Logistics Tech - Avendus

Logistics Tech - Avendus

Download as pdf or txt

You might also like

- HACCP ChecklistDocument3 pagesHACCP ChecklistTim Qu100% (4)

- BDO Unibank 2020 Annual Report Financial SupplementsDocument236 pagesBDO Unibank 2020 Annual Report Financial SupplementsDanNo ratings yet

- Light Industry PresentationDocument4 pagesLight Industry PresentationAlex LionNo ratings yet

- BDO Unibank 2021 Annual Report Financial SupplementsDocument236 pagesBDO Unibank 2021 Annual Report Financial Supplementssharielles /No ratings yet

- Top Airport Projects Landscape 2024Document11 pagesTop Airport Projects Landscape 2024mmuzzammilNo ratings yet

- Annual Report 2075 76 EnglishDocument200 pagesAnnual Report 2075 76 Englishram krishnaNo ratings yet

- Cuba - Year 49 PDFDocument57 pagesCuba - Year 49 PDFUyen HoangNo ratings yet

- Industry Statistics Auto Components 09Document7 pagesIndustry Statistics Auto Components 09ManishNo ratings yet

- PDFDocument8 pagesPDFtbnc5nbdqwNo ratings yet

- Profit and Loss Template Under 77k Turnover 1Document2 pagesProfit and Loss Template Under 77k Turnover 1Edem Kofi BoniNo ratings yet

- Down-Payment Payable Trade-In Offered PriceDocument2 pagesDown-Payment Payable Trade-In Offered PriceAna ZaraNo ratings yet

- BDO Unibank 2021 Annual Report Financial Highlights PDFDocument2 pagesBDO Unibank 2021 Annual Report Financial Highlights PDFJohn Michael Dela CruzNo ratings yet

- Cargills Ceylon Sustainability 2020-21 FinalDocument52 pagesCargills Ceylon Sustainability 2020-21 FinalPasindu HarshanaNo ratings yet

- Sour Crude Diet: Venezuela Production Decline Shifts Lighter Crude Slates For Heavy RefinersDocument21 pagesSour Crude Diet: Venezuela Production Decline Shifts Lighter Crude Slates For Heavy RefinersLindsey BondNo ratings yet

- MDKA SucorDocument6 pagesMDKA SucorFathan MujibNo ratings yet

- Vietn Nam Retail Stores Report 2022Document37 pagesVietn Nam Retail Stores Report 2022Tu NguyenNo ratings yet

- 5-Year Group Financial Highlights: Financial Years Ended 31 December (RM Million) 2018 2019 2020 2021 2022 (Restated)Document1 page5-Year Group Financial Highlights: Financial Years Ended 31 December (RM Million) 2018 2019 2020 2021 2022 (Restated)superspt21No ratings yet

- Honda Financial HighDocument1 pageHonda Financial HighKrisha ChhorwaniNo ratings yet

- Fiche Evolution ECOBANK CIDocument1 pageFiche Evolution ECOBANK CITristan KevinNo ratings yet

- Media-Kit-Steel 360 Media Kit 2018Document7 pagesMedia-Kit-Steel 360 Media Kit 2018Sharon SusmithaNo ratings yet

- Terjadi Pada Titik Singgung Antara Kurva Isocost Dan Isoquan TDocument9 pagesTerjadi Pada Titik Singgung Antara Kurva Isocost Dan Isoquan TYudhi SutanaNo ratings yet

- Financial Forecast-Monthly 5 YearsDocument38 pagesFinancial Forecast-Monthly 5 Yearsms.rashid33No ratings yet

- EMI Calculator - Prepayment OptionDocument20 pagesEMI Calculator - Prepayment OptionRahul JoshiNo ratings yet

- Harrisons 2022 Annual Report Final CompressedDocument152 pagesHarrisons 2022 Annual Report Final Compressedarusmajuenterprise80No ratings yet

- BDO Unibank 2019-Annual-Report-Financial-Supplements PDFDocument228 pagesBDO Unibank 2019-Annual-Report-Financial-Supplements PDFCristine AquinoNo ratings yet

- Cash Flow Projection of MCV: SQM SQM RP.M/SQM RP.M/SQM SQM SQM RP.M US$. Tho Rp. MDocument26 pagesCash Flow Projection of MCV: SQM SQM RP.M/SQM RP.M/SQM SQM SQM RP.M US$. Tho Rp. Mangg4interNo ratings yet

- Weekly Statistics: The Indonesia Stock Exchange Composite Stock Price Index and Equity Trading ValueDocument2 pagesWeekly Statistics: The Indonesia Stock Exchange Composite Stock Price Index and Equity Trading ValueIkhlas SadiminNo ratings yet

- Inventory in Months' Supply: April 2, 2010 All Residential Properties in SANDICOR MLSDocument10 pagesInventory in Months' Supply: April 2, 2010 All Residential Properties in SANDICOR MLSa4agarwalNo ratings yet

- ARcover Brochure Final1Document2 pagesARcover Brochure Final1Esther LeeNo ratings yet

- Sapphire Textile Mills Limited Corporate Briefing 2022Document20 pagesSapphire Textile Mills Limited Corporate Briefing 2022mahnoorabbasi2589No ratings yet

- Apple 3 Statement Model 1717230434Document12 pagesApple 3 Statement Model 1717230434Anshik SharmaNo ratings yet

- Calculo Wacc - AlicorpDocument14 pagesCalculo Wacc - Alicorpludwing espinar pinedoNo ratings yet

- Market Report December 2022Document36 pagesMarket Report December 2022gm9sfwdmfdNo ratings yet

- Chaudhry Steel Re-Rolling Mills Limited: Consultant To The IssueDocument8 pagesChaudhry Steel Re-Rolling Mills Limited: Consultant To The IssueAbdul Wahaab KhokharNo ratings yet

- Currency Futures in India-Status Check After One Year-Vrk100-14102009Document13 pagesCurrency Futures in India-Status Check After One Year-Vrk100-14102009RamaKrishna Vadlamudi, CFANo ratings yet

- GMA Network Inc.: A Presentation of The FinancialsDocument14 pagesGMA Network Inc.: A Presentation of The FinancialsZed LadjaNo ratings yet

- NR - CRT Facturi Comb. Ig., Cosm. Hrana Telefon Intret. Lumina GAZ Net, CabluDocument2 pagesNR - CRT Facturi Comb. Ig., Cosm. Hrana Telefon Intret. Lumina GAZ Net, CablugelubotNo ratings yet

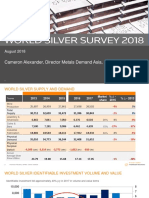

- Cameron Alexander, Director Metals Demand Asia, GFMS: August 2018Document13 pagesCameron Alexander, Director Metals Demand Asia, GFMS: August 2018Olivia JacksonNo ratings yet

- Sacco Statistics 2023-FinDocument3 pagesSacco Statistics 2023-FinbmwenjaNo ratings yet

- EMI Calculator - Prepayment OptionDocument18 pagesEMI Calculator - Prepayment Optionpranil deshmukhNo ratings yet

- Data Visualization ExercisesDocument151 pagesData Visualization ExercisesPUNITH S 1NT20BA065No ratings yet

- Gross Domestic Product (GDP) at Current PricesDocument4 pagesGross Domestic Product (GDP) at Current PricesChakma MansonNo ratings yet

- Pit e SelatanDocument1 pagePit e SelatanfajriNo ratings yet

- Wipro SFM - CIA1.1 2Document12 pagesWipro SFM - CIA1.1 2Saloni Jain 1820343No ratings yet

- Solidworks: Srikanth Kyatoor Applications Engineer Logical Solutions LTDDocument25 pagesSolidworks: Srikanth Kyatoor Applications Engineer Logical Solutions LTDNagesh BiradarNo ratings yet

- Triple - M-Trading - SARAYDocument10 pagesTriple - M-Trading - SARAYLaiza Cristella SarayNo ratings yet

- NKParmar 3Document1 pageNKParmar 3NikulNo ratings yet

- CheggDocument75 pagesCheggKaranNo ratings yet

- Financial Model Asian PaintsDocument19 pagesFinancial Model Asian Paintssantoshj423No ratings yet

- Relationship Between Hedge Profit and Jet Fuel PriceDocument4 pagesRelationship Between Hedge Profit and Jet Fuel PriceThomasNo ratings yet

- Ex - BOL Fomular (Newest)Document14 pagesEx - BOL Fomular (Newest)barcodeNo ratings yet

- FM AssignmentDocument27 pagesFM AssignmentMuhammad AkbarNo ratings yet

- Weekly Statistics: The Indonesia Stock Exchange Composite Stock Price Index and Equity Trading ValueDocument2 pagesWeekly Statistics: The Indonesia Stock Exchange Composite Stock Price Index and Equity Trading ValueGayeong KimNo ratings yet

- Book 1Document4 pagesBook 1CHARISSE ANN ANASTACIONo ratings yet

- Merchant Acquiring: How To Win in A Digital World: White PaperDocument13 pagesMerchant Acquiring: How To Win in A Digital World: White PaperMuumini De Souza NezzaNo ratings yet

- Q4 2010 Quarterly EarningsDocument15 pagesQ4 2010 Quarterly EarningsAlexia BonatsosNo ratings yet

- Presentasi - Eka Fitriyani - 110415Document17 pagesPresentasi - Eka Fitriyani - 110415reggywijaya9No ratings yet

- EMI Calculator - Prepayment OptionDocument15 pagesEMI Calculator - Prepayment OptionKiran MulyaNo ratings yet

- EMI Calculator - Prepayment OptionDocument15 pagesEMI Calculator - Prepayment OptionKiran MulyaNo ratings yet

- India Insights by IndiaQuotient - June 2024Document174 pagesIndia Insights by IndiaQuotient - June 2024Deepak J SharmaNo ratings yet

- Aahar 2024 Hallwise List of ParticipantsDocument102 pagesAahar 2024 Hallwise List of ParticipantsDeepak J SharmaNo ratings yet

- Praxis Report Modern Building Material Market Report 3Document32 pagesPraxis Report Modern Building Material Market Report 3Deepak J SharmaNo ratings yet

- IF 2024 BrochureDocument3 pagesIF 2024 BrochureDeepak J SharmaNo ratings yet

- ETP Dec23 Jan24Document60 pagesETP Dec23 Jan24Deepak J SharmaNo ratings yet

- The Recyclist Mag-Edition-2 DIGITAL WEB CorrectedDocument31 pagesThe Recyclist Mag-Edition-2 DIGITAL WEB CorrectedDeepak J SharmaNo ratings yet

- CMAI Apparel Magazine Jan-Mar 2024 PDFDocument152 pagesCMAI Apparel Magazine Jan-Mar 2024 PDFDeepak J SharmaNo ratings yet

- Material Recycling Magazine Mrai March 2024Document72 pagesMaterial Recycling Magazine Mrai March 2024Deepak J SharmaNo ratings yet

- POLYMERS Communique (Feb & Mar, 2024)Document154 pagesPOLYMERS Communique (Feb & Mar, 2024)Deepak J SharmaNo ratings yet

- ETP Feb Mar24Document56 pagesETP Feb Mar24Deepak J SharmaNo ratings yet

- TradeFlock - April 2024Document60 pagesTradeFlock - April 2024Deepak J SharmaNo ratings yet

- POLYMERS Communique - Dec 2023 - Jan 2024Document162 pagesPOLYMERS Communique - Dec 2023 - Jan 2024Deepak J SharmaNo ratings yet

- AV April Issue 2024 Web-1Document68 pagesAV April Issue 2024 Web-1Deepak J SharmaNo ratings yet

- CMAI Apparel Magazine Apr-June 2024Document142 pagesCMAI Apparel Magazine Apr-June 2024Deepak J SharmaNo ratings yet

- AEPC Apparel Mag April 2024Document64 pagesAEPC Apparel Mag April 2024Deepak J SharmaNo ratings yet

- Nacl Annual Report 2019 20Document206 pagesNacl Annual Report 2019 20Deepak J SharmaNo ratings yet

- Ardee City Judgement Feb 13Document5 pagesArdee City Judgement Feb 13Deepak J SharmaNo ratings yet

- Livestock and Poultry Improvement and ManagementDocument40 pagesLivestock and Poultry Improvement and ManagementDeepak J SharmaNo ratings yet

- Tender Document For Catering Services For Hostels 5, 7, 10, IIT BombayDocument9 pagesTender Document For Catering Services For Hostels 5, 7, 10, IIT BombayDeepak J SharmaNo ratings yet

- Package of Practices For Increasing Production: NO.3. DEC.'85Document16 pagesPackage of Practices For Increasing Production: NO.3. DEC.'85Deepak J SharmaNo ratings yet

- FWPS Vol 2 No 1 Paper 7Document20 pagesFWPS Vol 2 No 1 Paper 7030338220156No ratings yet

- Session 12Document34 pagesSession 12sgNo ratings yet

- Majumder Garments Limited: Standard Operating ProcedureDocument3 pagesMajumder Garments Limited: Standard Operating ProcedureRanjit Roy100% (2)

- H Ride Sign Furniture Handles 2014Document413 pagesH Ride Sign Furniture Handles 2014Anonymous xEJGcuNo ratings yet

- ZARA: Live The ExperienceDocument44 pagesZARA: Live The Experienceravi alwaysNo ratings yet

- Data MigrationDocument18 pagesData MigrationSai KrishnaNo ratings yet

- Muhmmad Ashraf RB - Pdf. (IR & Admin Manager)Document1 pageMuhmmad Ashraf RB - Pdf. (IR & Admin Manager)Engr AhmedNo ratings yet

- Alcisa & Pick GMBH: Small Food-Product Distributor Generates Value With Sap® Standard SolutionDocument4 pagesAlcisa & Pick GMBH: Small Food-Product Distributor Generates Value With Sap® Standard SolutionJan HarvestNo ratings yet

- UntitledDocument2 pagesUntitledI love strawberry berry berry strawberryNo ratings yet

- Material HandlingDocument54 pagesMaterial HandlingNafiul Alam SnigdhoNo ratings yet

- Business Studies ProjectDocument8 pagesBusiness Studies Projectkulmeet kaur jollyNo ratings yet

- Definition of Production ControlDocument22 pagesDefinition of Production ControlNorIshamIsmailNo ratings yet

- Hersheys Sweet VictoryDocument3 pagesHersheys Sweet Victorywanya64No ratings yet

- Guidelines For Storage and Handling Bluescope Steel 'S ProductsDocument20 pagesGuidelines For Storage and Handling Bluescope Steel 'S ProductsElieser Júnio100% (1)

- Stability in Air Cargo Handling ProcedureDocument14 pagesStability in Air Cargo Handling ProcedureMohamed Salah El DinNo ratings yet

- CAD/CAM/CIMDocument42 pagesCAD/CAM/CIMNPMYS23No ratings yet

- T.M. Bhagalpur University Bhagalpur-812007Document52 pagesT.M. Bhagalpur University Bhagalpur-812007raka kumarNo ratings yet

- Farmaid 4Document10 pagesFarmaid 4rohan2109No ratings yet

- Initial Stock Upload For Warehouse (1FU - US) : Test Script SAP S/4HANA - 15-02-22Document17 pagesInitial Stock Upload For Warehouse (1FU - US) : Test Script SAP S/4HANA - 15-02-22MAYANK JAINNo ratings yet

- Ca Final - Strategic Cost Management and Performance Evaluation 50 Important Queestions 1670727583800681Document185 pagesCa Final - Strategic Cost Management and Performance Evaluation 50 Important Queestions 1670727583800681Gaurang ChhanganiNo ratings yet

- Opm560 INDIVIDUAL ASSIGNMENT 1Document5 pagesOpm560 INDIVIDUAL ASSIGNMENT 1AHMAD AFIQ NORMANNo ratings yet

- BC2408 Project ProposalDocument2 pagesBC2408 Project ProposalGdeNo ratings yet

- Final-Scm PPT Big BazaarDocument29 pagesFinal-Scm PPT Big BazaarNirriti Shrawan50% (2)

- Cloud Bursting MethodologyDocument40 pagesCloud Bursting MethodologyJonathan SpindelNo ratings yet

- Warehouse and Inventory Management: Unit IvDocument111 pagesWarehouse and Inventory Management: Unit IvKumar AdityaNo ratings yet

- AEC301 Online NotesDocument86 pagesAEC301 Online NotesAnanda PreethiNo ratings yet

- Hari OmDocument2 pagesHari OmHariom YadavNo ratings yet

- SAP Movement TypesDocument46 pagesSAP Movement TypesBachtiar YanuariNo ratings yet