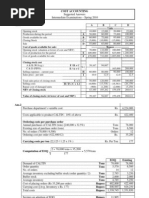

CM121.Solution September-2023 Exam.

CM121.Solution September-2023 Exam.

Download as pdf or txt

You might also like

- CMA Inter Management Accounting - DJB BookDocument166 pagesCMA Inter Management Accounting - DJB BookHitarth shah100% (1)

- Level 3 Costing & MA Text Update June 2021pdfDocument125 pagesLevel 3 Costing & MA Text Update June 2021pdfAmi KayNo ratings yet

- PDF Document 3Document13 pagesPDF Document 3Nina0% (1)

- Cost Accounting 3Document13 pagesCost Accounting 3Frenz VerdidaNo ratings yet

- Management Information - ND2020 - Suggested - AnswersDocument4 pagesManagement Information - ND2020 - Suggested - Answerskawsar alamNo ratings yet

- P1 Solution Dec 2018Document6 pagesP1 Solution Dec 2018Awal ShekNo ratings yet

- Solution CMA January 2022 ExaminationDocument6 pagesSolution CMA January 2022 ExaminationKamrul HassanNo ratings yet

- AFAR Set BDocument11 pagesAFAR Set BRence Gonzales0% (2)

- LEVEL 2 Online Quiz - Answers SET ADocument10 pagesLEVEL 2 Online Quiz - Answers SET AVincent Larrie MoldezNo ratings yet

- Costing Methods and TechniquesDocument4 pagesCosting Methods and TechniquesvishnuprasdhaNo ratings yet

- KCL 2013 Accouting Part B SolutionDocument5 pagesKCL 2013 Accouting Part B SolutionStephanie ImNo ratings yet

- Operation Costing, Just-In-Time System, and Backflush CostingDocument15 pagesOperation Costing, Just-In-Time System, and Backflush CostingJeremy Cyrus TrinidadNo ratings yet

- Cost Classification: Total Product/ ServiceDocument21 pagesCost Classification: Total Product/ ServiceThureinNo ratings yet

- Costing 2 Material - 014417Document40 pagesCosting 2 Material - 014417sirjamtech36No ratings yet

- Job Batch ProcessingDocument6 pagesJob Batch ProcessingIshfaq AhmadNo ratings yet

- Solution: EOQDocument4 pagesSolution: EOQLovely VillasNo ratings yet

- D10 Spring2010Document7 pagesD10 Spring2010meelas123No ratings yet

- CH 3Document19 pagesCH 3hey100% (1)

- CA Inter Cost MTP May22 Hand NotesDocument38 pagesCA Inter Cost MTP May22 Hand Notesvinayakjha57No ratings yet

- Cost and Management Accounting - 231025 - 204341Document277 pagesCost and Management Accounting - 231025 - 204341am.2021.foreverNo ratings yet

- Management Information: Time Allowed-2:15 Hours Total Marks - 100Document2 pagesManagement Information: Time Allowed-2:15 Hours Total Marks - 100Prabir Kumer RoyNo ratings yet

- Midterm Review Workshop ACCT 2230 F23Document42 pagesMidterm Review Workshop ACCT 2230 F23akhurshid2004No ratings yet

- U Win Bo Myint Cost and Management Overhead Homework - 2Document3 pagesU Win Bo Myint Cost and Management Overhead Homework - 2Theint Myat KyalsinNo ratings yet

- Solution CMA May-2023 Exam.Document7 pagesSolution CMA May-2023 Exam.Kamrul HassanNo ratings yet

- Q2 Midterm Cost BSAISDocument3 pagesQ2 Midterm Cost BSAISHannah Zoe MongayaNo ratings yet

- AcaDocument2 pagesAcaAnamicaMahajanNo ratings yet

- CM341. SMA (AL-I) Solution CMA January-2023 Exam.Document4 pagesCM341. SMA (AL-I) Solution CMA January-2023 Exam.Shawn MehdiNo ratings yet

- Acctg523-B1-Practice Midterm-W2022-SolutionDocument8 pagesAcctg523-B1-Practice Midterm-W2022-Solutionmakan94883No ratings yet

- 102.COAP - .L I Question CMA JUNE 2020 ExamDocument3 pages102.COAP - .L I Question CMA JUNE 2020 Examrumelrashid_seuNo ratings yet

- CM231. MAC Solution CMA January 2022 ExaminationDocument6 pagesCM231. MAC Solution CMA January 2022 ExaminationrifatNo ratings yet

- 12 CasDocument7 pages12 CasLakshay SharmaNo ratings yet

- RUNNING HEAD: Accounting Questions 1Document6 pagesRUNNING HEAD: Accounting Questions 1Chirayu ThapaNo ratings yet

- Assgnment 2 (f5) 10341Document11 pagesAssgnment 2 (f5) 10341Minhaj AlbeezNo ratings yet

- End Answers Chapter 2,3,4,7-1 Managerial Accounting Hilton PlattDocument14 pagesEnd Answers Chapter 2,3,4,7-1 Managerial Accounting Hilton PlattShivani TannuNo ratings yet

- 06 Cost Accounting System FTDocument18 pages06 Cost Accounting System FTnsm2zmvnbbNo ratings yet

- Ch13 Homework Assignment W24Document18 pagesCh13 Homework Assignment W24m.espinoza.plazaNo ratings yet

- Answers To Test Your Understanding: Cost Accounting Chapter 1 Cost Classification, Concepts and TerminologyDocument10 pagesAnswers To Test Your Understanding: Cost Accounting Chapter 1 Cost Classification, Concepts and TerminologyAnonymous vA2xNfNo ratings yet

- CA-Inter-Costing - Anuj-JalotaDocument17 pagesCA-Inter-Costing - Anuj-JalotaSUMANTO BARMANNo ratings yet

- Soultions - Chapter 3Document8 pagesSoultions - Chapter 3Naudia L. TurnbullNo ratings yet

- Unit and Batch Homework SolutionsDocument2 pagesUnit and Batch Homework Solutionsnikhilcoke7No ratings yet

- 102.COAP - .L I Question CMA Special Examination 2021novemberDocument4 pages102.COAP - .L I Question CMA Special Examination 2021novemberleyaketjnuNo ratings yet

- Week 4 PREPARED SOLUTIONS 2023Document7 pagesWeek 4 PREPARED SOLUTIONS 2023unathimsuthu006No ratings yet

- Cost Classification-PQDocument7 pagesCost Classification-PQRomail QaziNo ratings yet

- CM121. COA (IL-I) Solution CMA May-2024 Exam.Document6 pagesCM121. COA (IL-I) Solution CMA May-2024 Exam.farukbhuiyan145No ratings yet

- Absorption (Total) Costing: A2 Level Accounting - Resources, Past Papers, Notes, Exercises & QuizesDocument4 pagesAbsorption (Total) Costing: A2 Level Accounting - Resources, Past Papers, Notes, Exercises & QuizesAung Zaw HtweNo ratings yet

- Fima Week 2 ActivitiesDocument9 pagesFima Week 2 ActivitiesKatrina PaquizNo ratings yet

- Some Worked Out Problems in InventoryDocument6 pagesSome Worked Out Problems in InventoryYERRAMSETTY CHAITANYANo ratings yet

- FYMMS Cost and MA AssignmentDocument2 pagesFYMMS Cost and MA AssignmentRahul Nishad100% (1)

- F2.1 Management Accounting - Answ J2022Document20 pagesF2.1 Management Accounting - Answ J2022NKURUNZIZA FrancoisNo ratings yet

- Joint Products - by ProductsDocument3 pagesJoint Products - by ProductsShivansh NahataNo ratings yet

- MAF Assignment QuestionDocument13 pagesMAF Assignment QuestionKietHuynhNo ratings yet

- Group 3-AC23_ACCA107Document27 pagesGroup 3-AC23_ACCA107Sophia CaceresNo ratings yet

- Solution CMA September 2022 Exam.Document7 pagesSolution CMA September 2022 Exam.Md. Rafiqul IslamNo ratings yet

- MA1 - De thi giua ky - HK2 - 21-22 - send-đã chuyển đổiDocument4 pagesMA1 - De thi giua ky - HK2 - 21-22 - send-đã chuyển đổiThu ThanhNo ratings yet

- Assignment 2Document4 pagesAssignment 2Sahil KumarNo ratings yet

- 2008 Jun TDocument9 pages2008 Jun TGodfrey ChabukaNo ratings yet

- CM121. COA (IL-I) Solution CMA January-2023 Exam.Document7 pagesCM121. COA (IL-I) Solution CMA January-2023 Exam.Shawn MehdiNo ratings yet

- Cash Flow EstimationDocument6 pagesCash Flow EstimationFazul RehmanNo ratings yet

- Combined Past Paper A2.2 PDFDocument123 pagesCombined Past Paper A2.2 PDFSinamenyeNo ratings yet

- Past Papers AllDocument223 pagesPast Papers AllHAGENIMANA JEAN CLAUDENo ratings yet

- Answers To 11 - 16 Assignment in ABC PDFDocument3 pagesAnswers To 11 - 16 Assignment in ABC PDFMubarrach MatabalaoNo ratings yet

- Production and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesFrom EverandProduction and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesNo ratings yet

- (R Ffifr3: (Fu"ffrroDocument2 pages(R Ffifr3: (Fu"ffrroArif HossainNo ratings yet

- Titas Gas Transmission & Distribution Co. Ltd. (A Company of Petrobangla)Document1 pageTitas Gas Transmission & Distribution Co. Ltd. (A Company of Petrobangla)Arif HossainNo ratings yet

- Fiq Ffiftw Fi Rffi: Lgffiu Tffi.Q Dftffift M.L (IDocument3 pagesFiq Ffiftw Fi Rffi: Lgffiu Tffi.Q Dftffift M.L (IArif HossainNo ratings yet

- TA Bill Form NewDocument9 pagesTA Bill Form NewArif HossainNo ratings yet

- Evsjv 'K Cjøx Dbœqb Evw© DC RJV Cjøx Dbœqb Awdmv Ii KVHV©JQ Avgzjx, Ei BV - Cöwkÿ Yi Ågy E Q WeeiyxDocument2 pagesEvsjv 'K Cjøx Dbœqb Evw© DC RJV Cjøx Dbœqb Awdmv Ii KVHV©JQ Avgzjx, Ei BV - Cöwkÿ Yi Ågy E Q WeeiyxArif HossainNo ratings yet

- CM121.Question September-2023 Exam.Document8 pagesCM121.Question September-2023 Exam.Arif HossainNo ratings yet

- 2023 10 31 07 02Document1 page2023 10 31 07 02Arif HossainNo ratings yet

- Absorption Vs Marginal CostingDocument24 pagesAbsorption Vs Marginal CostingPoint BlankNo ratings yet

- Project Report Anand FoodDocument6 pagesProject Report Anand FoodMahesh100% (1)

- Job CostingDocument30 pagesJob Costingzahid_mahmood3811100% (1)

- Managerial Accounting PDFDocument350 pagesManagerial Accounting PDFSalinaNo ratings yet

- HW#2Document12 pagesHW#2Ja RedNo ratings yet

- Monitor and Control Finances: Submission DetailsDocument8 pagesMonitor and Control Finances: Submission Detailsrida zulquarnainNo ratings yet

- ATTACHAKKIDocument2 pagesATTACHAKKIgoutham.lokNo ratings yet

- Soal Asistensi AB Pertemuan 3 - FIXDocument4 pagesSoal Asistensi AB Pertemuan 3 - FIXYusuf FadhillahNo ratings yet

- Accounting Theory Unit 1Document13 pagesAccounting Theory Unit 1Tazrian AliNo ratings yet

- Business Plan Workbook For Students MML 3 3Document46 pagesBusiness Plan Workbook For Students MML 3 3Pudge Pudge'sNo ratings yet

- Cap 5 ContractsDocument18 pagesCap 5 Contractsdannieycandiey44No ratings yet

- Budgetary Control, Mar Cost c0st ST, Res AcDocument29 pagesBudgetary Control, Mar Cost c0st ST, Res AcYashasvi MohandasNo ratings yet

- Cost AccountingDocument13 pagesCost AccountingJoshua Wacangan100% (2)

- Endterm FinmaDocument10 pagesEndterm FinmaMarian Augelio PolancoNo ratings yet

- DupaDocument341 pagesDupaRheyJun Paguinto AnchetaNo ratings yet

- ACT202 - Management AccountingDocument7 pagesACT202 - Management AccountingSHANILA AHMED KHANNo ratings yet

- Some Basic Theory For Cost AccountingDocument16 pagesSome Basic Theory For Cost AccountingNaeem KhanNo ratings yet

- Tax Management and Make - Buy DecisionsDocument12 pagesTax Management and Make - Buy DecisionsYash MittalNo ratings yet

- Answer - Case 1Document10 pagesAnswer - Case 1EVI MARIA SIBUEANo ratings yet

- Decision Making-Limiting FactorDocument4 pagesDecision Making-Limiting FactorMuhammad Azam0% (1)

- Working Capital ManagementDocument7 pagesWorking Capital ManagementEduwiz Mänagemënt EdücatîonNo ratings yet

- Job Cost Sheet - Job J-832-LMDocument2 pagesJob Cost Sheet - Job J-832-LMAbrar Ahmed KhanNo ratings yet

- Cost Accounting MidtermsDocument5 pagesCost Accounting MidtermsJerico Mamaradlo0% (3)

- Vol 2. SampleDocument23 pagesVol 2. SamplevishnuvermaNo ratings yet

- Kuala Lumpur: Answer Sheets: GBHDHFH: 23525: ABMC2054 Cost & Management Accounting IDocument30 pagesKuala Lumpur: Answer Sheets: GBHDHFH: 23525: ABMC2054 Cost & Management Accounting IJUN XIANG NGNo ratings yet

- Cost AccountingDocument16 pagesCost AccountingKezia SantosidadNo ratings yet

- Cost.: Absorption Costing Variable CostingDocument4 pagesCost.: Absorption Costing Variable CostingAngeline RamirezNo ratings yet

- DQI - English WeekDocument3 pagesDQI - English WeekAngie Daniela Muñoz SanchezNo ratings yet