GWLC Corp Bf.

GWLC Corp Bf.

Download as pdf or txt

You might also like

- Accounting-Formats For Cambridge IGCSEDocument11 pagesAccounting-Formats For Cambridge IGCSEmuhtasim kabir100% (10)

- Quiz 1Document5 pagesQuiz 1yousufNo ratings yet

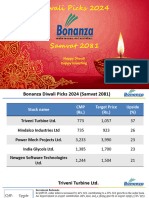

- Diwali Picks '24Document9 pagesDiwali Picks '241kavitacNo ratings yet

- BSCC - NTPC LTDDocument41 pagesBSCC - NTPC LTDDhruv ManshaniNo ratings yet

- Corporate Briefing Notes - POWERDocument5 pagesCorporate Briefing Notes - POWERAbdullah CheemaNo ratings yet

- Corporate Briefing Notes - ATRLDocument5 pagesCorporate Briefing Notes - ATRLxanen40512No ratings yet

- Adani Power Announces Q3 FY22 Results: Media ReleaseDocument4 pagesAdani Power Announces Q3 FY22 Results: Media Releasekashyappathak01No ratings yet

- Power UtilitiesDocument57 pagesPower UtilitiesVedant NarulaNo ratings yet

- Q1 Accounts 31.03.2024 2Document57 pagesQ1 Accounts 31.03.2024 2studyus11No ratings yet

- de 432 Caa 9 Aa 4 Fec 0Document1 pagede 432 Caa 9 Aa 4 Fec 0Ayaz ZafarNo ratings yet

- Check For Answers. Hope You Will Find ItDocument11 pagesCheck For Answers. Hope You Will Find ItMohammad Nazmul IslamNo ratings yet

- Binging Big On BTG : BUY Key Take AwayDocument17 pagesBinging Big On BTG : BUY Key Take AwaymittleNo ratings yet

- Corporate Briefing Notes - APLDocument5 pagesCorporate Briefing Notes - APLxanen40512No ratings yet

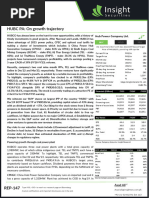

- Insight: HUBC PA: On Growth Trajectory Pakistan PowerDocument5 pagesInsight: HUBC PA: On Growth Trajectory Pakistan PowerShoaib A. KaziNo ratings yet

- Crompton Greaves LTD.: Investment RationaleDocument0 pagesCrompton Greaves LTD.: Investment Rationalespatel1972No ratings yet

- Initiating Coverage Cherat Cement Company LTD 2Document10 pagesInitiating Coverage Cherat Cement Company LTD 2faiqsattar1637No ratings yet

- Samaj Portfolio InvestmentDocument17 pagesSamaj Portfolio InvestmentsamanmaqsoodNo ratings yet

- Discussion Paper 01Document43 pagesDiscussion Paper 01Sari YaahNo ratings yet

- SH-2023-Q4-1-ICRA-Power Sector (1)Document10 pagesSH-2023-Q4-1-ICRA-Power Sector (1)pnadiyadra45No ratings yet

- JKLakshmi Cem Geojit 070218Document5 pagesJKLakshmi Cem Geojit 070218suprabhattNo ratings yet

- BGRDocument84 pagesBGRMustafa LokhandwalaNo ratings yet

- National Thermal Power Corporation LimitedDocument1 pageNational Thermal Power Corporation LimitedAshish kumar ThapaNo ratings yet

- Cement Utilization Level ImprovingDocument5 pagesCement Utilization Level Improvingfaizaaftab14No ratings yet

- Essar Oil and Gas Exploration and Production LimitedDocument7 pagesEssar Oil and Gas Exploration and Production LimitedParag HemdevNo ratings yet

- Jaiprakash Power Ventures LTDDocument8 pagesJaiprakash Power Ventures LTDMilind DhandeNo ratings yet

- Issues & Challenges in Power & Energy Sector of BangladeshDocument29 pagesIssues & Challenges in Power & Energy Sector of BangladeshRazu AhmedNo ratings yet

- Motilal Oswal Sees 18% UPSDIE in Coal India Robust Volume GrowthDocument18 pagesMotilal Oswal Sees 18% UPSDIE in Coal India Robust Volume GrowthDhaval MailNo ratings yet

- Power Sector: Ipps: Hedged To Near PerfectionDocument15 pagesPower Sector: Ipps: Hedged To Near Perfectionali_iqbalNo ratings yet

- Promoter's Background: Equity Shares Locked-In For One YearDocument8 pagesPromoter's Background: Equity Shares Locked-In For One YearabeeraksNo ratings yet

- Strategizing For Transformation To Clean Energy in The Changing Global Energy Landscap1Document7 pagesStrategizing For Transformation To Clean Energy in The Changing Global Energy Landscap1Oyedele PhilemonNo ratings yet

- Indian Express 14 September 2012 4Document1 pageIndian Express 14 September 2012 4Shahabaj DangeNo ratings yet

- Nalco Q4FY23 Result Update - 25052023 - 25-05-2023 - 12Document8 pagesNalco Q4FY23 Result Update - 25052023 - 25-05-2023 - 12Ashutosh AgarwalNo ratings yet

- Coal India LimitedDocument7 pagesCoal India Limitedabhinaskumarr150No ratings yet

- Way2Wealth May'22Document4 pagesWay2Wealth May'22RajatNo ratings yet

- Energy Security and AffordabilityDocument12 pagesEnergy Security and AffordabilityhonestscarryNo ratings yet

- Nabha Power Limited-10082012Document4 pagesNabha Power Limited-10082012Milind DhandeNo ratings yet

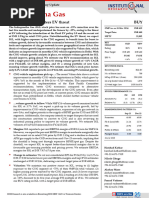

- 2.discourse-2023-05-04-challenges-and-reforms-in-pakistans-gas-sectorDocument3 pages2.discourse-2023-05-04-challenges-and-reforms-in-pakistans-gas-sectoryingte.tan.3uNo ratings yet

- BKT - Investor Presentation - February 2021 PDFDocument33 pagesBKT - Investor Presentation - February 2021 PDFYAP designerNo ratings yet

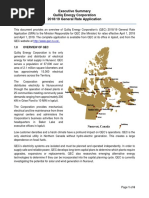

- 2018-2019 QEC General Rate Application, Executive SummaryDocument6 pages2018-2019 QEC General Rate Application, Executive SummaryNunatsiaqNewsNo ratings yet

- For Security and Affordability, We Must Shore Up Renewable Energy - The Daily StarDocument5 pagesFor Security and Affordability, We Must Shore Up Renewable Energy - The Daily StarMohammad Mukul HossainNo ratings yet

- 2020 Energy (Supply and Demand) Outlook For GhanaDocument93 pages2020 Energy (Supply and Demand) Outlook For GhanaRasheed BaisieNo ratings yet

- Coal India - IPO: Invest at Cut-OffDocument9 pagesCoal India - IPO: Invest at Cut-OffJoyraj DeyNo ratings yet

- NTPC LTD - Initiating Coverage - 04012024 - 04-01-2024 - 15Document19 pagesNTPC LTD - Initiating Coverage - 04012024 - 04-01-2024 - 15shivaNo ratings yet

- 17131483780.54904300Document9 pages17131483780.54904300Mr. GavNo ratings yet

- Industrial Goods Sector - Mid-Year Outlook 2023Document17 pagesIndustrial Goods Sector - Mid-Year Outlook 2023Carl MacaulayNo ratings yet

- Sustainability - Report ONGC PDFDocument116 pagesSustainability - Report ONGC PDFsurbhi guptaNo ratings yet

- AR 2013 14 Infra-ReviewDocument12 pagesAR 2013 14 Infra-ReviewHarshal PhuseNo ratings yet

- Performance Highlights: AccumulateDocument11 pagesPerformance Highlights: AccumulateAngel BrokingNo ratings yet

- NTPC Ltd - Stock Note -20.03.2023-signedDocument13 pagesNTPC Ltd - Stock Note -20.03.2023-signedSarvesh KanaujiaNo ratings yet

- Power Sector News 26.11Document5 pagesPower Sector News 26.11anjali_atriNo ratings yet

- Diwali Dhanotsav Portfolio 2023Document22 pagesDiwali Dhanotsav Portfolio 2023pramodkgowda3No ratings yet

- NTPC LimitedDocument7 pagesNTPC Limitedsaddiquekhan1014No ratings yet

- NTPC Result UpdatedDocument11 pagesNTPC Result UpdatedAngel BrokingNo ratings yet

- QuestionDocument22 pagesQuestionNikhil SainNo ratings yet

- West Bengal Commercial 2010 Chapter IIDocument79 pagesWest Bengal Commercial 2010 Chapter IISarthak ChatterjeeNo ratings yet

- Corporate Briefing Notes - EPCL-1Document4 pagesCorporate Briefing Notes - EPCL-1Abdullah CheemaNo ratings yet

- Q3 2023 Results PPT 1030Document16 pagesQ3 2023 Results PPT 1030lucius maharalNo ratings yet

- Ki Antm 20241108Document8 pagesKi Antm 20241108jenniferNo ratings yet

- 3_Mitigation and Adaptation_Pakistan's Nationally Determined Contributions-1Document26 pages3_Mitigation and Adaptation_Pakistan's Nationally Determined Contributions-1faizazahir3.57No ratings yet

- Circular DebtDocument6 pagesCircular DebtAli HaiderNo ratings yet

- CAREC Energy Strategy 2030: Common Borders. Common Solutions. Common Energy Future.From EverandCAREC Energy Strategy 2030: Common Borders. Common Solutions. Common Energy Future.No ratings yet

- Kaizen Done The IE Way Using Operations AnalysisDocument11 pagesKaizen Done The IE Way Using Operations AnalysisallahnawazksadozaiNo ratings yet

- Menstrual CupDocument9 pagesMenstrual Cupshreyash436No ratings yet

- CV DelviDocument5 pagesCV DelviMAULANA YUSUF HANAFINo ratings yet

- Financial Statement Analysis of Haldirams Pvt. Ltd.Document53 pagesFinancial Statement Analysis of Haldirams Pvt. Ltd.KRITISH BISWAS100% (1)

- Practice Exam 2013 Questions and AnswersDocument7 pagesPractice Exam 2013 Questions and AnswerstobyforsomereasonNo ratings yet

- Beginners-Guide To Real Estate InvestingDocument6 pagesBeginners-Guide To Real Estate InvestingDarriall PortilloNo ratings yet

- Lecture4 Interest N CashflowDocument24 pagesLecture4 Interest N Cashflowsuraj bhandariNo ratings yet

- COVID-19 Could Bring Down The Trading System: How To Stop Protectionism From Running AmokDocument6 pagesCOVID-19 Could Bring Down The Trading System: How To Stop Protectionism From Running AmokFer VdcNo ratings yet

- NCCC TemplateDocument5 pagesNCCC TemplateJack NobleNo ratings yet

- Computation 2022Document16 pagesComputation 2022Jagbandhu MaharanaNo ratings yet

- TIPS ON VALUE STATEMENTS IN CREDIT AUDITABLE ACCOUNTS UPTO Rs 50 CRDocument26 pagesTIPS ON VALUE STATEMENTS IN CREDIT AUDITABLE ACCOUNTS UPTO Rs 50 CRHaRa TNo ratings yet

- 2008410-Maruti Financial ModelDocument52 pages2008410-Maruti Financial ModelhellonandiniyadavNo ratings yet

- ECN 210 Review Questions For Chapter 12.Document5 pagesECN 210 Review Questions For Chapter 12.London CityNo ratings yet

- Assignment 2 FIN460Document28 pagesAssignment 2 FIN460tazrian nekeNo ratings yet

- Top 10 Picks For 2023Document13 pagesTop 10 Picks For 2023MittapalliUdayKumarReddyNo ratings yet

- Consumer As Co-ProducerDocument17 pagesConsumer As Co-ProducerNiraj ChaudhariNo ratings yet

- Walkers Case StudyDocument8 pagesWalkers Case StudyagilujallohNo ratings yet

- Chapter 3: Competing in Global Markets: Learning GoalsDocument6 pagesChapter 3: Competing in Global Markets: Learning GoalsshaimaaelgamalNo ratings yet

- EDP, Vivek Bansal, 154-18, Sec-CDocument15 pagesEDP, Vivek Bansal, 154-18, Sec-CVivek BansalNo ratings yet

- Analysis of Bkash Limited & Mobile Financial Services Industry in BangladeshDocument11 pagesAnalysis of Bkash Limited & Mobile Financial Services Industry in BangladeshRabeya AktarNo ratings yet

- Policy Certificate 73225618Document6 pagesPolicy Certificate 73225618concoctstoryNo ratings yet

- Adecco Taiwan Salary Guide 2023Document68 pagesAdecco Taiwan Salary Guide 2023Jackie Tung 董建祺No ratings yet

- IB Assignment (Suhani Narang)Document28 pagesIB Assignment (Suhani Narang)sanjognarang2007No ratings yet

- Hable Asrat PDFDocument75 pagesHable Asrat PDFNugusa Zeleke100% (1)

- Final SFM 1.5 Days StrategyDocument3 pagesFinal SFM 1.5 Days Strategyanandsundaramurthy10No ratings yet

- TYBAF SEM 6 Financial ManagementDocument10 pagesTYBAF SEM 6 Financial ManagementAditya DeodharNo ratings yet

- Fluorescent Tracking GelDocument2 pagesFluorescent Tracking GelBelfor JeldresNo ratings yet

- Kabarak University Placement List 2023 2024Document39 pagesKabarak University Placement List 2023 2024mwendaflaviushilelmutembeiNo ratings yet

- Production PlanningDocument4 pagesProduction PlanningTanishka R - VII CNo ratings yet