Mismatch in GSTR 2A Vs 2BAman GargNo ratings yet

- Section 128A of CGST ActDocument74 pagesSection 128A of CGST Actcgstauditcircle8group37No ratings yet

- Refund of IGST On Export of Goods PDFDocument7 pagesRefund of IGST On Export of Goods PDFCA Rahul ModiNo ratings yet

- Circular No.45Document5 pagesCircular No.45Hr legaladviserNo ratings yet

- APL AnnexueDocument4 pagesAPL Annexueca.cutesumit619No ratings yet

- Chapter 9 Reply of Notices Under GSTDocument15 pagesChapter 9 Reply of Notices Under GSTDR. PREETI JINDALNo ratings yet

- Circular No 211 05 2024Document4 pagesCircular No 211 05 2024हिनयकुमार मारुती सोनकवडेNo ratings yet

- Office of The Commissioner of Kolkata South CGST & CX: Kolkata GST Bhawan: 180, Rajdanga Main Road: Shantipally: Kolkata-700107Document6 pagesOffice of The Commissioner of Kolkata South CGST & CX: Kolkata GST Bhawan: 180, Rajdanga Main Road: Shantipally: Kolkata-700107saifkha2211No ratings yet

- Office of The Commissioner of Kolkata South CGST & CX: Kolkata GST Bhawan: 180, Rajdanga Main Road: Shantipally: Kolkata-700107Document6 pagesOffice of The Commissioner of Kolkata South CGST & CX: Kolkata GST Bhawan: 180, Rajdanga Main Road: Shantipally: Kolkata-700107saifkha2211No ratings yet

- ITC Reversal Due To Non-Payment Within 180 DaysDocument2 pagesITC Reversal Due To Non-Payment Within 180 DaysRajdev AssociatesNo ratings yet

- Draft Payment RulesDocument5 pagesDraft Payment RulesLillyLalithaNo ratings yet

- SCN Microtek October 2022Document10 pagesSCN Microtek October 2022gstparwanoodivNo ratings yet

- Cir 188 20 2022 CGSTDocument4 pagesCir 188 20 2022 CGSTAtanu Kumar SenNo ratings yet

- Circular-No-238-2024 Clarification of Doubts Under Sec 128ADocument15 pagesCircular-No-238-2024 Clarification of Doubts Under Sec 128AguptasuneetNo ratings yet

- Chapter 7 Input Tax Credit Under GSTDocument28 pagesChapter 7 Input Tax Credit Under GSTDR. PREETI JINDALNo ratings yet

- AAR On Financial Credit Notes MRF LimitedDocument10 pagesAAR On Financial Credit Notes MRF LimitedroshanjajooNo ratings yet

- TaxmannPPT - GST Litigation - Challenges and SolutionsDocument25 pagesTaxmannPPT - GST Litigation - Challenges and Solutionsmsanjib920No ratings yet

- Internal Circular (Restricted Circular For Office Use Only)Document16 pagesInternal Circular (Restricted Circular For Office Use Only)Manish K JadhavNo ratings yet

- RefundDocument34 pagesRefunddhruv MahajanNo ratings yet

- RR 3-02Document6 pagesRR 3-02matinikkiNo ratings yet

- GST Automated NoticesDocument6 pagesGST Automated NoticesMaunik ParikhNo ratings yet

- Draft Refund RulesDocument7 pagesDraft Refund RulessridharanNo ratings yet

- Cir 182 14 2022 CGSTDocument14 pagesCir 182 14 2022 CGSTArnav AggarwalNo ratings yet

- Refund Under GST Regime Up To Date 12-03-2021 Detailed AnalysisDocument17 pagesRefund Under GST Regime Up To Date 12-03-2021 Detailed AnalysisChaithanya RajuNo ratings yet

- Composition Rules SummaryDocument6 pagesComposition Rules Summaryguruswamy.ayyapanNo ratings yet

- Chapter 11 GST ReturnsDocument18 pagesChapter 11 GST ReturnsDR. PREETI JINDALNo ratings yet

- Circular CGST 197Document5 pagesCircular CGST 197Jaipur-B Gr-2No ratings yet

- Report No. 5 - 22 - Chapter-3-062f0e3be996485.72192939Document30 pagesReport No. 5 - 22 - Chapter-3-062f0e3be996485.72192939srbhgangu123No ratings yet

- Cir 183 15 2022 CGSTDocument5 pagesCir 183 15 2022 CGSTAmritesh RaiNo ratings yet

- Article On Assessment and AuditDocument33 pagesArticle On Assessment and Auditmks895525No ratings yet

- Section 16 of CGST Act 2017 - Eligibility & Conditions For Taking Input Tax Credit - Taxguru - inDocument3 pagesSection 16 of CGST Act 2017 - Eligibility & Conditions For Taking Input Tax Credit - Taxguru - inDHANNNo ratings yet

- Draft Reply To Notice For Mismatch in ITC As Per GSTR 3B, GSTR 9 & GSTR 2ADocument11 pagesDraft Reply To Notice For Mismatch in ITC As Per GSTR 3B, GSTR 9 & GSTR 2ACA Mohit GargNo ratings yet

- Guideline Assessment 63Document4 pagesGuideline Assessment 63pinaki mukherjeeNo ratings yet

- GST Latest Updates - Action Points To Be Checked in Nov'24Document14 pagesGST Latest Updates - Action Points To Be Checked in Nov'24MD Rafeeq Mba CmaNo ratings yet

- 06 A Idt Ammentments 2 in 1Document33 pages06 A Idt Ammentments 2 in 1Venkat RamanaNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep - Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep - Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- 1040 Exam Prep - Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep - Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- GST Class 10Document22 pagesGST Class 10avrs1299No ratings yet

- Detailed Estimate TemplateDocument1 pageDetailed Estimate TemplateEdmar BaldozaNo ratings yet

- Bkxs L9 Az IHx 5 Uc CMDocument6 pagesBkxs L9 Az IHx 5 Uc CMVIPIN SHARMANo ratings yet

- SurnameDocument1 pageSurnamesanbimatsayfarmNo ratings yet

- Notice To TP (RMO 15-2018)Document3 pagesNotice To TP (RMO 15-2018)Christian Albert HerreraNo ratings yet

- Delhi To Ranchi TicketDocument1 pageDelhi To Ranchi Ticketadarshbhankar00000No ratings yet

- Mathematics Book Book 1701441017923Document2 pagesMathematics Book Book 1701441017923tanmaybonde30No ratings yet

- INADMISSIBLEDocument4 pagesINADMISSIBLEADNAN AHMEDNo ratings yet

- Account Modification FormDocument3 pagesAccount Modification FormAbhishek GuptaNo ratings yet

- DT Compressed PDFDocument500 pagesDT Compressed PDFAshish Sisodia100% (1)

- 2015 10 20 Trends in The Indirect Tax Landscape and The Impact of BEPSDocument60 pages2015 10 20 Trends in The Indirect Tax Landscape and The Impact of BEPSMahesh KinalkarNo ratings yet

- PI Steel Structure Workshop Baofeng Gina 4.4Document1 pagePI Steel Structure Workshop Baofeng Gina 4.4wilson starkNo ratings yet

- 2 - Bir Ruling No. 517-11Document5 pages2 - Bir Ruling No. 517-11Gino Alejandro SisonNo ratings yet

- Deed of Cancellation of Contract of SaleDocument3 pagesDeed of Cancellation of Contract of SaleD.F. de Lira50% (2)

- PTE Academic OnlineDocument10 pagesPTE Academic OnlineMahendraNo ratings yet

- Date Narration Value Date Withdrawal Deposit Cheque/Ref. No. Closing BalanceDocument5 pagesDate Narration Value Date Withdrawal Deposit Cheque/Ref. No. Closing BalanceNanu PatelNo ratings yet

- KsebBill 1155058024039Document1 pageKsebBill 1155058024039akkgptcktmNo ratings yet

- Bank StatementDocument2 pagesBank StatementDJ TuchaNo ratings yet

- MI TV 43 InchDocument2 pagesMI TV 43 Inchharry tharunNo ratings yet

- Chap 13 - Income From BusinessDocument14 pagesChap 13 - Income From BusinessMuhammad Saad UmarNo ratings yet

- E WalletSystemforBangladeshanElectronicPaymentDocument5 pagesE WalletSystemforBangladeshanElectronicPaymentchentika bungaNo ratings yet

- Gasbill 3851735781 202003 20200423020450Document1 pageGasbill 3851735781 202003 20200423020450Shahzaib GujjarNo ratings yet

- C7021-22-2717923 30-03-2023 30-03-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP UshaDocument1 pageC7021-22-2717923 30-03-2023 30-03-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP UshaViraj DobriyalNo ratings yet

- Solutions To Self-Study Problems: Chapter 1 The Individual Income Tax ReturnDocument84 pagesSolutions To Self-Study Problems: Chapter 1 The Individual Income Tax ReturnTiffy LouiseNo ratings yet

- Telus 606759756 2024 06 13Document4 pagesTelus 606759756 2024 06 13Je JeNo ratings yet

- Exercises On Chapter 12 & 13Document8 pagesExercises On Chapter 12 & 13Iqmal khushairiNo ratings yet

- Setting Up Quickbooks For GSTDocument3 pagesSetting Up Quickbooks For GSTDONNo ratings yet

- Estatement 1Document2 pagesEstatement 1MargaritaHerreraNo ratings yet