5 TH

5 TH

Download as pdf or txt

You might also like

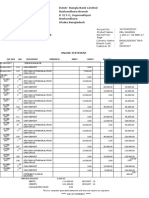

- Dutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshDocument2 pagesDutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshNur NobiNo ratings yet

- What Are The Soxeca Application Dates and Why Are They Different From Annex Vi?Document4 pagesWhat Are The Soxeca Application Dates and Why Are They Different From Annex Vi?vdevivNo ratings yet

- EC Prestige Annex1Document27 pagesEC Prestige Annex1flipflop12No ratings yet

- Minutes - ESSF - WFS - 10th Meeting - FinalDocument10 pagesMinutes - ESSF - WFS - 10th Meeting - FinalMartin HristovNo ratings yet

- Consolidated TEXT: ConslegDocument6 pagesConsolidated TEXT: ConslegCostinRotaruNo ratings yet

- Marpol 73Document3 pagesMarpol 73Arie AozNo ratings yet

- Official Journal L40: of The European UnionDocument24 pagesOfficial Journal L40: of The European UnionTVTA3No ratings yet

- Com 2023 657 en 0Document7 pagesCom 2023 657 en 0av1986362No ratings yet

- CMD Alexandre Tagore Presentation ISA 26 Nov 2008Document19 pagesCMD Alexandre Tagore Presentation ISA 26 Nov 2008marcos_ayala_12No ratings yet

- EU Directive 2006-87-EC-Requirements For Inland Waterway Vessels-ConsolidedDocument367 pagesEU Directive 2006-87-EC-Requirements For Inland Waterway Vessels-ConsolidedAleksandar DobrodolacNo ratings yet

- 2023 - 1805 (Regulation) - On The Use of Renewable and Low-Carbon Fuels in Maritime Transport, and Amending Directive 2009 - 16 - ECDocument53 pages2023 - 1805 (Regulation) - On The Use of Renewable and Low-Carbon Fuels in Maritime Transport, and Amending Directive 2009 - 16 - ECmarina.vlaicNo ratings yet

- PE 26 2023 INIT - enDocument139 pagesPE 26 2023 INIT - enGanesh Bharath KumarNo ratings yet

- Guide Short Sea Shipping en PDFDocument53 pagesGuide Short Sea Shipping en PDFAriv PTANNo ratings yet

- R (Factortame LTD) V Secretary of State For Transport: Court Full Case Name DecidedDocument13 pagesR (Factortame LTD) V Secretary of State For Transport: Court Full Case Name DecidedRevekka TheodorouNo ratings yet

- Commission of The European Communities, Represented by T. Van Rijn andDocument18 pagesCommission of The European Communities, Represented by T. Van Rijn andAlin NichiforNo ratings yet

- FUELEUDocument53 pagesFUELEUhugo YangNo ratings yet

- MGN 385 - TaggedDocument12 pagesMGN 385 - TaggedmanenderNo ratings yet

- Marine Pollution SourcesDocument45 pagesMarine Pollution Sourcesaika hartini100% (1)

- Thong Tin Va Mot So An Pham Cua IMO Duoc Cap Nhat, Sua DoiDocument100 pagesThong Tin Va Mot So An Pham Cua IMO Duoc Cap Nhat, Sua Doivannuipham67No ratings yet

- CLCS 60-EnDocument13 pagesCLCS 60-EnClyne TranNo ratings yet

- Convention On Facilitation of International Maritime TrafficDocument7 pagesConvention On Facilitation of International Maritime Trafficbittu692No ratings yet

- Annex C Draft MSN 1879Document34 pagesAnnex C Draft MSN 1879Mahesh KumbharNo ratings yet

- Marpol: NameDocument12 pagesMarpol: NameAhmed AboelmagdNo ratings yet

- RevisedMARPOL AnnexVIDocument34 pagesRevisedMARPOL AnnexVIrigaNo ratings yet

- 30 May 2012 No. 488 Environmental Safety For Ships and Mobile Offshore UnitsDocument5 pages30 May 2012 No. 488 Environmental Safety For Ships and Mobile Offshore UnitsValentin GiugleaNo ratings yet

- Σύμβαση παραχώρησης ΟΛΠDocument82 pagesΣύμβαση παραχώρησης ΟΛΠΘάνος ΚαμήλαληςNo ratings yet

- MEPC 68-7 - Amendments To The Form of Garbage Record Book (Australia, Liberia and Ne... )Document5 pagesMEPC 68-7 - Amendments To The Form of Garbage Record Book (Australia, Liberia and Ne... )ehbeckmanNo ratings yet

- Mgn159 - Marine PollutantsDocument12 pagesMgn159 - Marine Pollutantsaakash9090No ratings yet

- Agenda PDFDocument55 pagesAgenda PDFgeorgadam1983No ratings yet

- EU Air Transport Policy: Implications On Airlines and AirportsDocument42 pagesEU Air Transport Policy: Implications On Airlines and AirportsGabriel RazvanNo ratings yet

- 2014s Emsa Training On MLC, 2006 GCDocument28 pages2014s Emsa Training On MLC, 2006 GCGoran JurisicNo ratings yet

- Uk MRVDocument19 pagesUk MRVHarman SandhuNo ratings yet

- En 1998L0041 Do 001 PDFDocument9 pagesEn 1998L0041 Do 001 PDFCostinRotaruNo ratings yet

- Convention On Facilitation of International Maritime Traffic, 1965Document4 pagesConvention On Facilitation of International Maritime Traffic, 1965tallmansahuNo ratings yet

- C (2016) 3502 enDocument27 pagesC (2016) 3502 enAnonymous 4m2wW1EpNo ratings yet

- PRR - 2nd Draft Compromise (RO Presidency) - 06 June 2019Document85 pagesPRR - 2nd Draft Compromise (RO Presidency) - 06 June 2019Kateřina VokounováNo ratings yet

- MSC Circ. 955Document1 pageMSC Circ. 955P Venkata SureshNo ratings yet

- En 2002R0417 Do 001 PDFDocument10 pagesEn 2002R0417 Do 001 PDFCostinRotaruNo ratings yet

- 98 - 41 - CE Consolidada 2008ENDocument9 pages98 - 41 - CE Consolidada 2008ENPedro MorgadoNo ratings yet

- 2010 0450 enDocument11 pages2010 0450 ensdhumieresNo ratings yet

- Order On The Ship Reporting System BELTREP and On Navigation Under The East Bridge and The West Bridge in The Great BeltDocument14 pagesOrder On The Ship Reporting System BELTREP and On Navigation Under The East Bridge and The West Bridge in The Great Beltcaruzo082No ratings yet

- CO2 Regulation of The European Parliament and of The CouncilDocument47 pagesCO2 Regulation of The European Parliament and of The CouncilAlfonso BericuaNo ratings yet

- Celex 52013PC0480 en TXTDocument47 pagesCelex 52013PC0480 en TXTMarilena TzortziNo ratings yet

- Decree On Ship SurveysDocument13 pagesDecree On Ship SurveysAngelo AlonsoNo ratings yet

- IG Circular EU Sanctions - Clarification Published On The Carriage of Certain Russian Cargoes Including Coal and Fertilisers - 120822Document3 pagesIG Circular EU Sanctions - Clarification Published On The Carriage of Certain Russian Cargoes Including Coal and Fertilisers - 120822Efthymios LouridasNo ratings yet

- quy định IUUDocument105 pagesquy định IUUThuy Linh NguyenNo ratings yet

- Implementation of The International Safety Management (Ism) Code BY 1 JULY 2002Document2 pagesImplementation of The International Safety Management (Ism) Code BY 1 JULY 2002sabaingiNo ratings yet

- 4 Albert Embankment London Se1 7Sr Telephone: 020 7735 7611 Fax: 020 7587 3210 Telex: 23588 IMOLDN GDocument1 page4 Albert Embankment London Se1 7Sr Telephone: 020 7735 7611 Fax: 020 7587 3210 Telex: 23588 IMOLDN GRodrigoSantanderVegasNo ratings yet

- Conventions - HandoutDocument21 pagesConventions - Handout7z8yqd66nqNo ratings yet

- Orld Rade RganizationDocument31 pagesOrld Rade RganizationHitesh ParmarNo ratings yet

- Assignment C Extra First Class Course - Part ADocument13 pagesAssignment C Extra First Class Course - Part ARohit SethNo ratings yet

- Practical Handbook Amends-16 8 2010Document12 pagesPractical Handbook Amends-16 8 2010IacobDorinaNo ratings yet

- CMI Year Book 2001-SingaporeDocument724 pagesCMI Year Book 2001-SingaporeMugurel Iulian Moldoveanu100% (1)

- Guidance For Ship InspectionsDocument26 pagesGuidance For Ship InspectionsFr BNo ratings yet

- Draft EU Directive With AmmendmentsDocument146 pagesDraft EU Directive With Ammendmentsjahehe2000No ratings yet

- MG 2 13 7 PDFDocument5 pagesMG 2 13 7 PDFRamson RaymondNo ratings yet

- MARPOL 73-78 DosyasıDocument4 pagesMARPOL 73-78 DosyasıBeratYaşarNo ratings yet

- Consolidated TEXT: ConslegDocument34 pagesConsolidated TEXT: ConslegCostinRotaruNo ratings yet

- MED Directive 2014-90-EuDocument291 pagesMED Directive 2014-90-EuManuel GheorghiuNo ratings yet

- Erich Ciola: JUDGMENT OF 29. 4. 1999 - CASE C-224/97Document12 pagesErich Ciola: JUDGMENT OF 29. 4. 1999 - CASE C-224/97Daniela GoreaciiNo ratings yet

- Maritime Labour ConventionFrom EverandMaritime Labour ConventionRating: 5 out of 5 stars5/5 (1)

- Tax, Tip, Markup Notes OB KeyDocument3 pagesTax, Tip, Markup Notes OB Keyakivort29No ratings yet

- Engineering and Construction Contract Option FDocument3 pagesEngineering and Construction Contract Option FJuan Carlos50% (2)

- SUMMATIVE TEST 4Q Module 2Document4 pagesSUMMATIVE TEST 4Q Module 2Marivic Bernardo GalvezNo ratings yet

- AL BSL OrdinancesDocument152 pagesAL BSL OrdinancesMelanie HughesNo ratings yet

- Mixed Location List 24th April 24 - 350 DataDocument25 pagesMixed Location List 24th April 24 - 350 DatasarathNo ratings yet

- Citizens Charter: Capacuhan Elementary School, AnahawanDocument1 pageCitizens Charter: Capacuhan Elementary School, AnahawanMa. Rema PiaNo ratings yet

- CIPET-QF-7711 Format For Inspection ContractDocument5 pagesCIPET-QF-7711 Format For Inspection ContractUmeshNo ratings yet

- Delaware Capital Formation v. Krobach Mfg. - 102110Document13 pagesDelaware Capital Formation v. Krobach Mfg. - 102110jason codyNo ratings yet

- Arula Vs EspinoDocument6 pagesArula Vs EspinoNikki Joanne Armecin LimNo ratings yet

- Government of Pakistan Privatisation CommissionDocument3 pagesGovernment of Pakistan Privatisation CommissionMomin IqbalNo ratings yet

- LP Business Finance 1Document15 pagesLP Business Finance 1Rutchel NavoaNo ratings yet

- Contracts Outline RevisedDocument6 pagesContracts Outline RevisedLyn M. GrantNo ratings yet

- MDocument12 pagesMapi-3745637No ratings yet

- MSDS SK Supercut HN 5Document4 pagesMSDS SK Supercut HN 5sheNo ratings yet

- Yojana May 2021Document64 pagesYojana May 2021Eman ArshadNo ratings yet

- Chapter 1 Ncert XIIDocument16 pagesChapter 1 Ncert XIIaaditya160807No ratings yet

- SSC Steno 2023 Application FormDocument4 pagesSSC Steno 2023 Application FormBharathi SamireddyNo ratings yet

- Legislative History - Miami-Dade County Gender Pricing Ordinance 1996 - 2002Document23 pagesLegislative History - Miami-Dade County Gender Pricing Ordinance 1996 - 2002Raisa S.No ratings yet

- In Re Ricafort DigestDocument3 pagesIn Re Ricafort DigestNorie Sapanta100% (1)

- 01 Nordberg CH 01Document10 pages01 Nordberg CH 01Spandana AchantaNo ratings yet

- DPC Assignment MOUDocument8 pagesDPC Assignment MOUaryanNo ratings yet

- BankruptcyDocument29 pagesBankruptcyPraveena PeterNo ratings yet

- Pretrial BriefDocument4 pagesPretrial BriefKisha Karen ArafagNo ratings yet

- Group Discussion (LBT)Document30 pagesGroup Discussion (LBT)Acidri Francis (Counsel Acid)No ratings yet

- Finance and MGTDocument21 pagesFinance and MGTsameer_ahmed89No ratings yet

- IIMA - Industry ReportsDocument52 pagesIIMA - Industry ReportsParth SOODANNo ratings yet

- Offence of Robbery - Important CasesDocument54 pagesOffence of Robbery - Important CasesStudentLawTarun100% (4)

- AngelaDocument1 pageAngeladmassbagoesNo ratings yet

- WAC6550 Series: 802.11ac Outdoor Access PointDocument6 pagesWAC6550 Series: 802.11ac Outdoor Access PointClaudioNo ratings yet