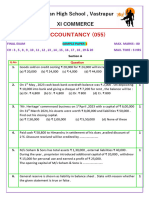

Trial Balance Sums

Trial Balance Sums

Download as pdf or txt

You might also like

- Reclaim Your Securities Posts-1Document459 pagesReclaim Your Securities Posts-1Bill Myers93% (43)

- 1a Millan Solution Manual 2021 1Document259 pages1a Millan Solution Manual 2021 1avilastephjane100% (3)

- Oracle R12 Financials (GL, AP, AR, CE, FA, MOAC and EB Tax) Training ManualDocument209 pagesOracle R12 Financials (GL, AP, AR, CE, FA, MOAC and EB Tax) Training ManualHaroon Dar67% (3)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- AP - 02 LOANS AND RECEIVALBES With Answer PDFDocument12 pagesAP - 02 LOANS AND RECEIVALBES With Answer PDFJymldy Encln67% (3)

- ODM Training MaterialDocument73 pagesODM Training MaterialMuhammad Zeeshan Younis100% (1)

- Finl Exm Et 1, 2024Document7 pagesFinl Exm Et 1, 2024Vishavpreet SinghNo ratings yet

- Class - 11 Accountancy Annual Exam Sample PaperDocument10 pagesClass - 11 Accountancy Annual Exam Sample Papergookhalo16No ratings yet

- Lea Cubia Topical TestDocument6 pagesLea Cubia Topical TestTesa RudangtaNo ratings yet

- 11 Accountancy SP 01Document33 pages11 Accountancy SP 01Abhay ChoudharyNo ratings yet

- Sample Paper 5 (Final Exam XI Accountancy)Document9 pagesSample Paper 5 (Final Exam XI Accountancy)pritanshutripathi84No ratings yet

- Class 12 Mjkps Question PaperDocument5 pagesClass 12 Mjkps Question PaperJeevitesh SinghalNo ratings yet

- Quiz 2 3 Sample 1 SolvedDocument6 pagesQuiz 2 3 Sample 1 SolvedJan Mohammad BalochNo ratings yet

- 11 Accountancy SP 01Document33 pages11 Accountancy SP 01Haridas OngallurNo ratings yet

- Time: 3 Hours Total Marks: 100: Printed Pages: 03 Sub Code: KMB103 Paper Id: 270103 Roll NoDocument4 pagesTime: 3 Hours Total Marks: 100: Printed Pages: 03 Sub Code: KMB103 Paper Id: 270103 Roll NoAbhishek ChaubeyNo ratings yet

- Cbse Class 11 Accountancy Sample Paper Set 1 QuestionsDocument6 pagesCbse Class 11 Accountancy Sample Paper Set 1 QuestionsNishtha 3153No ratings yet

- 11th AccountDocument3 pages11th Accountnmzrv8jfq8No ratings yet

- Ac Test 80 M (1) - Watermark - WatermarkDocument5 pagesAc Test 80 M (1) - Watermark - Watermarkanikeshyadav0700No ratings yet

- 11th Annual Benedict's PDFDocument15 pages11th Annual Benedict's PDFYugam RathiNo ratings yet

- Sample Paper AccountsDocument7 pagesSample Paper AccountsmenekyakiaNo ratings yet

- 11th Cbse - Edited FinalDocument19 pages11th Cbse - Edited FinalamarsinghdeoNo ratings yet

- A3-T1-T5 Grande Finale Solving Nov 2024 (Set 2)Document6 pagesA3-T1-T5 Grande Finale Solving Nov 2024 (Set 2)marymeela24No ratings yet

- 11 Accountancy First Term Set BDocument6 pages11 Accountancy First Term Set Bmcsworkshop777No ratings yet

- Namma Kalvi 11th Accountancy Model Questin Paper EM 221452Document8 pagesNamma Kalvi 11th Accountancy Model Questin Paper EM 221452sharonjamesappuNo ratings yet

- Acc Paper Class 11Document16 pagesAcc Paper Class 11Varsha AswaniNo ratings yet

- 1styr 1stMT Financial Accounting and Reporting 2324Document31 pages1styr 1stMT Financial Accounting and Reporting 2324MaryNo ratings yet

- Accounts U1 Spec2022Document41 pagesAccounts U1 Spec2022AbbyNo ratings yet

- Finals 2019Document4 pagesFinals 2019GargiNo ratings yet

- 11 Accountancy First Term Set ADocument6 pages11 Accountancy First Term Set Amcsworkshop777No ratings yet

- Bookkeping & AccountingDocument12 pagesBookkeping & Accountingzwelihlezwane38No ratings yet

- B.ComDocument32 pagesB.ComThirsha VNo ratings yet

- Management AccountingDocument3 pagesManagement AccountingDr.C.Boopathi HoD-B.Com PANo ratings yet

- Commercial Studies (Sem-2) 2022 Set - 2Document7 pagesCommercial Studies (Sem-2) 2022 Set - 2shrikantNo ratings yet

- The Accounting Process: Name: Date: Professor: Section: Score: QuizDocument6 pagesThe Accounting Process: Name: Date: Professor: Section: Score: QuizAllyna Jane Enriquez100% (1)

- Answer To MTP - Intermediate - Syllabus 2016 - June2020 - Set1: Paper 5-Financial AccountingDocument17 pagesAnswer To MTP - Intermediate - Syllabus 2016 - June2020 - Set1: Paper 5-Financial AccountingMohit SangwanNo ratings yet

- ACC XI SEE QP For RevisionDocument31 pagesACC XI SEE QP For Revisionvarshitha reddyNo ratings yet

- CA Foundation - Accounting - Suggested AnswerDocument17 pagesCA Foundation - Accounting - Suggested AnswerSunidhi AhireNo ratings yet

- Iatfe V4ggoDocument15 pagesIatfe V4ggogookhalo16No ratings yet

- MCQs On Cash Book & Ledgers PDFDocument11 pagesMCQs On Cash Book & Ledgers PDFHaroon Akhtar100% (1)

- Accountancy - Additional Questions MARKING SCHEMEDocument15 pagesAccountancy - Additional Questions MARKING SCHEMEseema chadhaNo ratings yet

- Xi See Acc 2021 Set 2 MsDocument5 pagesXi See Acc 2021 Set 2 Mss1672snehil6353No ratings yet

- 11 Accountancy Practice PaperDocument9 pages11 Accountancy Practice PaperPlayer dude65No ratings yet

- Marking Scheme of Accountancy PaperDocument12 pagesMarking Scheme of Accountancy PaperjyarjunNo ratings yet

- 12 Accountancy sp10Document26 pages12 Accountancy sp10Akshat AgarwalNo ratings yet

- DBM 611 Financial AccountingDocument3 pagesDBM 611 Financial AccountingCollins AbereNo ratings yet

- Chapter 9Document7 pagesChapter 9Saharin Islam ShakibNo ratings yet

- Poa Multiple Choice Questions 6-10Document11 pagesPoa Multiple Choice Questions 6-10AsishMohapatra100% (1)

- CBSE Class 10 Elements of Book Keeping and Accountancy Sample Question Paper 2017-2018Document5 pagesCBSE Class 10 Elements of Book Keeping and Accountancy Sample Question Paper 2017-2018Sowmy BNo ratings yet

- Sss 3 Exam QuetionsDocument10 pagesSss 3 Exam QuetionsEmmanuel UbaNo ratings yet

- MGMT 600 SAMPLE Midterm Exam 1Document9 pagesMGMT 600 SAMPLE Midterm Exam 1Enkhbadral UlaanhuuNo ratings yet

- Financial Accounting RealDocument7 pagesFinancial Accounting RealMihir ChawlaNo ratings yet

- 02 - Book Keeping-QuestionDocument9 pages02 - Book Keeping-Questionvivian1642006No ratings yet

- 943 Question PaperDocument3 pages943 Question PaperPacific TigerNo ratings yet

- Sample QP For Grade 11 ACC Model Examination 2024Document9 pagesSample QP For Grade 11 ACC Model Examination 2024Suhaim SahebNo ratings yet

- Cbleacpu 08Document10 pagesCbleacpu 08Agastya KarnwalNo ratings yet

- Iii SemesterDocument13 pagesIii Semesternashedidrax14581No ratings yet

- DISSLUTIONDocument3 pagesDISSLUTIONomgarg2714No ratings yet

- Sol. Man. - Chapter 1 - The Accounting Process - Ia Part 1a - 2020 EditionDocument12 pagesSol. Man. - Chapter 1 - The Accounting Process - Ia Part 1a - 2020 EditionCharlene Mae Malaluan100% (1)

- Time: 3 Hours Total Marks: 100: Printed Pages: 03 Subcode:Nmba013 Paper Id: 270138 Roll NoDocument3 pagesTime: 3 Hours Total Marks: 100: Printed Pages: 03 Subcode:Nmba013 Paper Id: 270138 Roll NoMohit RanaNo ratings yet

- Final Question Paper Accountancy (2023-24)Document6 pagesFinal Question Paper Accountancy (2023-24)mamta.bdvrrmaNo ratings yet

- 14 Corporate Accounting - April May 2021 (Repeaters 2013-14 and Onwards)Document8 pages14 Corporate Accounting - April May 2021 (Repeaters 2013-14 and Onwards)premium info2222No ratings yet

- Chapter 6-Trial Balance and Rectification of Errors Previous QuestionsDocument12 pagesChapter 6-Trial Balance and Rectification of Errors Previous Questionscrescenthss vanimalNo ratings yet

- Revision Accountancy XI Term II 8.12.2022 FinalDocument15 pagesRevision Accountancy XI Term II 8.12.2022 FinalNIRMALA COMMERCE DEPTNo ratings yet

- ICWIM - EIF - Notes 11Document98 pagesICWIM - EIF - Notes 11Sailesh GoenkkaNo ratings yet

- National Income Circular Flow MCQ SolutionDocument5 pagesNational Income Circular Flow MCQ SolutionSailesh GoenkkaNo ratings yet

- MichelleDocument50 pagesMichelleSailesh GoenkkaNo ratings yet

- Vijay Eco Copy 12Document50 pagesVijay Eco Copy 12Sailesh GoenkkaNo ratings yet

- June 2020 QP - Paper 2 Edexcel (A) Economics As-LevelDocument32 pagesJune 2020 QP - Paper 2 Edexcel (A) Economics As-LevelSailesh GoenkkaNo ratings yet

- National Income Computation QuestionDocument28 pagesNational Income Computation QuestionSailesh GoenkkaNo ratings yet

- Cash Book QuestionDocument24 pagesCash Book QuestionSailesh GoenkkaNo ratings yet

- Issue of DebenturesDocument3 pagesIssue of DebenturesSailesh GoenkkaNo ratings yet

- Business ManagementDocument50 pagesBusiness ManagementSailesh GoenkkaNo ratings yet

- Journal QuestionsDocument22 pagesJournal QuestionsSailesh GoenkkaNo ratings yet

- The Mother Dairy Employees Cghs LTD.: All Members / OwnersDocument3 pagesThe Mother Dairy Employees Cghs LTD.: All Members / OwnersAnilNo ratings yet

- 2-Ch. (Partnership Firm-Basic Concepts (Ver.-5)Document51 pages2-Ch. (Partnership Firm-Basic Concepts (Ver.-5)VP SengarNo ratings yet

- Cambridge Ordinary Level: Cambridge Assessment International EducationDocument20 pagesCambridge Ordinary Level: Cambridge Assessment International EducationShingirayi MazingaizoNo ratings yet

- FABM2121 Fundamentals of Accountancy Q2 Written Work 1Document4 pagesFABM2121 Fundamentals of Accountancy Q2 Written Work 1Christian Tero100% (2)

- Fundamentals of Accountancy, Business and Management 1 (First Quarter)Document80 pagesFundamentals of Accountancy, Business and Management 1 (First Quarter)Bernard Baruiz100% (1)

- Soneri Bank Internship ReportDocument24 pagesSoneri Bank Internship ReportOvaIs MoInNo ratings yet

- Basic Documentation and Books of Account: Topic 3Document32 pagesBasic Documentation and Books of Account: Topic 3vickramravi16No ratings yet

- LK Buku Besar PT Home BycicleDocument7 pagesLK Buku Besar PT Home BycicleFredi Dwi SusantoNo ratings yet

- P5 8Document4 pagesP5 8laurentinus fikaNo ratings yet

- Aec 203 Activitieswk5Document12 pagesAec 203 Activitieswk5Lorenz Joy Ogatis BertoNo ratings yet

- Business Account I 05 Gree I A LaDocument440 pagesBusiness Account I 05 Gree I A Lablu_qwertyNo ratings yet

- 3.1 Lecturer1.Chapter3.Balancing Off and Trail BalanceDocument34 pages3.1 Lecturer1.Chapter3.Balancing Off and Trail Balancekurosakirin004No ratings yet

- 5 6215195415390715991Document16 pages5 6215195415390715991RITIK AGARWALNo ratings yet

- Mid Term Exam Oct 2016 With SolDocument11 pagesMid Term Exam Oct 2016 With Solsunflower33% (3)

- BCSV5.2 - Organization and FormationDocument9 pagesBCSV5.2 - Organization and Formationjam linganNo ratings yet

- CHAPTER 3 The Accounting Cycle (I)Document33 pagesCHAPTER 3 The Accounting Cycle (I)Addisalem Mesfin0% (2)

- Đề Thi Thử KPMG Intern 2022Document123 pagesĐề Thi Thử KPMG Intern 2022Minh Nhật Bùi100% (1)

- Applying For A VISA 2015 PDFDocument5 pagesApplying For A VISA 2015 PDFShihab HasanNo ratings yet

- Quiz Financial Accounting NTTDocument34 pagesQuiz Financial Accounting NTTdatdo1105No ratings yet

- Audit of The Sales and Collection Cycle: Tests of Controls and Substantive Tests of TransactionsDocument38 pagesAudit of The Sales and Collection Cycle: Tests of Controls and Substantive Tests of TransactionsLouis ValentinoNo ratings yet

- INDUSDocument2 pagesINDUSHoaccounts AuNo ratings yet

- Document 28 PDF - RemovedDocument1 pageDocument 28 PDF - RemovedalysNo ratings yet

- Cost CenterDocument47 pagesCost Centerkunaruba89% (9)

- Hernandez Cieza ING 1 PAFDocument59 pagesHernandez Cieza ING 1 PAFJosè MHNo ratings yet

- SAP Certified Application Associate - Financial Accounting With SAP ERP - FullDocument41 pagesSAP Certified Application Associate - Financial Accounting With SAP ERP - FullMohammed Nawaz ShariffNo ratings yet

- Form - 1040 - ES PDFDocument12 pagesForm - 1040 - ES PDFAnonymous JqimV1ENo ratings yet

- Hotel Cash ManagementDocument56 pagesHotel Cash ManagementMandeep Singh100% (1)