Unit I

Unit I

Download as docx, pdf, or txt

You might also like

- Central Bureau of Investigation (India) ListDocument312 pagesCentral Bureau of Investigation (India) ListSrinath ParthaNo ratings yet

- Banking Laws Course SyllabusDocument4 pagesBanking Laws Course SyllabusJaimie Lyn TanNo ratings yet

- Introduction To Banking Full NoteDocument46 pagesIntroduction To Banking Full Notedeekshithshetty996No ratings yet

- Chapter 1: Introduction 1.1 Meaning and Definition of BankDocument6 pagesChapter 1: Introduction 1.1 Meaning and Definition of BankdineshNo ratings yet

- Submitted To: Submitted By: Mrs. Sumeet Kaur Srishti Pahwa Professor-G.G.D.S.D College, Sem. Chandigarh Roll No-1515021Document7 pagesSubmitted To: Submitted By: Mrs. Sumeet Kaur Srishti Pahwa Professor-G.G.D.S.D College, Sem. Chandigarh Roll No-1515021radhika marwahNo ratings yet

- Banking Innovation.: EtymologyDocument78 pagesBanking Innovation.: EtymologyFaisal AnsariNo ratings yet

- The Project On Pragathi BankDocument85 pagesThe Project On Pragathi BankPrashanth PBNo ratings yet

- What Is A Bank ? Introduction: - CrowtherDocument29 pagesWhat Is A Bank ? Introduction: - CrowtherHarbrinder GurmNo ratings yet

- Chapter - 01 Introduction of BankDocument37 pagesChapter - 01 Introduction of BankJeeva JeevaNo ratings yet

- FinalDocument21 pagesFinalArjun MishraNo ratings yet

- Introduction To Banking: The Indian Baking Can Be Broadly Categorized IntoDocument12 pagesIntroduction To Banking: The Indian Baking Can Be Broadly Categorized IntoNaveen GowdaNo ratings yet

- Banking Awareness BasicsDocument21 pagesBanking Awareness BasicsAbhijit WankhedeNo ratings yet

- Project On Andhra Bank: Chapter: 1. Introduction of BankDocument47 pagesProject On Andhra Bank: Chapter: 1. Introduction of BankMukesh ManwaniNo ratings yet

- Anitha HDFCDocument84 pagesAnitha HDFCchaluvadiinNo ratings yet

- Impact of Gloablisationon Indian Banking SectorDocument48 pagesImpact of Gloablisationon Indian Banking SectorVicky MishraNo ratings yet

- Final Copy 1Document15 pagesFinal Copy 1gagana sNo ratings yet

- Ma If - Theory and Practice of Modern BankingDocument94 pagesMa If - Theory and Practice of Modern Bankingpersonalacc22197No ratings yet

- What Is A Payment Bank PDFDocument76 pagesWhat Is A Payment Bank PDFsmithNo ratings yet

- Banking and InsuranceDocument11 pagesBanking and InsuranceGanpat SoundaleNo ratings yet

- 1 BK XI I 2019 - StudentsDocument60 pages1 BK XI I 2019 - Studentssneha.ss1411No ratings yet

- Indian Bank - All ChaptersDocument109 pagesIndian Bank - All ChaptersRAMAKRISHNANNo ratings yet

- Banking Industry: Definition of BankDocument10 pagesBanking Industry: Definition of BankNikhitha ShettyNo ratings yet

- OutsourcingDocument55 pagesOutsourcingNagesh More100% (1)

- Banking Sector in India 1, 2 & 3Document19 pagesBanking Sector in India 1, 2 & 3Sk HossainNo ratings yet

- Banking TheoryDocument299 pagesBanking TheoryMohammedNo ratings yet

- Content (Kiran)Document67 pagesContent (Kiran)Omkar ChavanNo ratings yet

- Banking and Working System of BanksDocument25 pagesBanking and Working System of BanksMohitJangidNo ratings yet

- BankinglawDocument86 pagesBankinglawrahul singhNo ratings yet

- DISSERTATION Finance PGDMDocument29 pagesDISSERTATION Finance PGDMnupur sarkarNo ratings yet

- RakshaDocument8 pagesRakshabruceleechain00No ratings yet

- 35 Modernization and Innovation in Banking Sector Repaired)Document85 pages35 Modernization and Innovation in Banking Sector Repaired)Hema Golani100% (2)

- Brief History of Banking in IndiaDocument53 pagesBrief History of Banking in IndiaLove NijaiNo ratings yet

- Types of Bank DepositsDocument55 pagesTypes of Bank DepositsrocksonNo ratings yet

- Introduction To BankingDocument6 pagesIntroduction To BankingGraciously meNo ratings yet

- ReportDocument102 pagesReportchsibiNo ratings yet

- Sbaa 7001Document221 pagesSbaa 7001rishijain9h1No ratings yet

- Introduction To Ozone Layer DepletionDocument35 pagesIntroduction To Ozone Layer DepletionPlease let me knowNo ratings yet

- Chapter:-1 Introduction of BankDocument54 pagesChapter:-1 Introduction of BankOmkar ChavanNo ratings yet

- Q1 Banking 1Document18 pagesQ1 Banking 1Adarsh ShetNo ratings yet

- An Overview of Banking Industry - Unit I: Lecture Notes SeriesDocument28 pagesAn Overview of Banking Industry - Unit I: Lecture Notes SeriesGame ProfileNo ratings yet

- Finance ProjectDocument61 pagesFinance Projecthiren9090No ratings yet

- JANKIDocument47 pagesJANKIJankiNo ratings yet

- Research PaperDocument43 pagesResearch PaperJankiNo ratings yet

- Ifs Cia 3Document11 pagesIfs Cia 3Rohit GoyalNo ratings yet

- Chapter - 1 Introduction To Commercial BankingDocument26 pagesChapter - 1 Introduction To Commercial BankingMd Mohsin AliNo ratings yet

- Union Bank of IndiaDocument58 pagesUnion Bank of Indiadivyesh_variaNo ratings yet

- A Project Report On: Under The Supervision Of: Submitted By: MD - SageerDocument46 pagesA Project Report On: Under The Supervision Of: Submitted By: MD - Sageerdev42No ratings yet

- Comparative Between Commercial Bank and Co Operative BankDocument39 pagesComparative Between Commercial Bank and Co Operative BankSoundari Nadar100% (3)

- Union Bank of IndiaDocument58 pagesUnion Bank of IndiaRakesh Prabhakar ShrivastavaNo ratings yet

- Project On Bank of IndiaDocument57 pagesProject On Bank of IndiaShweta Yashwant Chalke0% (1)

- Banking Law NotesDocument28 pagesBanking Law NotesSarim FazliNo ratings yet

- Banking Law NotesDocument8 pagesBanking Law NotesGeetika DhamaNo ratings yet

- Review of LiteratureDocument65 pagesReview of LiteratureRUTUJA PATILNo ratings yet

- Review of LiteratureDocument64 pagesReview of LiteratureRUTUJA PATILNo ratings yet

- Pooja RakshaDocument28 pagesPooja Rakshabruceleechain00No ratings yet

- BANKING MODULE (Study Material) PDFDocument63 pagesBANKING MODULE (Study Material) PDFSupriyo GhoshNo ratings yet

- Banking 2Document24 pagesBanking 2bishnu paudelNo ratings yet

- MBFI NotesDocument27 pagesMBFI NotesSrikanth Prasanna BhaskarNo ratings yet

- Unit 2 Banking Innovations: Evolution of Banking in IndiaDocument8 pagesUnit 2 Banking Innovations: Evolution of Banking in IndiaAnitha RNo ratings yet

- BankingDocument101 pagesBankingvipul5290No ratings yet

- India Bulls Bank Details Updation FormDocument1 pageIndia Bulls Bank Details Updation FormpankajkumarsNo ratings yet

- Investment BankingDocument15 pagesInvestment BankingRahul singhNo ratings yet

- Real-Time Payment System IMPS - Future & ChallengesDocument27 pagesReal-Time Payment System IMPS - Future & ChallengesRahul AminNo ratings yet

- Bank Loan Report Query DocumentDocument3 pagesBank Loan Report Query Documentnikita.salunkhe7997No ratings yet

- Church ResolutionDocument1 pageChurch ResolutionGil Mae Huelar100% (1)

- Vikas Final ProjectDocument54 pagesVikas Final Projectvikas mahajanNo ratings yet

- Black Card Concept by NLEXEDocument4 pagesBlack Card Concept by NLEXEKannada Rapper100% (1)

- Untitled 1Document26 pagesUntitled 1ER SAABNo ratings yet

- PL Cendana Spark - Aug 2023 - Signed (002) Signed RH 26072023Document3 pagesPL Cendana Spark - Aug 2023 - Signed (002) Signed RH 26072023Cindy PermatasariNo ratings yet

- Lodones Copy5Document2 pagesLodones Copy5Cristine GonzalesNo ratings yet

- Comparative Analysis of SBI & HDFC BankDocument101 pagesComparative Analysis of SBI & HDFC BankArvind Mahandhwal73% (55)

- 96th RMFI Questions AnalysisDocument4 pages96th RMFI Questions Analysischayon mondolNo ratings yet

- 1 Chinese Yen in Rupees - Google SearchDocument1 page1 Chinese Yen in Rupees - Google Searchvidhya_jeevaNo ratings yet

- Cash-And-Cash-Equivalent - Answers On HandoutDocument6 pagesCash-And-Cash-Equivalent - Answers On HandoutElaine AntonioNo ratings yet

- Akw 104 Accounting & Finance Lecture 4: Cash & Internal ControlDocument17 pagesAkw 104 Accounting & Finance Lecture 4: Cash & Internal ControlmuitsNo ratings yet

- Project On "Credit Appraisal System in Banks": Project Guide: Prof. Samveg PatelDocument16 pagesProject On "Credit Appraisal System in Banks": Project Guide: Prof. Samveg PatelHarshil BadaniNo ratings yet

- HF 0 Eqhk 2 SB AZWezqDocument5 pagesHF 0 Eqhk 2 SB AZWezqRaju BhaiNo ratings yet

- Aml Templates From Transparint, LLCDocument8 pagesAml Templates From Transparint, LLCEmil AbrahamyanNo ratings yet

- Bank Al Habib HistoryDocument3 pagesBank Al Habib HistoryTalha Abdul RaufNo ratings yet

- BOM DEP STMT XXXXXXXX6029 153416Document14 pagesBOM DEP STMT XXXXXXXX6029 153416rgdtpdhdkpNo ratings yet

- FSBL Makes Advances To Different Sectors For Different Purposes. They Are As FollowsDocument5 pagesFSBL Makes Advances To Different Sectors For Different Purposes. They Are As FollowsRajib DattaNo ratings yet

- 2020 Chapter 3 Audit of Cash Student GuideDocument29 pages2020 Chapter 3 Audit of Cash Student GuideBeert De la CruzNo ratings yet

- Account Statement: Penyata AkaunDocument2 pagesAccount Statement: Penyata AkaunMr HaiFadzNo ratings yet

- GK-1 - Bank & Banking Related GK by Engineer's BCS CareDocument10 pagesGK-1 - Bank & Banking Related GK by Engineer's BCS Caresuhajanan16No ratings yet

- Institute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingDocument3 pagesInstitute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingS100% (2)

- TD Bank StatementDocument3 pagesTD Bank StatementRoger kellyNo ratings yet

- Fess 1 PsDocument13 pagesFess 1 Psvinod maddikeraNo ratings yet

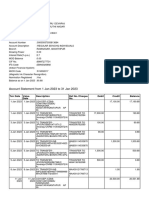

- Customer StatementDocument1 pageCustomer StatementWasim AhmedNo ratings yet