D14 F6SGP QP

D14 F6SGP QP

Download as pdf or txt

You might also like

- Sage Accpac Erp BrochureDocument16 pagesSage Accpac Erp Brochuredearsuru316No ratings yet

- F6SGP Dec2015q PDFDocument15 pagesF6SGP Dec2015q PDFDrift SirNo ratings yet

- Taxation (Singapore) : March/June 2016 - Sample QuestionsDocument10 pagesTaxation (Singapore) : March/June 2016 - Sample QuestionsJobsdudeNo ratings yet

- f6sgp 2017 Sep Dec Q PDFDocument10 pagesf6sgp 2017 Sep Dec Q PDFJobsdudeNo ratings yet

- Taxation - Singapore (TX - SGP) : Applied SkillsDocument19 pagesTaxation - Singapore (TX - SGP) : Applied SkillsLee WendyNo ratings yet

- Advanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsDocument12 pagesAdvanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsLee WendyNo ratings yet

- Advanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsDocument12 pagesAdvanced Taxation - Singapore (Atx - SGP) : Strategic Professional - Optionsnivethababu7No ratings yet

- Taxation (Singapore) : March/June 2018 - Sample QuestionsDocument10 pagesTaxation (Singapore) : March/June 2018 - Sample QuestionsLee WendyNo ratings yet

- Advanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsDocument13 pagesAdvanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsLee WendyNo ratings yet

- Week 8 - TDocument6 pagesWeek 8 - TataseskiNo ratings yet

- FM - Chapter 3 - QuizDocument8 pagesFM - Chapter 3 - QuizHausland Const. Corp.No ratings yet

- Income-tax-calculator-for-New-and-Old-tax-difference-FY-24-25-Original-1Document4 pagesIncome-tax-calculator-for-New-and-Old-tax-difference-FY-24-25-Original-1Shabin BlessonNo ratings yet

- Capital BudgetingDocument19 pagesCapital BudgetingcaapurvamehtaNo ratings yet

- Income Taxation Answer ExamDocument5 pagesIncome Taxation Answer Examyezaquera100% (1)

- Amendment May - 2024Document5 pagesAmendment May - 2024VINOD KUMARNo ratings yet

- TDS Calculation On Salary FinalDocument2 pagesTDS Calculation On Salary FinalKowsar HossainNo ratings yet

- Solutions On Capital BudgetingDocument25 pagesSolutions On Capital BudgetingASH GAMING GamesNo ratings yet

- Practice Problem Set #1 Capital Budgeting - Solution - : FIN 448, Sections 2 & 3, Fall 2020 Advanced Financial ManagementDocument5 pagesPractice Problem Set #1 Capital Budgeting - Solution - : FIN 448, Sections 2 & 3, Fall 2020 Advanced Financial ManagementAndrewNo ratings yet

- Faq'S & Guidlines On Income TaxDocument50 pagesFaq'S & Guidlines On Income Taxvelpurimani19No ratings yet

- Cash Flow Master Question With SolutionDocument6 pagesCash Flow Master Question With Solutionft2vny7nytNo ratings yet

- Ratio Analysis Numericals Including Reverse RatiosDocument6 pagesRatio Analysis Numericals Including Reverse RatiosFunny ManNo ratings yet

- Test 2Document7 pagesTest 2khowcatherine2000No ratings yet

- Exercise 9-5 No 9-20Document9 pagesExercise 9-5 No 9-20Kent LumanasNo ratings yet

- Reviewer Fabm2Document3 pagesReviewer Fabm2Mark LappayNo ratings yet

- Answer 1Document5 pagesAnswer 1mayetteNo ratings yet

- Assignment E & L Env 4 BusiDocument9 pagesAssignment E & L Env 4 BusiSyed Hamza RasheedNo ratings yet

- Main TablesDocument1 pageMain Tablesvishalbharatshah2776No ratings yet

- Tax Calculator 2018-19 (Farrukh Iqbal Khan)Document2 pagesTax Calculator 2018-19 (Farrukh Iqbal Khan)FarrukhNo ratings yet

- KTTC1AOFDocument5 pagesKTTC1AOFnnhuser255No ratings yet

- CH 12 SM AssigDocument6 pagesCH 12 SM AssigJefferson SarmientoNo ratings yet

- R2. TAX (M.L) Solution CMA May-2023 ExamDocument5 pagesR2. TAX (M.L) Solution CMA May-2023 ExamSharif MahmudNo ratings yet

- Amendments DT 2016Document70 pagesAmendments DT 2016dbp9050No ratings yet

- Special Allowable Itemized DeductionsDocument13 pagesSpecial Allowable Itemized DeductionsSandia EspejoNo ratings yet

- Managment Accountant ACCOW, OpenT, KPP WBDocument6 pagesManagment Accountant ACCOW, OpenT, KPP WBFarahAin FainNo ratings yet

- Final Activity Income TaxationDocument6 pagesFinal Activity Income TaxationPrincess MarianoNo ratings yet

- Financial Management Economics For Finance 2023 1671444516Document36 pagesFinancial Management Economics For Finance 2023 1671444516RADHIKANo ratings yet

- Test 1Document6 pagesTest 1khowcatherine2000No ratings yet

- Assessment of Charitable Trusts: Tax SupplementDocument3 pagesAssessment of Charitable Trusts: Tax SupplementCA Ved Parkash AroraNo ratings yet

- Solution of Governmentl CH 5Document18 pagesSolution of Governmentl CH 5Ahmad KamalNo ratings yet

- 204.TAXP_.L-II-December-2020-1 (1)Document4 pages204.TAXP_.L-II-December-2020-1 (1)mezbafaisalceoNo ratings yet

- Activity 13 May 2023 Key To CorrectionDocument1 pageActivity 13 May 2023 Key To CorrectionJohn Paul MagbitangNo ratings yet

- Ratio Analysis Numericals Including Reverse RatiosDocument6 pagesRatio Analysis Numericals Including Reverse Ratioscopying74No ratings yet

- Quiz 1 - StrataxDocument3 pagesQuiz 1 - Strataxspongebob SquarepantsNo ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- Class Exercise - Answer PA U202324 - AmendedDocument5 pagesClass Exercise - Answer PA U202324 - AmendedPeman YNo ratings yet

- Pointers-to-review-Finals.Document4 pagesPointers-to-review-Finals.dabyyyy0423No ratings yet

- Assignment - Chapter 2 - Problem 28 (Due 09.20.20)Document2 pagesAssignment - Chapter 2 - Problem 28 (Due 09.20.20)Tenaj KramNo ratings yet

- Decision making_ sol_IMT5Document9 pagesDecision making_ sol_IMT5loyetic600No ratings yet

- Computation of Total Income & Tax LiabilityDocument24 pagesComputation of Total Income & Tax LiabilityKartikNo ratings yet

- Income Tax Calculation SheetDocument8 pagesIncome Tax Calculation SheetArajrubanNo ratings yet

- Practice-Problem-24-25Document2 pagesPractice-Problem-24-25shaineemaezamoraNo ratings yet

- Corporate Tax Planning & Management - M. Com III - AS 2374Document9 pagesCorporate Tax Planning & Management - M. Com III - AS 2374ranu28322No ratings yet

- Business Taxation SolutionDocument3 pagesBusiness Taxation SolutionBillie MatchocaNo ratings yet

- ANSWER KEY Quiz On Tax On Compensation PDFDocument6 pagesANSWER KEY Quiz On Tax On Compensation PDFMeg CruzNo ratings yet

- Business Budgetting Assignment - Noah MzyeceDocument10 pagesBusiness Budgetting Assignment - Noah MzyeceNoah MzyeceNo ratings yet

- Income Tax - Corporations Sample Problems: SolutionsDocument12 pagesIncome Tax - Corporations Sample Problems: SolutionsYellow BelleNo ratings yet

- Financial Management NPVDocument8 pagesFinancial Management NPVAnaNo ratings yet

- Direct Rax CodeDocument14 pagesDirect Rax CodedivajainNo ratings yet

- Afar JNDocument2 pagesAfar JNjasonnumahnalkelNo ratings yet

- 8.2 Assignment - Regular Income Tax For Individuals (For Discussion)Document8 pages8.2 Assignment - Regular Income Tax For Individuals (For Discussion)Roselyn LumbaoNo ratings yet

- Oracle Application's Blog - 21 Most Important Oracle r12 Payables Interview QuestionsDocument5 pagesOracle Application's Blog - 21 Most Important Oracle r12 Payables Interview Questionssreenivas.oracle08No ratings yet

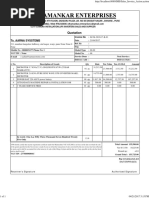

- Aarna Systemes PDFDocument1 pageAarna Systemes PDFSunil DhamankarNo ratings yet

- Proforma Invoice - Harka - PI - Har.22.11.2023 - Qu416265 - Inc VATDocument2 pagesProforma Invoice - Harka - PI - Har.22.11.2023 - Qu416265 - Inc VATMahamane TouréNo ratings yet

- 121 3 1000125009Document9 pages121 3 1000125009Rehana AzeemNo ratings yet

- Tally Erp 9.0 Material Tax Collected at Source Tally Erp 9.0Document25 pagesTally Erp 9.0 Material Tax Collected at Source Tally Erp 9.0Raghavendra yadav KMNo ratings yet

- Import Payment Covering Letter and A1 FormatDocument4 pagesImport Payment Covering Letter and A1 Formatgan_muruNo ratings yet

- HDD InvoiceDocument1 pageHDD Invoicearun rayakwarNo ratings yet

- Export Import Magic ImpexDocument17 pagesExport Import Magic ImpexVishal VirolaNo ratings yet

- CBRE-ATT - Vendor Training (WON - Work Order Network) 5-20-14Document48 pagesCBRE-ATT - Vendor Training (WON - Work Order Network) 5-20-14donelly1976No ratings yet

- Project ReportDocument30 pagesProject Reportkeqra100% (1)

- MM QuestionnaireDocument8 pagesMM QuestionnaireCABUTOTAN100% (2)

- Indirect Taxes QP-2Document3 pagesIndirect Taxes QP-2Venkatesh PrabhuNo ratings yet

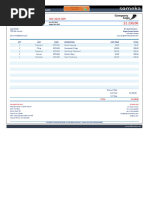

- InvoiceDocument1 pageInvoicewasu sheebuNo ratings yet

- GoAir S42SFIDocument1 pageGoAir S42SFISabyasachi KarNo ratings yet

- DRC VAT Training CAs Day 1-2Document40 pagesDRC VAT Training CAs Day 1-2iftekharul alam100% (2)

- Billing Address:: Bill InvoiceDocument2 pagesBilling Address:: Bill InvoiceHathiram NenavathNo ratings yet

- Invoice 1447 From LDK ElectricalDocument1 pageInvoice 1447 From LDK ElectricalJason GoddardNo ratings yet

- BBP New Sap FicoDocument109 pagesBBP New Sap Ficoalisnowkiss657075% (4)

- Accounting Entries For MMDocument5 pagesAccounting Entries For MMJim D'souza25% (4)

- Proforma Invoice: Product UOM Quantity Unit Weight (In KG) Total Wt:Kgs Unit Price Inc Total Price IncDocument1 pageProforma Invoice: Product UOM Quantity Unit Weight (In KG) Total Wt:Kgs Unit Price Inc Total Price Incrox odhiamboNo ratings yet

- Dental Invoice Template Someka Example PDF V1Document1 pageDental Invoice Template Someka Example PDF V1Albert A. KayNo ratings yet

- Air Canada V CirDocument15 pagesAir Canada V CirArmstrong BosantogNo ratings yet

- Credit Invoice TNDocument57 pagesCredit Invoice TNPithakarasNo ratings yet

- Peoplesoft Inventory CostingDocument36 pagesPeoplesoft Inventory Costingjaish2No ratings yet

- 00-C-WS-L-0782 Extension of Time (EOT) Relevant Costs Claim - C PDFDocument5 pages00-C-WS-L-0782 Extension of Time (EOT) Relevant Costs Claim - C PDFCandy EmanNo ratings yet

- Merchandising Entity StudentsDocument34 pagesMerchandising Entity StudentsJenny AstroNo ratings yet

- Scrisori BusinessDocument8 pagesScrisori BusinessOana-AlexandraNo ratings yet

- Substantive Procedures SheetDocument28 pagesSubstantive Procedures SheetMohanrajNo ratings yet

- Everything About ArtDocument88 pagesEverything About ArtRavinder SIngh0% (1)