The Amato Theater is preparing for a loan renewal meeting with its bankers. The trial balance from December 31, 2015 is presented, along with additional financial information. Adjusting journal entries are necessary to properly account for depreciation, interest, unearned revenue, advertising, and salaries. Without the adjustments, Amato's income and current assets/liabilities would be misstated, affecting the bankers' evaluation. While bankers want more frequent reports, shorter periods reduce reliability as determining proper net income is difficult and errors more likely, balancing relevance with faithful representation.

The Amato Theater is preparing for a loan renewal meeting with its bankers. The trial balance from December 31, 2015 is presented, along with additional financial information. Adjusting journal entries are necessary to properly account for depreciation, interest, unearned revenue, advertising, and salaries. Without the adjustments, Amato's income and current assets/liabilities would be misstated, affecting the bankers' evaluation. While bankers want more frequent reports, shorter periods reduce reliability as determining proper net income is difficult and errors more likely, balancing relevance with faithful representation.

The Amato Theater is preparing for a loan renewal meeting with its bankers. The trial balance from December 31, 2015 is presented, along with additional financial information. Adjusting journal entries are necessary to properly account for depreciation, interest, unearned revenue, advertising, and salaries. Without the adjustments, Amato's income and current assets/liabilities would be misstated, affecting the bankers' evaluation. While bankers want more frequent reports, shorter periods reduce reliability as determining proper net income is difficult and errors more likely, balancing relevance with faithful representation.

The Amato Theater is preparing for a loan renewal meeting with its bankers. The trial balance from December 31, 2015 is presented, along with additional financial information. Adjusting journal entries are necessary to properly account for depreciation, interest, unearned revenue, advertising, and salaries. Without the adjustments, Amato's income and current assets/liabilities would be misstated, affecting the bankers' evaluation. While bankers want more frequent reports, shorter periods reduce reliability as determining proper net income is difficult and errors more likely, balancing relevance with faithful representation.

Download as DOCX, PDF, TXT or read online from Scribd

Download as docx, pdf, or txt

You are on page 1/ 3

2.

Accounting, Analysis, and Principles

The Amato Theater is nearing the end of the year and is preparing for a meeting with its bankers to discuss the renewal of a loan. The accounts listed appeared in the December 31, 2015, trial balance as follows:

1. The equipment has an estimated useful life of 16 years and a residual value of £40,000 at the end of that time. Amato uses the straight-line method for depreciation. 2. The note payable is a one-year note given to the bank January 31 and bearing interest at 10%. Interest is calculated on a monthly basis. 3. The theater sold 350 coupon ticket books at £50 each. Two hundred ticket books were used in 2015. One hundred fifty of these ticket books can be used only for admission any time after January 1, 2016. The cash received was recorded as Unearned Service Revenue. 4. Advertising paid in advance was £6,000 and was debited to Prepaid Advertising. The company has used £2,500 of the advertising as of December 31, 2015. 5. Salaries and wages accrued but unpaid at December 31, 2015, were £3,500.

Accounting Prepare any adjusting journal entries necessary for the year ended December 31, 2015.

Answer:

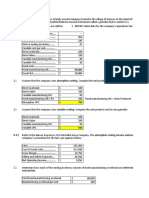

Date Accounts and Explanation Debit (£) Credit (£)

Interest Payable 8,250 (£90,000 x 10%) x 11/12 = £8,250)

31 Dec 2015 Unearned Service Revenue 10,000

Service Revenue 10,000 200 x £50 = £10,000 31 Dec 2015 Advertising Expense 2,500

Prepaid Advertising 2,500

31 Dec 2015 Salaries and Wages Expense 3,500

Salaries and Wages Payable 3,500

£33,750 £33,750

Both sides of the journal total $33,750.

The net income of the business entity is overstated when adjusting entries are not made. Reporting financial information frequently to users will increase the relevance of the financial statements.

Analysis Determine Amato’s income before and after recording the adjusting entries. Use your analysis to explain why Amato’s bankers should be willing to wait for Amato to complete its year-end adjustment process before making a decision on the loan renewal.

Answer:

Income before Income after

Adjustments Adjustments Adjustments Service revenue £360,000 £10,000 £370,000 Depreciation expense (9,500) (9,500) Advertising expense (18,680) (2,500) (21,180) Salaries and Wages expense (67,600) (3,500) (71,100) Interest expense (1,400) (8,250) (9,650) Net income £272,320 £258,570

The loan is provided based on the liquidity position of the business entity. The adjusting entries would correct the misstated balance of the current assets and liabilities. Therefore, the bankers should wait for year-end adjustments. Without recording the adjusting entries, Amato’s income is overstated. In addition, without the adjustments, Amato’s current liabilities and current assets are misstated, which could affect evaluation of Amato’s liquidity. Adjusting entries are required every time a company, prepares financial statements. Adjusting Entries In order for revenues to be recorded in the period in which services are performed and for expenses to be recognized in the period in which they are incurred, companies make adjusting entries. The use of adjusting entries makes it possible to report on the statement of financial position the appropriate assets, liabilities, and equity at the statement date. Adjusting entries also make it possible to report on the income statement the proper revenues and expenses for the period.

Principles Although Amato’s bankers are willing to wait for the adjustment process to be completed before they receive financial information, they would like to receive financial reports more frequently than annually or even quarterly. What trade-offs, in terms of relevance and faithful representation, are inherent is preparing financial statements for shorter accounting time periods?

Answer: The periodicity (or time period) assumption implies that a company can divide its economic activities into artificial time periods. These time periods vary, but the most common are monthly, quarterly, and yearly. The shorter the time period, the more difficult it is to determine the proper net income for the period. A month’s results usually prove less reliable than a quarter’s results, and a quarter’s results are likely to be less reliable than a year’s results. Investor desire and demand that a company quickly process and disseminate information. Yet the quicker a company releases the information, the more likely the information will include errors. The problem of defining the time period becomes more serious as product cycles shorten and products become obsolete more quickly. Many believe that, given technology advances, companies need to provide more online, real-time financial information to ensure the availability of relevant information.