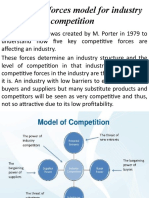

Porter Analysis: Threat of New Entrants

Porter Analysis: Threat of New Entrants

Download as docx, pdf, or txt

You might also like

- Porter's Five Forces: Understand competitive forces and stay ahead of the competitionFrom EverandPorter's Five Forces: Understand competitive forces and stay ahead of the competitionRating: 4 out of 5 stars4/5 (10)

- How Competitive Forces Shape StrategyDocument11 pagesHow Competitive Forces Shape StrategyErwinsyah RusliNo ratings yet

- Supermarket Industry PorterDocument5 pagesSupermarket Industry PorterMiklós BarnabásNo ratings yet

- Industry Analysis: Positioning The Firm Within The Specific EnvironmentDocument12 pagesIndustry Analysis: Positioning The Firm Within The Specific EnvironmentJann Aldrin Pula100% (1)

- Consulting Interview Case Preparation: Frameworks and Practice CasesFrom EverandConsulting Interview Case Preparation: Frameworks and Practice CasesNo ratings yet

- Competing Against Time: How Time-Based Competition is Reshaping Global MarFrom EverandCompeting Against Time: How Time-Based Competition is Reshaping Global MarRating: 4 out of 5 stars4/5 (9)

- Red Brand CannersDocument2 pagesRed Brand Cannersprateek_goyal20910% (1)

- Opportunities & Threats - Analyzing The External EnvironmentDocument4 pagesOpportunities & Threats - Analyzing The External EnvironmentMaeNo ratings yet

- External Analysis: The Identification of Opportunities and ThreatsDocument16 pagesExternal Analysis: The Identification of Opportunities and Threatsfaria tabassum anikaNo ratings yet

- Business EnvironmentDocument22 pagesBusiness Environmentgetcultured69No ratings yet

- Porter's 5 ForcesDocument15 pagesPorter's 5 ForcesGolan MehtaNo ratings yet

- The External EnvironmentDocument6 pagesThe External EnvironmentLovely De CastroNo ratings yet

- Reviewquestion Chapter5 Group5Document7 pagesReviewquestion Chapter5 Group5Linh Bảo BảoNo ratings yet

- Group 1Document16 pagesGroup 1priyanka srivastavaNo ratings yet

- Industry AnalysisDocument25 pagesIndustry AnalysisPrashant Tejwani100% (1)

- The Structural Analysis of IndustriesDocument6 pagesThe Structural Analysis of IndustriesAnonymous B59wYX4EhNo ratings yet

- Porter's 5 ForcesDocument16 pagesPorter's 5 ForcesSamir ParikhNo ratings yet

- Porter's 5 ForcesDocument16 pagesPorter's 5 ForcesAnjali SaigalNo ratings yet

- Porters Five Force ModelDocument13 pagesPorters Five Force Modelyuvaraj100% (1)

- Market AnalysisDocument6 pagesMarket AnalysisVincent NdaleNo ratings yet

- Threat of Entry: ReviewDocument4 pagesThreat of Entry: ReviewJerome NaronNo ratings yet

- SBM TSB GRP 6 - Porters 5 ForceDocument27 pagesSBM TSB GRP 6 - Porters 5 ForceShashank BhootraNo ratings yet

- Chapter 3-External AnalysisDocument18 pagesChapter 3-External AnalysisMd. Rashed Kamal 221-45-042No ratings yet

- Porters Five Forces Model For Industry CompetitionDocument15 pagesPorters Five Forces Model For Industry CompetitionShahid ChuhdryNo ratings yet

- Case Study: Competitive ForcesDocument3 pagesCase Study: Competitive ForcesArif QureshiNo ratings yet

- Defining An Industry: Strategy: Porter's Five Forces Model: Analysing Industry StructureDocument3 pagesDefining An Industry: Strategy: Porter's Five Forces Model: Analysing Industry StructureSahera KhanNo ratings yet

- The Strategic Planning ProcessDocument39 pagesThe Strategic Planning Processakash0chattoorNo ratings yet

- Developing Strategy Through External AnalysisDocument8 pagesDeveloping Strategy Through External AnalysisDavid GreeneNo ratings yet

- 7bTHE STRATEGIC PLANNING PROCESS, PART 1 & 2Document22 pages7bTHE STRATEGIC PLANNING PROCESS, PART 1 & 2Sakura CnNo ratings yet

- Feb Chap 5Document13 pagesFeb Chap 5gx559953No ratings yet

- Hanger Industry Based On Porter's Five ForcesDocument4 pagesHanger Industry Based On Porter's Five ForcesMuktadirhasanNo ratings yet

- LSE CMC Exploring Strategy Industry and Sector AnalysisDocument32 pagesLSE CMC Exploring Strategy Industry and Sector AnalysisĐinh Hữu NamNo ratings yet

- Portel Five ModelDocument22 pagesPortel Five ModelMuhammad shahNo ratings yet

- Strategy - Chapter 3: Can A Firm Develop Strategies That Influence Industry Structure in Order To Moderate Competition?Document8 pagesStrategy - Chapter 3: Can A Firm Develop Strategies That Influence Industry Structure in Order To Moderate Competition?Tang WillyNo ratings yet

- Industry AnalysisDocument7 pagesIndustry AnalysisNethiyaaRajendranNo ratings yet

- Strama 2Document26 pagesStrama 2Ruby De GranoNo ratings yet

- Red Ocean and Blue Ocean StrategyDocument7 pagesRed Ocean and Blue Ocean StrategySeikh SadiNo ratings yet

- Ranbaxy PorterDocument4 pagesRanbaxy PorterBhanu GuptaNo ratings yet

- Module 2 BAV 30-05-2024Document89 pagesModule 2 BAV 30-05-2024f20210957No ratings yet

- 5 Chapter Industry and Competitor AnalysisDocument10 pages5 Chapter Industry and Competitor AnalysisSuman ChaudharyNo ratings yet

- Industry Life Cycle Analysis BCGDocument6 pagesIndustry Life Cycle Analysis BCGsabbir mahmud sakilNo ratings yet

- Module 3 - Industry AnalysisDocument28 pagesModule 3 - Industry AnalysisJohanna EkbladNo ratings yet

- Strategy: Porter's Five Forces Model: Analysing Industry StructureDocument19 pagesStrategy: Porter's Five Forces Model: Analysing Industry StructureMalsha KularathnaNo ratings yet

- Porter's Five Forces AnalysisDocument3 pagesPorter's Five Forces Analysisvidhit87No ratings yet

- Porter's Five Forces ModelDocument5 pagesPorter's Five Forces ModelPrajakta Gokhale100% (1)

- Chapter 2 The EnvironmentDocument15 pagesChapter 2 The Environmentelio achkarNo ratings yet

- Porter Five Forces PDFDocument9 pagesPorter Five Forces PDFMeepNo ratings yet

- Strategy: Porter's Five Forces Model: Analysing Industry StructureDocument3 pagesStrategy: Porter's Five Forces Model: Analysing Industry StructuresunnysunsationNo ratings yet

- Competitive Strategy: Lecture 2: External EnvironmentDocument22 pagesCompetitive Strategy: Lecture 2: External EnvironmenthrleenNo ratings yet

- Hec Group of Institutions, Haridwar Online Notes Topic:-Michael Porter's Five Forces ModelDocument4 pagesHec Group of Institutions, Haridwar Online Notes Topic:-Michael Porter's Five Forces ModelHarshit KumarNo ratings yet

- OligopolyDocument16 pagesOligopolygipaworldNo ratings yet

- CG SkriptaDocument41 pagesCG SkriptaInesNo ratings yet

- Industry Handbook: Porte: R's 5 Forces AnalysisDocument20 pagesIndustry Handbook: Porte: R's 5 Forces AnalysisAnitha GirigoudruNo ratings yet

- Analysis of The Competitive EnvironmentDocument46 pagesAnalysis of The Competitive Environmentshivbab1No ratings yet

- Porters Five ForcesDocument12 pagesPorters Five ForcesPrithvi AcharyaNo ratings yet

- Industry and Environmental Analysis ActivityDocument3 pagesIndustry and Environmental Analysis Activityrosalinda yapNo ratings yet

- Analisis PorterDocument2 pagesAnalisis PorterAlim AhmadNo ratings yet

- Lecture 3 Industry AnalysisDocument37 pagesLecture 3 Industry AnalysisAsmaa BaaboudNo ratings yet

- Industry AnalysisDocument3 pagesIndustry AnalysisYuvraj MinawalaNo ratings yet

- Chapter 3 StrategicDocument9 pagesChapter 3 StrategicShewit DestaNo ratings yet

- The Competitive Power of the Product Lifecycle: Revolutionise the way you sell your productsFrom EverandThe Competitive Power of the Product Lifecycle: Revolutionise the way you sell your productsNo ratings yet

- BMA 12e SM CH 26 Final PDFDocument14 pagesBMA 12e SM CH 26 Final PDFNikhil ChadhaNo ratings yet

- TBCH 16Document19 pagesTBCH 16Bill Benntt100% (1)

- Forex MarketDocument33 pagesForex Marketaniket7gNo ratings yet

- Brunn 2002Document13 pagesBrunn 2002Aggna NiawanNo ratings yet

- CA Foundation BookDocument341 pagesCA Foundation Bookpmritunjay219No ratings yet

- Divergence (BraveFx Academy)Document12 pagesDivergence (BraveFx Academy)Mikail AdedejiNo ratings yet

- Dr. Ram Manohar Lohiya National Lawuniversity 2018-2019: Project OnDocument21 pagesDr. Ram Manohar Lohiya National Lawuniversity 2018-2019: Project OnHariank GuptaNo ratings yet

- Volume and Divergence by Gail MerceDocument7 pagesVolume and Divergence by Gail MerceCryptoFX80% (5)

- De Mar's Product Strategy Case Study: Group ThreeDocument11 pagesDe Mar's Product Strategy Case Study: Group ThreeDeepak UpadhyayNo ratings yet

- Marketing MyopiaDocument29 pagesMarketing MyopiaMuzammil MuzammilNo ratings yet

- Dividend Policy: Financial Management Theory and PracticeDocument33 pagesDividend Policy: Financial Management Theory and PracticeSamar KhanzadaNo ratings yet

- Strategy Formulation - Group 4Document41 pagesStrategy Formulation - Group 4Angeline de Sagun100% (1)

- ABM Applied Economics Module 5 Evaluating The Viability and Impacts of Business On The CommunityDocument90 pagesABM Applied Economics Module 5 Evaluating The Viability and Impacts of Business On The Communitymara ellyn lacson100% (1)

- (English) Why Do Competitors Open Their Stores Next To One Another? - Jac de Haan (DownSub - Com)Document4 pages(English) Why Do Competitors Open Their Stores Next To One Another? - Jac de Haan (DownSub - Com)FlorencedNo ratings yet

- Fundamental Inflexibility Assumptions:: W - Inflexible P - InflexibleDocument18 pagesFundamental Inflexibility Assumptions:: W - Inflexible P - InflexibleCedric PinNo ratings yet

- Marketing Management ReviewerDocument6 pagesMarketing Management ReviewerGrace MarasiganNo ratings yet

- Warwick Economics Summer School 2016 Problem Set 1 AnswersDocument9 pagesWarwick Economics Summer School 2016 Problem Set 1 AnswersAndrew NormandNo ratings yet

- Money Market Vs Capital MarketDocument53 pagesMoney Market Vs Capital MarketrajNo ratings yet

- The Expert'S Guide: To Building A GTM Strategy That WorksDocument22 pagesThe Expert'S Guide: To Building A GTM Strategy That WorksRony James100% (2)

- Physical DistributionDocument2 pagesPhysical DistributionKeshav ShankarNo ratings yet

- Parkin Econ SM CH06Document21 pagesParkin Econ SM CH06Quang VinhNo ratings yet

- Reading 6 The Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnDocument5 pagesReading 6 The Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnPriyadarshini SealNo ratings yet

- Exploring The Difference Between Micro and Macro EconomicsDocument5 pagesExploring The Difference Between Micro and Macro EconomicsExport ImbdNo ratings yet

- Employee ManagementDocument18 pagesEmployee ManagementTina BrutsNo ratings yet

- Supply, Demand and Government PoliciesDocument7 pagesSupply, Demand and Government PoliciesLý ĐinhNo ratings yet

- Addons Retail Private Limited Was Incorporated in 2006 (Autosaved)Document7 pagesAddons Retail Private Limited Was Incorporated in 2006 (Autosaved)Rajat RajoriyaNo ratings yet

- Noc18 mg35 Assignment5Document4 pagesNoc18 mg35 Assignment5ANADI BANCHHORNo ratings yet

- Introduction To Macroeconomics: IS-LM ModelDocument45 pagesIntroduction To Macroeconomics: IS-LM ModelAlbert Eka SaputraNo ratings yet

- Soneri Bank Limited Balance SheetDocument3 pagesSoneri Bank Limited Balance SheetSaad Ur RehmanNo ratings yet