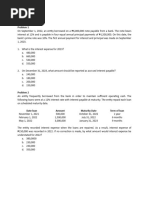

Impairment of Loans and Notes Receivable

Impairment of Loans and Notes Receivable

Download as docx, pdf, or txt

You might also like

- Audprob Answer 1Document1 pageAudprob Answer 1venice cambryNo ratings yet

- Statement Bank March Delavid Distributor LLC A2cb2f38f9Document10 pagesStatement Bank March Delavid Distributor LLC A2cb2f38f9Madelyn Vasquez100% (1)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2019 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2019 Edition)Rating: 5 out of 5 stars5/5 (1)

- Loans ReceivableDocument22 pagesLoans ReceivableJendall SisonNo ratings yet

- Mama Mo Lily I AbilitiesDocument39 pagesMama Mo Lily I AbilitiesjdNo ratings yet

- ProblemsDocument7 pagesProblemsHanna Mae Arcilla67% (6)

- MODAUD2 - Unit 3 - Audit of Accounts and Notes Payable - T31516 - FINALDocument4 pagesMODAUD2 - Unit 3 - Audit of Accounts and Notes Payable - T31516 - FINALmimi96No ratings yet

- Module 1 and 3 AssignmentDocument12 pagesModule 1 and 3 AssignmentPrincess Maeca OngNo ratings yet

- Receivables QuizDocument3 pagesReceivables QuizAshianna KimNo ratings yet

- Illustrative Examples - Notes and Loans ReceivableDocument4 pagesIllustrative Examples - Notes and Loans ReceivableMelrose Eugenio ErasgaNo ratings yet

- Loans ReceivableDocument1 pageLoans ReceivableJanidelle Swiftie67% (3)

- Loans Receivable QuizDocument2 pagesLoans Receivable Quizann chrislynNo ratings yet

- Practice Problems - Notes and Loans Receivable: General InstructionsDocument2 pagesPractice Problems - Notes and Loans Receivable: General Instructionseia aieNo ratings yet

- 4 FAR Handout Notes ReceivableDocument2 pages4 FAR Handout Notes Receivablealford sery CammayoNo ratings yet

- 19 Notes PayableDocument3 pages19 Notes Payableangelienacion8No ratings yet

- 02 Notes Loans and Bonds Payables and Debt Restructuring PDFDocument6 pages02 Notes Loans and Bonds Payables and Debt Restructuring PDFKlomoNo ratings yet

- Loans ReceivableDocument4 pagesLoans ReceivableDianna Dayawon0% (1)

- Impairment of Loans and Receivable FinancingDocument17 pagesImpairment of Loans and Receivable FinancingGelyn CruzNo ratings yet

- Week 1 OutputDocument4 pagesWeek 1 OutputFria Mae Aycardo AbellanoNo ratings yet

- 1st Compre NR and LR PDFDocument3 pages1st Compre NR and LR PDFHelton Jun M. TuralbaNo ratings yet

- Notes Receivable and Loan ImpairmentDocument2 pagesNotes Receivable and Loan ImpairmentplantationarkanaNo ratings yet

- 6991 Note PayableDocument2 pages6991 Note PayableFREE MOVIESNo ratings yet

- Far1 Notes ReceivableDocument4 pagesFar1 Notes ReceivableRico Jay EmejasNo ratings yet

- 3 - Accounting For Loans and ImpairmentDocument1 page3 - Accounting For Loans and ImpairmentReese AyessaNo ratings yet

- BP - ProblemsDocument3 pagesBP - ProblemsNhel AlvaroNo ratings yet

- 07 Loans Receivable - (Multiple)Document3 pages07 Loans Receivable - (Multiple)kyle mandaresioNo ratings yet

- Acc412 Pe QuestionsDocument5 pagesAcc412 Pe QuestionsMa Teresa B. CerezoNo ratings yet

- Problem 77Document1 pageProblem 77YukidoNo ratings yet

- Drills Notes Receivable To Discounting of ReceivableDocument3 pagesDrills Notes Receivable To Discounting of ReceivableVincent AbellaNo ratings yet

- Sample Problem - Notes Receivable and Loan ImpairmentDocument4 pagesSample Problem - Notes Receivable and Loan ImpairmentYashi SantosNo ratings yet

- Chapter 14Document4 pagesChapter 14ks1043210No ratings yet

- Far Quiz 2Document13 pagesFar Quiz 2Shiela Jane CrismundoNo ratings yet

- Answer Key - M1L2 PDFDocument4 pagesAnswer Key - M1L2 PDFEricka Mher IsletaNo ratings yet

- Prelim Examination 2018 With AnswersDocument6 pagesPrelim Examination 2018 With Answersjudel ArielNo ratings yet

- Prelim Examination 2018 With Answers PDFDocument6 pagesPrelim Examination 2018 With Answers PDFjudel ArielNo ratings yet

- AE 111 Final Summative Assessment 1Document3 pagesAE 111 Final Summative Assessment 1Djunah ArellanoNo ratings yet

- Chapter 2Document8 pagesChapter 2cindyNo ratings yet

- HW On ReceivablesDocument4 pagesHW On ReceivablesGian Carlo RamonesNo ratings yet

- Receivables ProblemsDocument4 pagesReceivables ProblemsLarpii MonameNo ratings yet

- ACCTGREV1 - 002 Notes Payable and RestructuringDocument2 pagesACCTGREV1 - 002 Notes Payable and RestructuringRenz Angel M. RiveraNo ratings yet

- Activity 7 Financial Liabilities P 1Document2 pagesActivity 7 Financial Liabilities P 1Dianne Mei Tagabi CastroNo ratings yet

- Receivable-to-Receivable-Financing (PRACTICE)Document3 pagesReceivable-to-Receivable-Financing (PRACTICE)liezelkatemesina82No ratings yet

- ReviewerDocument19 pagesReviewerLyca Jane OlamitNo ratings yet

- Chapter 1 Liabilities ExercisesDocument3 pagesChapter 1 Liabilities ExercisesAwish FernNo ratings yet

- ACCOUNTING 2 - ProblemsDocument6 pagesACCOUNTING 2 - ProblemsJasmin NoblezaNo ratings yet

- Drill 1 (15 Marks) : General Direction: Place On A Separate Sheet of Paper and Show Supporting Solutions in Good FormDocument3 pagesDrill 1 (15 Marks) : General Direction: Place On A Separate Sheet of Paper and Show Supporting Solutions in Good FormKaye GonxalesNo ratings yet

- 7103 - Notes Receivable and Loan ImpairmentDocument2 pages7103 - Notes Receivable and Loan ImpairmentGerardo YadawonNo ratings yet

- QUIZ 1 Part 1Document2 pagesQUIZ 1 Part 1Jerah Marie PepitoNo ratings yet

- Quiz 5 ReceivablesDocument1 pageQuiz 5 ReceivablesPanda ErarNo ratings yet

- Loan Receivable 6Document1 pageLoan Receivable 6Mitos Cielo NavajaNo ratings yet

- Audit of Liabilities No AnsDocument16 pagesAudit of Liabilities No AnsG18 Yna RecintoNo ratings yet

- Chapters 5-6: Use The Following For The Next Two QuestionsDocument4 pagesChapters 5-6: Use The Following For The Next Two QuestionsSherri BonquinNo ratings yet

- HW On Receivables CDocument5 pagesHW On Receivables CAmjad Rian MangondatoNo ratings yet

- Borrowing Cost ProbDocument10 pagesBorrowing Cost ProbYoite MiharuNo ratings yet

- HW On Receivables ADocument3 pagesHW On Receivables Aebranola0423No ratings yet

- Exercise LiabilitiesDocument2 pagesExercise LiabilitiesAlaine Milka GosycoNo ratings yet

- Midterm Quizzes Compilation - Docx-1Document91 pagesMidterm Quizzes Compilation - Docx-1Yess poooNo ratings yet

- CE On Receivables T2 AY2021Document4 pagesCE On Receivables T2 AY2021Gian Carlo RamonesNo ratings yet

- Finding Balance 2019: Benchmarking the Performance of State-Owned Banks in the PacificFrom EverandFinding Balance 2019: Benchmarking the Performance of State-Owned Banks in the PacificNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Problems of Bangladesh Garments Sector and Their Solution - An Islamic PerspectiveDocument1 pageProblems of Bangladesh Garments Sector and Their Solution - An Islamic PerspectiveSalman Khaled BariNo ratings yet

- CH 9Document79 pagesCH 9Manmeet Kaur AroraNo ratings yet

- Introduction To Accounting PrinciplesDocument4 pagesIntroduction To Accounting PrinciplesJess CaburnayNo ratings yet

- Corporate Governance ReportDocument10 pagesCorporate Governance Reportmd.akibulalam1100No ratings yet

- FM Testbank Ch04Document16 pagesFM Testbank Ch04David LarryNo ratings yet

- 4.7. Major Theories of Regional IntegrationsDocument14 pages4.7. Major Theories of Regional Integrationssolomon GebreNo ratings yet

- Woodshire M3M GGNDocument50 pagesWoodshire M3M GGNManish Ranjan100% (1)

- Accounting For Receivables: Weygandt - Kieso - KimmelDocument49 pagesAccounting For Receivables: Weygandt - Kieso - KimmelHaftom YitbarekNo ratings yet

- Technological Globalization - Examples, Pros and ConsDocument2 pagesTechnological Globalization - Examples, Pros and ConsTarek Souheil100% (1)

- 5Document38 pages5Rei Ian G. CabeguinNo ratings yet

- 1.abolition of The Slave TradeDocument2 pages1.abolition of The Slave TradeNEO MLILONo ratings yet

- Jawaban MGT BiayaDocument9 pagesJawaban MGT BiayaRessa LiniNo ratings yet

- 4201 (Previous Year Questions)Document13 pages4201 (Previous Year Questions)Tanjid MahadyNo ratings yet

- GO No.119 SET BACKSDocument2 pagesGO No.119 SET BACKSmadhav0303No ratings yet

- Gold StandardDocument21 pagesGold StandardIhsan Ullah HimmatNo ratings yet

- Unit-3 Public ExpenditureDocument27 pagesUnit-3 Public ExpendituremelaNo ratings yet

- IMF Study Guide SMUN2030Document15 pagesIMF Study Guide SMUN2030kimaNo ratings yet

- INR One Thousand One Hundred and Ninety Nine Rupees and Zero Paise Only Tax Is Payable On Reverse Charge Basis: No E. & O.EDocument1 pageINR One Thousand One Hundred and Ninety Nine Rupees and Zero Paise Only Tax Is Payable On Reverse Charge Basis: No E. & O.EKamlesh PatelNo ratings yet

- Cf23a1ibm DSMM Fbe Course ScheduleDocument1 pageCf23a1ibm DSMM Fbe Course ScheduleVishwa NirmalaNo ratings yet

- Chapter 1 AgendaDocument4 pagesChapter 1 AgendaAndres BoteroNo ratings yet

- PDB-Gross Domestic Product (GDP) - InggrisDocument7 pagesPDB-Gross Domestic Product (GDP) - InggrisPradiptaAdiPamungkasNo ratings yet

- Murabaha - Application (Trade Finance)Document72 pagesMurabaha - Application (Trade Finance)Riz Khan100% (2)

- Paris: Capital of The Nineteenth Century?Document6 pagesParis: Capital of The Nineteenth Century?Gordon ChanNo ratings yet

- Endorsements by Pick N Pay Top Management For Extraordinary Success in Opening New Mega-Store, Migrating Staff From Another Mega-Store and MoreDocument15 pagesEndorsements by Pick N Pay Top Management For Extraordinary Success in Opening New Mega-Store, Migrating Staff From Another Mega-Store and MoreDirk CoetzeeNo ratings yet

- 2021 Ems GR 9 Poa Grade 9 Ems 2021 Assessment PlanDocument2 pages2021 Ems GR 9 Poa Grade 9 Ems 2021 Assessment PlannicolemalumaneNo ratings yet

- Sonic WhitepaperDocument9 pagesSonic Whitepapert.pentzekNo ratings yet

- Balance Sheet of Axis Bank: MoneyDocument13 pagesBalance Sheet of Axis Bank: MoneyNaresh KumarNo ratings yet

- Contoh-Soal-Managerial-Accounting BinusDocument7 pagesContoh-Soal-Managerial-Accounting Binuswiwinsusiani1991No ratings yet

- UntitledDocument5 pagesUntitledmujahid.aliNo ratings yet