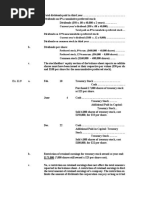

Screenshot 2024-05-20 at 9.51.03 PM

Screenshot 2024-05-20 at 9.51.03 PM

Download as pdf or txt

You might also like

- Problems Chapter 11Document29 pagesProblems Chapter 11Incia100% (1)

- SHE Answer KeyDocument29 pagesSHE Answer KeyTerence Jeff Tamondong100% (1)

- RevOps FrameworkDocument29 pagesRevOps FrameworkCSPL 247100% (2)

- Repay Mobile Wallet Pitch Deck Orientation NullDocument15 pagesRepay Mobile Wallet Pitch Deck Orientation NullNick MilanoNo ratings yet

- Advanced Portfolio Management: A Quant's Guide for Fundamental InvestorsFrom EverandAdvanced Portfolio Management: A Quant's Guide for Fundamental InvestorsNo ratings yet

- Chapter 2 - Shareholder's Equity MCDocument19 pagesChapter 2 - Shareholder's Equity MCJoshua AbanalesNo ratings yet

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Ex Ch.15Document2 pagesEx Ch.15kenny 322016048No ratings yet

- Sol. Man. - Chapter 10 She 1Document9 pagesSol. Man. - Chapter 10 She 1Miguel AmihanNo ratings yet

- AppliedEconomics - Q3 - Mod3 - Market Demand, Market Supply and Market EquilibriumDocument16 pagesAppliedEconomics - Q3 - Mod3 - Market Demand, Market Supply and Market EquilibriumRolando Corado Rama Gomez Jr.67% (9)

- ACT1106-Midterm Quiz No. 3 With AnswerDocument6 pagesACT1106-Midterm Quiz No. 3 With AnswerPj Dela VegaNo ratings yet

- Solution To Ch15 ProblemDocument19 pagesSolution To Ch15 Problemsabrina danteNo ratings yet

- InstructionsDocument7 pagesInstructionsGarp BarrocaNo ratings yet

- ACC 3003 - ReviewDocument22 pagesACC 3003 - Reviewfalnuaimi001No ratings yet

- Soal Chapter 15 Dividend - Kelompok 1Document11 pagesSoal Chapter 15 Dividend - Kelompok 1suci monalia putriNo ratings yet

- ACC 3003 - Final Exam Revision - SolutionDocument22 pagesACC 3003 - Final Exam Revision - Solutionfalnuaimi001No ratings yet

- QUIZ AccountingDocument5 pagesQUIZ AccountingEzy Tri TANo ratings yet

- 2010-10-21 031215 MookaDocument2 pages2010-10-21 031215 MookaVahrul DavidNo ratings yet

- Dividends E15-12 (Cash Dividend and Liquidating Dividend)Document3 pagesDividends E15-12 (Cash Dividend and Liquidating Dividend)Salma Hazem100% (1)

- Practice Drills - Accounting For CorporationDocument7 pagesPractice Drills - Accounting For Corporationhida.bajao.swuNo ratings yet

- Catapang Hazel Ann E.Document4 pagesCatapang Hazel Ann E.Johnlloyd BarretoNo ratings yet

- Sol. Man. - Chapter 11 She 2Document14 pagesSol. Man. - Chapter 11 She 2finn mertensNo ratings yet

- Assessment Tasks Jan 5 and 7 2022 InocencioDocument8 pagesAssessment Tasks Jan 5 and 7 2022 Inocencioalianna johnNo ratings yet

- Dividend Practice Problems (1) Anderson Inc. Has 600,000 Shares of Common Stock Outstanding, and Its EPS AreDocument4 pagesDividend Practice Problems (1) Anderson Inc. Has 600,000 Shares of Common Stock Outstanding, and Its EPS AreYoite MiharuNo ratings yet

- Solution Aassignments CH 11Document12 pagesSolution Aassignments CH 11RuturajPatilNo ratings yet

- Chapter 17 AnswersDocument5 pagesChapter 17 AnswersJennifer Cooper100% (1)

- Equity Investments Tutorial (3373)Document4 pagesEquity Investments Tutorial (3373)Rawan YasserNo ratings yet

- Sol. Man. - Chapter 10 She 1Document5 pagesSol. Man. - Chapter 10 She 1Nikky Bless LeonarNo ratings yet

- Homework 1 - BSC 402Document7 pagesHomework 1 - BSC 402Filip Cano100% (1)

- Acc108 Gen 008 p3 Questions and AnswersDocument26 pagesAcc108 Gen 008 p3 Questions and AnswersdgdeguzmanNo ratings yet

- Final Requirement ProblemsDocument5 pagesFinal Requirement ProblemsYoite MiharuNo ratings yet

- Special Appendix 1: Understanding The IssuesDocument6 pagesSpecial Appendix 1: Understanding The IssuesAnton VitaliNo ratings yet

- Chapter 10 Shareholders' 1Document8 pagesChapter 10 Shareholders' 1Thalia Rhine AberteNo ratings yet

- Solutions Chapter 16Document7 pagesSolutions Chapter 16Kakin WanNo ratings yet

- Chapter# 5 of Investments Principles & Concepts International Student Version 11th EditionDocument5 pagesChapter# 5 of Investments Principles & Concepts International Student Version 11th Editionmavimalik89% (9)

- Bab 3 - Kunci JawabanDocument6 pagesBab 3 - Kunci JawabanVanni LimNo ratings yet

- Mock Questions 2 Solutions - Various TopicsDocument9 pagesMock Questions 2 Solutions - Various TopicsiamneenugeorgeNo ratings yet

- Module 2 EquityDocument14 pagesModule 2 EquityFujoshi BeeNo ratings yet

- Sol. Man. - Chapter 14 - BVPS - 2021Document11 pagesSol. Man. - Chapter 14 - BVPS - 2021Crystal Rose TenerifeNo ratings yet

- Module 14 EquityDocument17 pagesModule 14 EquityZyril RamosNo ratings yet

- Amelia Putri Adinda 4b Lat 20Document6 pagesAmelia Putri Adinda 4b Lat 20Amel GpNo ratings yet

- Quiz Chapter-11 She-Part-2 2021Document5 pagesQuiz Chapter-11 She-Part-2 2021Salma B. AbdullahNo ratings yet

- Accounting SolutionsDocument11 pagesAccounting SolutionsKrittima Parn SuwanphorungNo ratings yet

- Kelompok 6 Latihan Soal EquityDocument7 pagesKelompok 6 Latihan Soal EquityTria SalzanabillaNo ratings yet

- Problem 16Document11 pagesProblem 16Anjan kunduNo ratings yet

- Corporation Issuance of Shares Illutsrative ProblemDocument15 pagesCorporation Issuance of Shares Illutsrative ProblemHoney MuliNo ratings yet

- Chapter 8Document10 pagesChapter 8Vip BigbangNo ratings yet

- Shareholders Equity Set CDocument14 pagesShareholders Equity Set CKaren GarciaNo ratings yet

- Shareholders' Equity Problems (Gallery Company)Document19 pagesShareholders' Equity Problems (Gallery Company)Nikki San GabrielNo ratings yet

- Review Questions For Test #2 ACC210Document8 pagesReview Questions For Test #2 ACC210AaaNo ratings yet

- Additional Solutions - Chapter 15Document24 pagesAdditional Solutions - Chapter 15maxima0078No ratings yet

- Earnings Per Share: Name: Date: Professor: Section: Score: QuizDocument5 pagesEarnings Per Share: Name: Date: Professor: Section: Score: QuizLovErsMaeBasergo0% (1)

- Exercises Module 9 For UploadDocument14 pagesExercises Module 9 For UploadjpNo ratings yet

- 07 Fischer10e SM Ch07 Final PDFDocument57 pages07 Fischer10e SM Ch07 Final PDFvivi anggi0% (1)

- ACCT336 Solved Exercises - Chapters 14 and 15Document5 pagesACCT336 Solved Exercises - Chapters 14 and 15kareemrawwadNo ratings yet

- Mill A N CH A Pter 1 Business Combin A Tion P A RT 3 CompressDocument5 pagesMill A N CH A Pter 1 Business Combin A Tion P A RT 3 CompressAubrey Shaiyne OfianaNo ratings yet

- Akm2 - Tugas4 - Kelompok 6Document13 pagesAkm2 - Tugas4 - Kelompok 6JNT EXPRESS TIMOHONo ratings yet

- Topic No. 5 Book Value Per ShareDocument36 pagesTopic No. 5 Book Value Per ShareYohanne MissNo ratings yet

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Paupau0% (1)

- CH 17 Select Problem SolutionsDocument11 pagesCH 17 Select Problem SolutionsJannit CarasscoNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- The Boston Institute of Finance Mutual Fund Advisor Course: Series 6 and Series 63 Test PrepFrom EverandThe Boston Institute of Finance Mutual Fund Advisor Course: Series 6 and Series 63 Test PrepNo ratings yet

- C O & G S R: Anadian IL AS Ector EportDocument10 pagesC O & G S R: Anadian IL AS Ector EportKullerglasez RoseNo ratings yet

- List PDFDocument2 pagesList PDFKristinaNo ratings yet

- Chap 1 Taking Risks and Making Profits Within The Dynamic Business EnvironmentDocument21 pagesChap 1 Taking Risks and Making Profits Within The Dynamic Business EnvironmentMinh DuyNo ratings yet

- Proposal Short Report Final DraftDocument3 pagesProposal Short Report Final Draftshort reportNo ratings yet

- BMO0272 Week 3 - Marketing week-StudentPreDocument58 pagesBMO0272 Week 3 - Marketing week-StudentPrekenechi lightNo ratings yet

- Lambda Exercises - Copy (11Document6 pagesLambda Exercises - Copy (11SamNo ratings yet

- Accounting: Cambridge International Examinations International General Certificate of Secondary EducationDocument16 pagesAccounting: Cambridge International Examinations International General Certificate of Secondary EducationOmar BilalNo ratings yet

- Grocery 4U CatalogueDocument34 pagesGrocery 4U Cataloguelexefem427No ratings yet

- 1 The Indian Contract Act 1872Document33 pages1 The Indian Contract Act 1872Varad Jakite100% (1)

- Demand, Supply and Equilibrium - QuizDocument3 pagesDemand, Supply and Equilibrium - Quizfranco jocsonNo ratings yet

- Theoretical Framework On Training and deDocument15 pagesTheoretical Framework On Training and deJason PowellNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument57 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancepra09031888No ratings yet

- Chapter 10 Project ManagementDocument49 pagesChapter 10 Project Managementtame kibruNo ratings yet

- International Business (Ine2028E) Final AssignmentDocument6 pagesInternational Business (Ine2028E) Final AssignmentHương GiangNo ratings yet

- The Complete Guide To Construction Management: Course ManualDocument49 pagesThe Complete Guide To Construction Management: Course ManualJosé Pedro Agonia100% (1)

- Compared To The Accounting For Business EntitiesDocument26 pagesCompared To The Accounting For Business EntitiesKristine PacalNo ratings yet

- Sustainability 16 02336 v2Document16 pagesSustainability 16 02336 v2k4b3x40No ratings yet

- Business CommunicationDocument2 pagesBusiness CommunicationSraban Ahmed MasumNo ratings yet

- Advertising Management Unit 2Document12 pagesAdvertising Management Unit 2goelsamarth17No ratings yet

- Influence Analysis of Customer Ratings Reviews Online, Free Shipping Promotion and Discount Promotion On Purchasing Decisions in E-CommerceDocument9 pagesInfluence Analysis of Customer Ratings Reviews Online, Free Shipping Promotion and Discount Promotion On Purchasing Decisions in E-CommercetamondongsharmNo ratings yet

- Sagesse University: Faculty of Business Administration and FinanceDocument7 pagesSagesse University: Faculty of Business Administration and FinanceZiad FarahNo ratings yet

- Training Needs Analysis TemplateDocument6 pagesTraining Needs Analysis TemplateNitesh LaguriNo ratings yet

- Eng (AutoRecovered)Document22 pagesEng (AutoRecovered)Thanh Trúc NguyễnNo ratings yet

- PDF Digital Marketing Strategy Guide Intermediate Level CompressDocument25 pagesPDF Digital Marketing Strategy Guide Intermediate Level CompressomaribnoussinaNo ratings yet

- 2019 Iso TDS PH88 en PDFDocument1 page2019 Iso TDS PH88 en PDFAabraham Samraj PonmaniNo ratings yet

- New Resume WFHDocument2 pagesNew Resume WFHsoukis rajNo ratings yet

- Q1. Prepare Ledger Account Using FIFO, LIFO, Weighted Average Method From The Following Transaction - Year 2006Document12 pagesQ1. Prepare Ledger Account Using FIFO, LIFO, Weighted Average Method From The Following Transaction - Year 2006MajidAli TvNo ratings yet