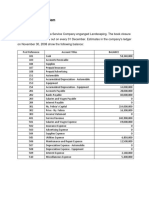

Seminar 8 PART B

Seminar 8 PART B

Download as docx, pdf, or txt

You might also like

- 13 Week Cash Flow ModelDocument16 pages13 Week Cash Flow ModelASChipLeadNo ratings yet

- Ac 4052qa Coursework Augs24 Intake Assignment Brief 01Document2 pagesAc 4052qa Coursework Augs24 Intake Assignment Brief 01collojaiwhiteNo ratings yet

- F 13 Financial Accounting CpaDocument9 pagesF 13 Financial Accounting CpaMarcellin MarcaNo ratings yet

- AC123ASS1Document4 pagesAC123ASS1masiwakalonga28No ratings yet

- Tutorial Questions Cac2101 2021Document13 pagesTutorial Questions Cac2101 2021chibireginabNo ratings yet

- 2023AcF100EXAM1JUNEFINAL AccountingandFSADocument11 pages2023AcF100EXAM1JUNEFINAL AccountingandFSAnikoleta demosthenousNo ratings yet

- Companies Accounting Class Execises - Williams LTDDocument2 pagesCompanies Accounting Class Execises - Williams LTDndilimotuwilika001No ratings yet

- National University of Science and TechnologyDocument8 pagesNational University of Science and TechnologyPATIENCE MUSHONGANo ratings yet

- Classroom Exerisises On Presentation of Financial Statements PDFDocument2 pagesClassroom Exerisises On Presentation of Financial Statements PDFalyssaNo ratings yet

- Lcci - Higher - 2023 - QPDocument18 pagesLcci - Higher - 2023 - QPMUSTHARI KHANNo ratings yet

- BAF 311 BAC 361 Pasts Exam Papers and AnswesDocument47 pagesBAF 311 BAC 361 Pasts Exam Papers and AnswesshayoyaestherNo ratings yet

- Ias 12 Practice QuestionsDocument9 pagesIas 12 Practice QuestionsKeith P. KatsandeNo ratings yet

- Bcac 321 Cat OneDocument2 pagesBcac 321 Cat OneMichael BwireNo ratings yet

- Cuac208 Tests and AssignmentsDocument8 pagesCuac208 Tests and AssignmentsInnocent GwangwaraNo ratings yet

- Test 3 2020Document4 pagesTest 3 2020zuludennischibweya1No ratings yet

- BSC (Hons) Financial Services (General) : Cohort: Bfsg/08/Ft - Year 1 Examinations For 2008 - 2009 Semester IiDocument8 pagesBSC (Hons) Financial Services (General) : Cohort: Bfsg/08/Ft - Year 1 Examinations For 2008 - 2009 Semester Iipriyadarshini212007No ratings yet

- RV102 Semester Test 2 Question 7 October 2022Document5 pagesRV102 Semester Test 2 Question 7 October 2022kgomotsofmatabaneNo ratings yet

- University of Bradford Financial Accounting, Afe5008-B Final ExaminationDocument9 pagesUniversity of Bradford Financial Accounting, Afe5008-B Final ExaminationDiana TuckerNo ratings yet

- LatihanDocument7 pagesLatihanDeny WilyartaNo ratings yet

- Name: Dao Mai Linh Class: F13B ID NUMBER: F13-127Document30 pagesName: Dao Mai Linh Class: F13B ID NUMBER: F13-127Linhzin LinhzinNo ratings yet

- Business+Finance Projected+Financial+StatementsDocument5 pagesBusiness+Finance Projected+Financial+StatementsRaiza FayeNo ratings yet

- P1 - ReviewDocument14 pagesP1 - ReviewEvitaAyneMaliñanaTapit0% (2)

- MOJAKOE AK1 UTS 2012 GasalDocument15 pagesMOJAKOE AK1 UTS 2012 GasalVincenttio le CloudNo ratings yet

- FAR - Final Preboard CPAR 92Document14 pagesFAR - Final Preboard CPAR 92joyhhazelNo ratings yet

- 301 AFA II PL III Question CMA June 2021 Exam.Document4 pages301 AFA II PL III Question CMA June 2021 Exam.rumelrashid_seuNo ratings yet

- Question 2 - MFAC73116 Class Parctice - Cash FlowDocument2 pagesQuestion 2 - MFAC73116 Class Parctice - Cash Flowbonolo.moilweNo ratings yet

- PDE4232 Individual Coursework - 2023-24 UpdatedDocument5 pagesPDE4232 Individual Coursework - 2023-24 UpdatedTariq KhanNo ratings yet

- Hba 2302 Advanced TaxationDocument4 pagesHba 2302 Advanced TaxationprescoviaNo ratings yet

- ADVANCED FINANCIAL REPORTING - PDF Nov 2012Document10 pagesADVANCED FINANCIAL REPORTING - PDF Nov 2012Nitin ChoudharyNo ratings yet

- Maf5101 Financial Accounting I Eve SuppDocument6 pagesMaf5101 Financial Accounting I Eve Suppshobasabria187No ratings yet

- CAC1201201008 Financial Accounting 1BDocument6 pagesCAC1201201008 Financial Accounting 1Bnyasha gundaniNo ratings yet

- ACC311 July 2017Document4 pagesACC311 July 2017Sunday NgbokiNo ratings yet

- Cases Chapter 5Document2 pagesCases Chapter 5Rifqi FarhanNo ratings yet

- Accounting Paper One Revision - 13 November 2024Document12 pagesAccounting Paper One Revision - 13 November 2024iHancoNo ratings yet

- Chapter 9Document23 pagesChapter 9TouseefsabNo ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan Brohi100% (1)

- Financial Accounting 19 PDF FreeDocument6 pagesFinancial Accounting 19 PDF FreeLyka Kristine Jane PacardoNo ratings yet

- FIA142 Cash Flows - Companies - Revision Exercise - 2024 Class SessionDocument11 pagesFIA142 Cash Flows - Companies - Revision Exercise - 2024 Class Sessionthimnabomvana3No ratings yet

- L1-June 2013-FINANCIAL REPORTINGDocument25 pagesL1-June 2013-FINANCIAL REPORTINGMetick MicaiahNo ratings yet

- CAFM FULL SYLLABUS FREE TEST DEC 23-Executive-RevisionDocument7 pagesCAFM FULL SYLLABUS FREE TEST DEC 23-Executive-Revisionyogeetha saiNo ratings yet

- T Fraser, Motif and Meath Cash Flow QuestionsDocument5 pagesT Fraser, Motif and Meath Cash Flow Questionschalah DeriNo ratings yet

- FAR Final Exam - QuestionnaireDocument10 pagesFAR Final Exam - QuestionnairemavsgamingguildNo ratings yet

- Case StudyDocument3 pagesCase Study203560No ratings yet

- Chapter 1 11 IA3Document10 pagesChapter 1 11 IA3ZicoNo ratings yet

- Financial Accounting 2 Assignment 1 2020 PDFDocument7 pagesFinancial Accounting 2 Assignment 1 2020 PDFclaudiogiro23No ratings yet

- Ac208 2019 11Document6 pagesAc208 2019 11brian mgabi100% (1)

- Socf Ii SMNR Q Q2.1. The Financial Reports of Jim LTD For The Years Ended 31 March 2007 andDocument2 pagesSocf Ii SMNR Q Q2.1. The Financial Reports of Jim LTD For The Years Ended 31 March 2007 andTakudzwa LanceNo ratings yet

- Sole Trader - Final Accounts: The Following Trial Balance Was Extracted From The Books of K. Kelly On 31/12/2005Document8 pagesSole Trader - Final Accounts: The Following Trial Balance Was Extracted From The Books of K. Kelly On 31/12/2005MahmozNo ratings yet

- I1.2-Financial Reporting QPDocument8 pagesI1.2-Financial Reporting QPConstantin NdahimanaNo ratings yet

- Ias-07Document15 pagesIas-07Abu SufyanNo ratings yet

- PDFDocument6 pagesPDFjoshua yakubuNo ratings yet

- Cash FlowsDocument18 pagesCash FlowsTamlyn MaistryNo ratings yet

- Test 1Document3 pagesTest 1tshepomoejanejrNo ratings yet

- Mba ZC415 Ec-3r First Sem 2022-2023Document4 pagesMba ZC415 Ec-3r First Sem 2022-2023Ravi KaviNo ratings yet

- National University of Science and TechnologyDocument5 pagesNational University of Science and TechnologyPATIENCE MUSHONGANo ratings yet

- 3rd Year Diagnostic TestDocument11 pages3rd Year Diagnostic TestRaizell Jane Masiglat CarlosNo ratings yet

- ExercisesDocument20 pagesExercisesRolivhuwaNo ratings yet

- The Following Trial Balance Was Extracted From The Books of Craz LTD As at 31 Dec 2014Document5 pagesThe Following Trial Balance Was Extracted From The Books of Craz LTD As at 31 Dec 2014Pham TrangNo ratings yet

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Lecture 6 - Working Capital Management 1Document19 pagesLecture 6 - Working Capital Management 1Gaba RieleNo ratings yet

- Tutorial 9 & 10 Control AccountsDocument3 pagesTutorial 9 & 10 Control AccountsGaba RieleNo ratings yet

- Tutorial 9 & 10 Control Accounts CorrectedDocument4 pagesTutorial 9 & 10 Control Accounts CorrectedGaba RieleNo ratings yet

- Tutorial 7-Bank ReconcilliationDocument2 pagesTutorial 7-Bank ReconcilliationGaba RieleNo ratings yet

- Seminar 1 AnswersDocument3 pagesSeminar 1 AnswersGaba RieleNo ratings yet

- Topic 2 - Equity 1 AnsDocument6 pagesTopic 2 - Equity 1 AnsGaba RieleNo ratings yet

- Phineas 27Document42 pagesPhineas 27Gaba Riele100% (2)

- Topic 4 - Debt Ans 2019-20Document4 pagesTopic 4 - Debt Ans 2019-20Gaba RieleNo ratings yet

- An Application For Fixation of Standard RentDocument2 pagesAn Application For Fixation of Standard RentPalash Banerjee100% (1)

- UAP HoldingsDocument5 pagesUAP HoldingsGiselle Esguerra ManansalaNo ratings yet

- ACK877781380300723 Jainendra JainDocument1 pageACK877781380300723 Jainendra Jaintusharjain247No ratings yet

- q2 Illustrating Simple and Compound InterestDocument66 pagesq2 Illustrating Simple and Compound Interestkinggilgamesh820No ratings yet

- Gross Domestic ProductDocument8 pagesGross Domestic ProductNiño Rey LopezNo ratings yet

- EASC345 Tutorial 5Document11 pagesEASC345 Tutorial 5DANDII SO SicKNo ratings yet

- Foundations of Finance - Final Prac Exam 1Document12 pagesFoundations of Finance - Final Prac Exam 1xuechengbo0502No ratings yet

- The Life Cycle of Private EquityDocument3 pagesThe Life Cycle of Private EquitydapijNo ratings yet

- Residential: Information Deemed Reliable, Not Verified or GuaranteedDocument1 pageResidential: Information Deemed Reliable, Not Verified or GuaranteedJude Thomas SmithNo ratings yet

- C3 Accounting & Information SystemDocument22 pagesC3 Accounting & Information SystemSteeeeeeeephNo ratings yet

- Farrari Case StudyDocument24 pagesFarrari Case StudyUmair JanNo ratings yet

- Amity Law School, Noida: Shelf Prospectus and Red Herring ProspectusDocument5 pagesAmity Law School, Noida: Shelf Prospectus and Red Herring ProspectusadititopperNo ratings yet

- QDP CommunicationDocument2 pagesQDP CommunicationbuddhindraNo ratings yet

- BBA Program StructureDocument12 pagesBBA Program StructureMd AbdullahNo ratings yet

- CH 5 PART 2 Guest Accounting ModuleDocument26 pagesCH 5 PART 2 Guest Accounting ModuleNurul AliahNo ratings yet

- Project For Audit, BBA STUDENTSDocument175 pagesProject For Audit, BBA STUDENTSrb2863578No ratings yet

- Philippine National Bank Vs Lilibeth ChanDocument14 pagesPhilippine National Bank Vs Lilibeth ChanJoatham GenovisNo ratings yet

- What Does REHABILITATION MeanDocument23 pagesWhat Does REHABILITATION MeanMaLizaCainapNo ratings yet

- Pre Final Reviewer Ais 3Document3 pagesPre Final Reviewer Ais 3kaialesterfieroNo ratings yet

- Pakistan Salary Income Tax Calculator Tax Year 2021 2022Document4 pagesPakistan Salary Income Tax Calculator Tax Year 2021 2022Kashif NiaziNo ratings yet

- Floresca V Evangelista 96 SCRA 130Document2 pagesFloresca V Evangelista 96 SCRA 130yannie isananNo ratings yet

- Payment Options: Online Banking - Highly RecommendedDocument1 pagePayment Options: Online Banking - Highly RecommendedMEET SHAHNo ratings yet

- Bitcoin (BTC) Price Prediction 2022 - 2030 According To The Crypto ExpertsDocument1 pageBitcoin (BTC) Price Prediction 2022 - 2030 According To The Crypto Expertssanyshah0No ratings yet

- Famba6e Quiz Solutions Apxb 012315Document2 pagesFamba6e Quiz Solutions Apxb 012315kala_kawyaNo ratings yet

- United Utilities Case SolutionDocument11 pagesUnited Utilities Case SolutionAfrin JahanNo ratings yet

- Acct Statement - XX0101 - 21082023Document7 pagesAcct Statement - XX0101 - 21082023apocryphonraNo ratings yet

- HO1 Problems and ExercisesDocument2 pagesHO1 Problems and ExercisesGuiana WacasNo ratings yet

- Csec Poa Paper3 Jan2015 PDFDocument8 pagesCsec Poa Paper3 Jan2015 PDFaellaniNo ratings yet

- Approaches To International CompensationDocument20 pagesApproaches To International CompensationDhwani Shah100% (4)

- Chapter 2 Insurance and Risk PDFDocument19 pagesChapter 2 Insurance and Risk PDFKRZ. Arpon Root HackerNo ratings yet