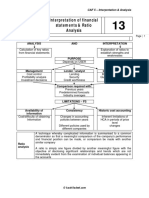

Ms9107a - Financial Statements Analysis

Ms9107a - Financial Statements Analysis

Download as docx, pdf, or txt

You might also like

- Financial Planning & Analysis and Performance ManagementFrom EverandFinancial Planning & Analysis and Performance ManagementRating: 3 out of 5 stars3/5 (1)

- Report On Ratio Analysis (Reliance Infrastructure Limited)Document21 pagesReport On Ratio Analysis (Reliance Infrastructure Limited)SiddhiNo ratings yet

- Solved On November 4 Kim Contracted To Sell To Lynn 500Document1 pageSolved On November 4 Kim Contracted To Sell To Lynn 500Anbu jaromiaNo ratings yet

- Material No. 2 Financial Statement Analysis: Laguna State Polytechnic University-Los Baños Laguna (LSPU-LBC)Document5 pagesMaterial No. 2 Financial Statement Analysis: Laguna State Polytechnic University-Los Baños Laguna (LSPU-LBC)Kristine Joy NolloraNo ratings yet

- 04 Financial Statements Analysis: Management Advisory Services Online ReviewDocument16 pages04 Financial Statements Analysis: Management Advisory Services Online Reviewkarim abitagoNo ratings yet

- Basic Accounting RatiosDocument47 pagesBasic Accounting RatiosSUNYYRNo ratings yet

- ch15 - Financial Statement AnalysisDocument51 pagesch15 - Financial Statement AnalysisMd.Shadid Ur RahmanNo ratings yet

- Ratio Analysis - Unit 2Document8 pagesRatio Analysis - Unit 2T S Kumar Kumar100% (1)

- SBA01 FSAnalysisPart1Document4 pagesSBA01 FSAnalysisPart1Hazel VillanuevaNo ratings yet

- FM. Financial Analysis BookDocument31 pagesFM. Financial Analysis Bookahmedsoobi73No ratings yet

- Ratio Analysis Q&a MAFDocument23 pagesRatio Analysis Q&a MAFmohedNo ratings yet

- Financial Statement AnalysisDocument13 pagesFinancial Statement AnalysisKim EllaNo ratings yet

- Chapter 9 Ratio AnalysisDocument65 pagesChapter 9 Ratio AnalysisClara rdpNo ratings yet

- Ratio AnalysisDocument33 pagesRatio AnalysisSamNo ratings yet

- The Financial Statement AnalysisDocument25 pagesThe Financial Statement Analysisgk37765No ratings yet

- UNIT 2 - Ratio AnalysisDocument16 pagesUNIT 2 - Ratio AnalysisVishika jainNo ratings yet

- Financial Statement AnalysisDocument56 pagesFinancial Statement AnalysisJade Berlyn AgcaoiliNo ratings yet

- Mahesh Total Project 1Document70 pagesMahesh Total Project 1Kaveti Madhu lathaNo ratings yet

- Financial Statement AnalysisDocument6 pagesFinancial Statement AnalysisCIPRIANO, Rodielyn L.No ratings yet

- Final Report Rachitha PDFDocument35 pagesFinal Report Rachitha PDFThanuja BhaskarNo ratings yet

- 4 Financial AnalysisDocument1 page4 Financial AnalysisHana DwiNo ratings yet

- Class 12 Accountancy Project (Specific) Ratio Analysis PidiliteDocument18 pagesClass 12 Accountancy Project (Specific) Ratio Analysis PidiliteAvirup Chakraborty55% (40)

- Class 12 Accountancy Project Specific Ratio Analysis PidiliteDocument18 pagesClass 12 Accountancy Project Specific Ratio Analysis Pidiliteyogesh kumarNo ratings yet

- Unit 5 MANAGEMENT ACCOUNTINGDocument25 pagesUnit 5 MANAGEMENT ACCOUNTINGSANDFORD MALULUNo ratings yet

- Ratio AnalysisDocument25 pagesRatio Analysismba departmentNo ratings yet

- Chapter 9 Ratio AnalysisDocument65 pagesChapter 9 Ratio AnalysisPoojaNo ratings yet

- Interpretation of Financial Statements & Ratio AnalysisDocument35 pagesInterpretation of Financial Statements & Ratio Analysisamitsinghslideshare67% (3)

- Introduction To Accounting: Financial Statements AnalysisDocument53 pagesIntroduction To Accounting: Financial Statements AnalysiskweeNo ratings yet

- Bafinmax Topic 2Document109 pagesBafinmax Topic 2airwaller rNo ratings yet

- Financial Statement Analysis LectureDocument71 pagesFinancial Statement Analysis Lecturephilippineball mapper100% (2)

- Vertical AnalysisDocument45 pagesVertical AnalysisArpit SidhuNo ratings yet

- AFMA Cha 4 MBA TT at 2020Document38 pagesAFMA Cha 4 MBA TT at 2020sheawNo ratings yet

- Financial Ratios: Research StartersDocument11 pagesFinancial Ratios: Research Starterszar.mx03No ratings yet

- 05 Ratios and Trend AnalysisDocument11 pages05 Ratios and Trend AnalysisHaris IshaqNo ratings yet

- Finalysis Reviewer Ver1Document2 pagesFinalysis Reviewer Ver1Eyvin AbleNo ratings yet

- FPA CHEATSHEET c6m74mDocument1 pageFPA CHEATSHEET c6m74mMaqbool ShahidNo ratings yet

- Report - Financial Statement AnalysisDocument43 pagesReport - Financial Statement AnalysisVijayNo ratings yet

- Class 12 Accountancy Projectspecific Ratio Analysis Pidilite PDF FreeDocument15 pagesClass 12 Accountancy Projectspecific Ratio Analysis Pidilite PDF Freeabu lilahNo ratings yet

- Financial RatiosDocument9 pagesFinancial RatiosDavid Isaias Jaimes ReyesNo ratings yet

- Pre Defense ReportDocument4 pagesPre Defense ReportKhayceePadillaNo ratings yet

- 1.1 Basic Financial Statement Analysis 2Document69 pages1.1 Basic Financial Statement Analysis 27rtqzp2fj8No ratings yet

- Financial RatiosDocument30 pagesFinancial RatiosSumitt AgrawalNo ratings yet

- Bcom Ratio Anlysis - Dr. S. M. VohraDocument18 pagesBcom Ratio Anlysis - Dr. S. M. Vohrankengbrandon7No ratings yet

- Module 01Document11 pagesModule 01VinDiesel Balag-eyNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument26 pagesFinancial Statement Analysis: K R Subramanyam John J WildichabooksNo ratings yet

- CF1 Lec3 Financial Analysis SVDocument31 pagesCF1 Lec3 Financial Analysis SVAnh Nguyễn MaiNo ratings yet

- Financial Statement Anlaysis Ratio Analysis - Session 17 To 19Document49 pagesFinancial Statement Anlaysis Ratio Analysis - Session 17 To 19shvm.shkla96No ratings yet

- Final Project Report On Financial Statement AnalysisDocument36 pagesFinal Project Report On Financial Statement AnalysisMercy Jacob100% (1)

- Chapter 9 Ratio Analysis1Document65 pagesChapter 9 Ratio Analysis1niovaleyNo ratings yet

- Ratio Analysis 08.04.2022Document15 pagesRatio Analysis 08.04.2022surangauorNo ratings yet

- Financial Performance Measures and Value Creation: the State of the ArtFrom EverandFinancial Performance Measures and Value Creation: the State of the ArtNo ratings yet

- Financial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesFrom EverandFinancial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesNo ratings yet

- Wiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)No ratings yet

- Financial Statement Analysis: Business Strategy & Competitive AdvantageFrom EverandFinancial Statement Analysis: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Financial Steering: Valuation, KPI Management and the Interaction with IFRSFrom EverandFinancial Steering: Valuation, KPI Management and the Interaction with IFRSNo ratings yet

- Implementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesFrom EverandImplementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesNo ratings yet

- Financial Management: Partner in Driving Performance and ValueFrom EverandFinancial Management: Partner in Driving Performance and ValueNo ratings yet

- 9114 - Process CostingDocument4 pages9114 - Process CostingCelestaire LeeNo ratings yet

- 9113 - Standard CostingDocument2 pages9113 - Standard CostingCelestaire LeeNo ratings yet

- 9112 - JIT and Backflush CostingDocument2 pages9112 - JIT and Backflush CostingCelestaire LeeNo ratings yet

- MS9111a - Self-Test AnswersDocument7 pagesMS9111a - Self-Test AnswersCelestaire LeeNo ratings yet

- ch09 1Document20 pagesch09 1Celestaire LeeNo ratings yet

- Chapter 5 Job Order CostingDocument19 pagesChapter 5 Job Order CostingCelestaire LeeNo ratings yet

- CPAR85 Auditing TheoryDocument10 pagesCPAR85 Auditing TheoryCelestaire LeeNo ratings yet

- Chapter 16 Managing Costs and UncertaintyDocument22 pagesChapter 16 Managing Costs and UncertaintyCelestaire LeeNo ratings yet

- Chapter 15 Capital BudgetingDocument16 pagesChapter 15 Capital BudgetingCelestaire LeeNo ratings yet

- Chapter 11 Allocation of Joint Costs and Accounting For by ProductDocument18 pagesChapter 11 Allocation of Joint Costs and Accounting For by ProductCelestaire LeeNo ratings yet

- Chapter 14 Performance Measurement, Balanced Scorecards and Performance RewardsDocument12 pagesChapter 14 Performance Measurement, Balanced Scorecards and Performance RewardsCelestaire LeeNo ratings yet

- GS Guide To Inflation-Linked BondsDocument8 pagesGS Guide To Inflation-Linked BondsOmer H.No ratings yet

- Excise, Taxation and Narcotics Control DepartmentDocument1 pageExcise, Taxation and Narcotics Control DepartmentabdulqadirjewlNo ratings yet

- Ee 4146 - Chapt. 4, 5, 6Document13 pagesEe 4146 - Chapt. 4, 5, 6Gian Carla C. NICOLASNo ratings yet

- Macroeconomics: Lection 2: Riccardo FranceschinDocument20 pagesMacroeconomics: Lection 2: Riccardo FranceschindurdyNo ratings yet

- Company Vinamilk PESTLE AnalyzeDocument2 pagesCompany Vinamilk PESTLE AnalyzeHiền ThảoNo ratings yet

- 1form No. IoccadDocument1 page1form No. Ioccadkinnari bhutaNo ratings yet

- Filing of Resolutions and Agreements To The Registrar Under Section 117Document14 pagesFiling of Resolutions and Agreements To The Registrar Under Section 117Prathap ChowdaryNo ratings yet

- PARAGMILK StockReport 20230828 1022Document12 pagesPARAGMILK StockReport 20230828 1022Chetan ChouguleNo ratings yet

- Projections 20.11.20Document7 pagesProjections 20.11.20Pawan GuptaNo ratings yet

- Copy4-Mr. Ramashankar Yadav Confirmation Letter Ind 1Document2 pagesCopy4-Mr. Ramashankar Yadav Confirmation Letter Ind 1farhanNo ratings yet

- Each Question Carries Mark: Objective TypeDocument10 pagesEach Question Carries Mark: Objective TypeSyed Fawad MarwatNo ratings yet

- Chak # 111/15-L, Post Office Mohsinwal, Tehsil Mian Channu, Khanewal, Mian Channu. Abbas AliDocument3 pagesChak # 111/15-L, Post Office Mohsinwal, Tehsil Mian Channu, Khanewal, Mian Channu. Abbas AliZeeshan Haider RizviNo ratings yet

- (Updated) List of IFRS and IAS 2021 - WikiaccountingDocument4 pages(Updated) List of IFRS and IAS 2021 - WikiaccountingAli KhanNo ratings yet

- CA Final DT Q MTP 2 Nov23 Castudynotes ComDocument10 pagesCA Final DT Q MTP 2 Nov23 Castudynotes ComRajdeep GuptaNo ratings yet

- Powell and Zwolinski The Ethical and Economic Case Against Sweatshop LaborDocument24 pagesPowell and Zwolinski The Ethical and Economic Case Against Sweatshop LaborEngr Gaddafi Kabiru MarafaNo ratings yet

- Thi Online 1 Phân TDocument3 pagesThi Online 1 Phân TnguyenanhthushinNo ratings yet

- CONTROLLING. Your TRADES, MONEY& EMOTIONS. by Chris VermeulenDocument11 pagesCONTROLLING. Your TRADES, MONEY& EMOTIONS. by Chris VermeulenfrankkinunghiNo ratings yet

- Ay - of - IKEA - in - The - Case - of - Internationalisation Title: Strategic Drivers & Barriers Essay of IKEA in The Case of InternationalisationDocument12 pagesAy - of - IKEA - in - The - Case - of - Internationalisation Title: Strategic Drivers & Barriers Essay of IKEA in The Case of InternationalisationgayaNo ratings yet

- Case Study On MilkyMistDocument10 pagesCase Study On MilkyMistHarshit MistryNo ratings yet

- Qnet Full Magazine NewDocument94 pagesQnet Full Magazine NewNishad MishraNo ratings yet

- CASE DIGEST Commissioner of Lnternal Revenue (CIR) vs. Algue, Inc. (158 SCRA 9), G.R. No. L-28896, February 17, 1988 - Batas FiDocument1 pageCASE DIGEST Commissioner of Lnternal Revenue (CIR) vs. Algue, Inc. (158 SCRA 9), G.R. No. L-28896, February 17, 1988 - Batas FisundaeicecreamNo ratings yet

- 3443 Daiwa 20221027 PDFDocument8 pages3443 Daiwa 20221027 PDFVinaNo ratings yet

- QB Income TaxesDocument6 pagesQB Income TaxesSarthak MalhotraNo ratings yet

- 2.3.4 Marketing PlanDocument9 pages2.3.4 Marketing PlanKumar DiwakarNo ratings yet

- Emilio P. Callelero Ii: Putatan, Muntinlupa CityDocument3 pagesEmilio P. Callelero Ii: Putatan, Muntinlupa CityYuan Joseph YuloNo ratings yet

- FMT 14Document8 pagesFMT 14Armel AbarracosoNo ratings yet

- Inventory SystemsDocument3 pagesInventory SystemsAllen Carl33% (3)

- Net Capital Outflow: Trade BalanceDocument3 pagesNet Capital Outflow: Trade Balancehnin scarletNo ratings yet

- Honda MotorsDocument68 pagesHonda MotorsCyber VirginNo ratings yet