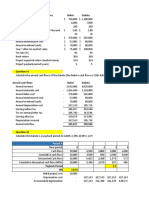

Afar 05a

Afar 05a

Download as pdf or txt

You might also like

- HUNTINGTON NATIONAL BANK StatementDocument7 pagesHUNTINGTON NATIONAL BANK StatementEmannuel Ontario74% (35)

- The Magic of Getting What You WantDocument284 pagesThe Magic of Getting What You WantOomar Capery100% (15)

- Case of Franklin LumberDocument4 pagesCase of Franklin LumberSedih Berasa100% (2)

- Case 5Document12 pagesCase 5JIAXUAN WANGNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Tax Invoice: Delivery ToDocument1 pageTax Invoice: Delivery ToManoj MalikNo ratings yet

- Cognovi Labs FinancialsDocument52 pagesCognovi Labs FinancialsShukran AlakbarovNo ratings yet

- LA 2 Construction Contracts PDFDocument3 pagesLA 2 Construction Contracts PDFliliNo ratings yet

- CADocument2 pagesCAHannahNo ratings yet

- Free Cash Flow CalculationDocument31 pagesFree Cash Flow CalculationPaulNo ratings yet

- Intermediate Accounting II Chapter 18Document2 pagesIntermediate Accounting II Chapter 18izza zahratunnisaNo ratings yet

- Sample Financial Projections676Document21 pagesSample Financial Projections676assefamenelik1No ratings yet

- Financial Accounting Ifrs 4e Solution Ch04Document50 pagesFinancial Accounting Ifrs 4e Solution Ch04蔡宜欣No ratings yet

- Homework Chapter 20 - Group 8Document5 pagesHomework Chapter 20 - Group 8Thư LuyệnNo ratings yet

- Tugas 2, ANALISIS LAPORAN KEUANGANDocument9 pagesTugas 2, ANALISIS LAPORAN KEUANGANlessyNo ratings yet

- Fix It Financial Statemnets (No Data Version)Document13 pagesFix It Financial Statemnets (No Data Version)F010emNo ratings yet

- Baf 422 Continous Assessment Test Class Assignment 20240328Document5 pagesBaf 422 Continous Assessment Test Class Assignment 20240328briankuria21No ratings yet

- Ceci TEAMWORK HW - Case - New and Repaired FurnaceDocument14 pagesCeci TEAMWORK HW - Case - New and Repaired FurnaceMarcela GzaNo ratings yet

- IF1 2102E TBS01 02.simulationDocument4 pagesIF1 2102E TBS01 02.simulationharnoor11s100% (1)

- 5 - Depericiation, WC, Scenarios - With Dep FormulaDocument8 pages5 - Depericiation, WC, Scenarios - With Dep FormulaFaisal NAUMANNo ratings yet

- P1AD21Document12 pagesP1AD21Unanimous OneNo ratings yet

- 04SDocument5 pages04SEric Jed OlivarezNo ratings yet

- Assignment 2 - Strategic Financial Management - Abdulhakeem MustafaDocument7 pagesAssignment 2 - Strategic Financial Management - Abdulhakeem MustafaHakeem SnrNo ratings yet

- 06 Task Performance 1 ARGDocument4 pages06 Task Performance 1 ARGshiplusNo ratings yet

- Yolanda Reality Work Sheet For The Month Ended April 2020Document2 pagesYolanda Reality Work Sheet For The Month Ended April 2020Hannah DimalibotNo ratings yet

- Competency AssessmentDocument5 pagesCompetency AssessmentMiracle FlorNo ratings yet

- Projection ReportDocument12 pagesProjection ReportCA Ananta BhandariNo ratings yet

- Tutorial 5Document2 pagesTutorial 5mint chocolateNo ratings yet

- Fina 470 Project Two - Check PointDocument9 pagesFina 470 Project Two - Check PointMitchell ParrottNo ratings yet

- Socw - 1263543589Document7 pagesSocw - 1263543589dolevov652No ratings yet

- CH 4Document50 pagesCH 4nhungntt22405cNo ratings yet

- MBA and MBA (Banking & Finance) : Mmpc-004: Accounting For ManagersDocument20 pagesMBA and MBA (Banking & Finance) : Mmpc-004: Accounting For ManagersAvijit GuinNo ratings yet

- Ias 12 Question With AnswersDocument5 pagesIas 12 Question With AnswersPrince Daniels TutorNo ratings yet

- Financial PlanDocument7 pagesFinancial PlanFesto MshumaNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- 1.+FRA - Study+Guide - v2.0 23Document3 pages1.+FRA - Study+Guide - v2.0 23Jerlin PreethiNo ratings yet

- MS Brothers Super Rice MillDocument9 pagesMS Brothers Super Rice MillMasud Ahmed khan100% (1)

- AOP Sales - 23.12.2017Document12 pagesAOP Sales - 23.12.2017Rubayat MatinNo ratings yet

- Annexes 2021Document19 pagesAnnexes 2021Charish LariosaNo ratings yet

- Business PlanDocument11 pagesBusiness Plananil thapaNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document15 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- Financial Accounting Ifrs 4e Chapter 4 SolutionDocument50 pagesFinancial Accounting Ifrs 4e Chapter 4 SolutionSana SoomroNo ratings yet

- 3rd Long QuizDocument1 page3rd Long QuizRonah SabanalNo ratings yet

- FY2024 Proposed BudgetDocument17 pagesFY2024 Proposed BudgetArif EWSNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document14 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- Anandam Case AnalysisDocument5 pagesAnandam Case AnalysisVini ShethNo ratings yet

- Statement: Annual BudgetDocument76 pagesStatement: Annual Budgetshani2010No ratings yet

- Chapter 4Document35 pagesChapter 4ReineNo ratings yet

- Accountancy Auditing 2023Document7 pagesAccountancy Auditing 2023amir8407477No ratings yet

- Worksheet To FSDocument29 pagesWorksheet To FSChelsea TengcoNo ratings yet

- Chapter 6 PDFDocument23 pagesChapter 6 PDFreyNo ratings yet

- Solution Far410 Dec - 2019 - 1 - PDFDocument8 pagesSolution Far410 Dec - 2019 - 1 - PDF2022478048No ratings yet

- Complete Financial ModelDocument47 pagesComplete Financial ModelArrush AhujaNo ratings yet

- Financial Forecasting and CFC Valuation (Shell)Document2 pagesFinancial Forecasting and CFC Valuation (Shell)romeshpradeep31No ratings yet

- Financial Planning: 6.1 Start-Up Cost and Capital ExpenditureDocument4 pagesFinancial Planning: 6.1 Start-Up Cost and Capital ExpenditurearefeenaNo ratings yet

- 2816 Solution To Long Term Construction ContractsDocument47 pages2816 Solution To Long Term Construction ContractsPhoeza Espinosa Villanueva100% (1)

- 324 PratikBhandari Case1Document3 pages324 PratikBhandari Case1Manas MondalNo ratings yet

- Financial Accounting and Reporting-I: Page 1 of 7Document7 pagesFinancial Accounting and Reporting-I: Page 1 of 7Obaid RasheedNo ratings yet

- Nokia Corporation: ISIN: FI0009000681 WKN: Nokia Asset Class: StockDocument2 pagesNokia Corporation: ISIN: FI0009000681 WKN: Nokia Asset Class: StockMohtasim Bin HabibNo ratings yet

- ACCT 440 FMGT Exams 2021 SandwichDocument4 pagesACCT 440 FMGT Exams 2021 SandwichNubor RichardNo ratings yet

- AssignmentDocument6 pagesAssignmentAnkita KumariNo ratings yet

- Answer To RQ 3 - Week 6 PDFDocument1 pageAnswer To RQ 3 - Week 6 PDFcalebNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Excel Stock TrackingDocument315 pagesExcel Stock TrackingSyed HasanNo ratings yet

- The Institute of Chartered Shipbrokers: Answer Any FIVE Questions - All Questions Carry Equal MarksDocument4 pagesThe Institute of Chartered Shipbrokers: Answer Any FIVE Questions - All Questions Carry Equal MarksDeepak ShoriNo ratings yet

- Assignment - Dow ChemicalDocument2 pagesAssignment - Dow ChemicalRaj Kamal BishtNo ratings yet

- Introduction To Reward ManagementDocument43 pagesIntroduction To Reward ManagementHarsh RanjanNo ratings yet

- Bru World CafeDocument19 pagesBru World CaferavirajmistryNo ratings yet

- Bajaj XCDDocument4 pagesBajaj XCDshruti.shindeNo ratings yet

- Om - Location DecisionsDocument14 pagesOm - Location DecisionsMarissa C BautistaNo ratings yet

- Detroit EM Order No 18 CombinedDocument118 pagesDetroit EM Order No 18 CombinedStephen BoyleNo ratings yet

- Mahesh Summer Internship ReportDocument20 pagesMahesh Summer Internship ReportmaheshNo ratings yet

- Business Tool Register TemplateDocument2 pagesBusiness Tool Register TemplatenaveenkrealNo ratings yet

- Appsscm 1Document9 pagesAppsscm 1ashibekNo ratings yet

- Terms and Conditions EToroDocument42 pagesTerms and Conditions EToroZhess BugNo ratings yet

- Sub Order LabelsDocument4 pagesSub Order Labelssattar khanNo ratings yet

- Customer SatisfactionDocument64 pagesCustomer Satisfactionaishwarya ghorpadeNo ratings yet

- Your Electronic Ticket Receipt PDFDocument2 pagesYour Electronic Ticket Receipt PDFJanga RamireddyNo ratings yet

- Red HunterDocument3 pagesRed Hunterssknowledge07No ratings yet

- 16-1 Hospital Supply IncDocument4 pages16-1 Hospital Supply IncFrancisco Marvin100% (1)

- Pag Ibig Foreclosed Properties Pubbid101116 NCR No Discount CompressedDocument10 pagesPag Ibig Foreclosed Properties Pubbid101116 NCR No Discount CompressedkkkNo ratings yet

- 2005 Process Trends (040306) - Business Process Modelling PDFDocument209 pages2005 Process Trends (040306) - Business Process Modelling PDFdheer4dheerNo ratings yet

- Acatech STUDIE Maturity Index Eng WEB PDFDocument60 pagesAcatech STUDIE Maturity Index Eng WEB PDFCarlos MolinaNo ratings yet

- Informal SectorsDocument41 pagesInformal SectorsMikee TanNo ratings yet

- Maritime Muslim Academy Contract - Chebucto Road SchoolDocument14 pagesMaritime Muslim Academy Contract - Chebucto Road SchooleditorhilaryNo ratings yet

- MembersDocument79 pagesMembersErik HooverNo ratings yet

- Converting A Manual RTG Terminal To An AutoRTG TerminalDocument16 pagesConverting A Manual RTG Terminal To An AutoRTG Terminalacanbasri1980No ratings yet

- Conceptualizing, Measuring, and Managing Customer Based Brand Equity (Keller)Document23 pagesConceptualizing, Measuring, and Managing Customer Based Brand Equity (Keller)Sayed Shaiq Ali MusaviNo ratings yet

- City of Saratoga Springs: 2015 Comprehensive PlanDocument76 pagesCity of Saratoga Springs: 2015 Comprehensive PlanWendy LiberatoreNo ratings yet

- Market Research EntrepDocument18 pagesMarket Research EntrepKevin Miscala MelendresNo ratings yet