Gov. 16-17

Gov. 16-17

Download as pdf or txt

You might also like

- Dps Custodial Terms Conditions February2021v25 1Document6 pagesDps Custodial Terms Conditions February2021v25 1mexiso3561No ratings yet

- Accounting Last Push-GautengDocument26 pagesAccounting Last Push-GautengYolisa NkosiNo ratings yet

- Audit of Sole ProprietorDocument9 pagesAudit of Sole ProprietorPrincess Bhavika100% (2)

- CCEDocument3 pagesCCESofia Nadine100% (1)

- Unit-2 Audit of Cash and Marketable SecuritiesDocument6 pagesUnit-2 Audit of Cash and Marketable SecuritiesKiya AbdiNo ratings yet

- Chapter 24 AnsDocument10 pagesChapter 24 AnsDave Manalo100% (1)

- Chapter06 - Answer PDFDocument6 pagesChapter06 - Answer PDFAvon Jade RamosNo ratings yet

- Chapter 9Document10 pagesChapter 9Jesther John Vocal100% (2)

- Actg1 - Chapter 3Document37 pagesActg1 - Chapter 3Reynaleen Agta100% (1)

- Chapter 16 - Corporate GovernanceDocument34 pagesChapter 16 - Corporate Governancekarryl barnuevoNo ratings yet

- Chapter 20 - Answer PDFDocument10 pagesChapter 20 - Answer PDFjhienellNo ratings yet

- MO-09- Performing Auditing and Reporting Level IV(1)Document32 pagesMO-09- Performing Auditing and Reporting Level IV(1)Mesfin AberaNo ratings yet

- Audit II CH 02 Audit of cash and cassh equivalentDocument12 pagesAudit II CH 02 Audit of cash and cassh equivalentantenehNo ratings yet

- Chapter 13 Before You Go OnDocument4 pagesChapter 13 Before You Go Onpatricianguyen1997No ratings yet

- 1) Audit of Investment in Financial InstrumentDocument6 pages1) Audit of Investment in Financial InstrumentMaxene Joi PigtainNo ratings yet

- Audit of CashDocument15 pagesAudit of CashZelalem Hassen100% (1)

- Index: SR - No. Particulars SignatureDocument20 pagesIndex: SR - No. Particulars SignatureMohammedAhmedRazaNo ratings yet

- Auditing and Corporate Governanc1Document26 pagesAuditing and Corporate Governanc1clash with devilNo ratings yet

- Auditing and Corporate Governanc Py SolvedDocument10 pagesAuditing and Corporate Governanc Py Solvedclash with devilNo ratings yet

- Chapter 2 Audit of CashDocument11 pagesChapter 2 Audit of Cashadinew abeyNo ratings yet

- Auditing and Corporate Governanc1Document26 pagesAuditing and Corporate Governanc1clash with devilNo ratings yet

- Chapter-2: Audit of Cash and Marketable SecuritiesDocument27 pagesChapter-2: Audit of Cash and Marketable Securitiesbikilahussen100% (1)

- Trust AuditDocument4 pagesTrust Auditswt123421No ratings yet

- Audit Objectives and Procedures: HapterDocument121 pagesAudit Objectives and Procedures: HapterabdellaNo ratings yet

- Audit - CASH AND INVESTMENTS AUDITDocument7 pagesAudit - CASH AND INVESTMENTS AUDITIulia BurtoiuNo ratings yet

- How To Conduct A Financial AuditDocument4 pagesHow To Conduct A Financial AuditSherleen GallardoNo ratings yet

- 6th Sessiom - Audit of Investment STUDENTDocument17 pages6th Sessiom - Audit of Investment STUDENTNIMOTHI LASENo ratings yet

- Chapter06 - Answer PDFDocument6 pagesChapter06 - Answer PDFJONAS VINCENT SamsonNo ratings yet

- Untitled Document 1Document4 pagesUntitled Document 1GESPEJO, JC SHEEN O.No ratings yet

- Basic Concepts in AuditingDocument29 pagesBasic Concepts in Auditinganon_672065362100% (1)

- CH 10Document25 pagesCH 10Eric Yao100% (1)

- Chapter 06 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Document73 pagesChapter 06 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Awais Azeemi33% (3)

- Audit of Specialized Industry Banking PDFDocument7 pagesAudit of Specialized Industry Banking PDFLovely-Lou LaurenaNo ratings yet

- Auditing - Review Material 4Document50 pagesAuditing - Review Material 4KathleenNo ratings yet

- Ch18 SolutionsDocument8 pagesCh18 Solutionschaplain80No ratings yet

- Chapter 2 AUDIT OF CASH& MARKETABLE SECURITYDocument7 pagesChapter 2 AUDIT OF CASH& MARKETABLE SECURITYsteveiamidNo ratings yet

- 01 Unit 1-Audit of LiabilitiesDocument9 pages01 Unit 1-Audit of Liabilitieskara albueraNo ratings yet

- 2019 Answers AuditingDocument16 pages2019 Answers Auditingdhanush.rNo ratings yet

- CashDocument15 pagesCashGizaw BelayNo ratings yet

- Substantive Test of InvestmentsDocument57 pagesSubstantive Test of Investmentsjulia4razoNo ratings yet

- Chapter 19 - Answer PDFDocument12 pagesChapter 19 - Answer PDFjhienellNo ratings yet

- Asynchronous Audit Assurance RapasDocument2 pagesAsynchronous Audit Assurance RapasQueen RapasNo ratings yet

- Chapter 6Document14 pagesChapter 6Genanew AbebeNo ratings yet

- VouchingDocument16 pagesVouchingJones MaryNo ratings yet

- Chapter 1 - AACA P1Document7 pagesChapter 1 - AACA P1Toni Rose Hernandez LualhatiNo ratings yet

- Mahusay Module 4 - Acc4115Document4 pagesMahusay Module 4 - Acc4115Jeth MahusayNo ratings yet

- 100 MCQ TestBankDocument18 pages100 MCQ TestBankMaricrisNo ratings yet

- CLASS NOTES Topic 9 Internal ControlSystemsDocument14 pagesCLASS NOTES Topic 9 Internal ControlSystemsKiasha WarnerNo ratings yet

- Bunwin Residence: Is The Company Profitable??Document6 pagesBunwin Residence: Is The Company Profitable??Pum MineaNo ratings yet

- Substantive Test OF Shareholders' EquityDocument46 pagesSubstantive Test OF Shareholders' EquityAldrin John TungolNo ratings yet

- VouchingDocument8 pagesVouchingGyanesh DoshiNo ratings yet

- Audit of Cash Nov. 2016Document22 pagesAudit of Cash Nov. 2016tekalignyohannesNo ratings yet

- H. Investments, Including Investments in AffiliatesDocument15 pagesH. Investments, Including Investments in AffiliatesadelmariaracelleNo ratings yet

- Auditing NotesDocument65 pagesAuditing NotesTushar GaurNo ratings yet

- Murabah ProfitDocument15 pagesMurabah ProfitMuhammad ZulkifulNo ratings yet

- Bba 301Document10 pagesBba 301rohanNo ratings yet

- The Importance of Cash Flow StatementDocument2 pagesThe Importance of Cash Flow StatementBeboy TorregosaNo ratings yet

- AAT Paper 2 FinanceDocument4 pagesAAT Paper 2 FinanceRay LaiNo ratings yet

- Textbook of Urgent Care Management: Chapter 13, Financial ManagementFrom EverandTextbook of Urgent Care Management: Chapter 13, Financial ManagementNo ratings yet

- Mastering Bookkeeping: Unveiling the Key to Financial SuccessFrom EverandMastering Bookkeeping: Unveiling the Key to Financial SuccessNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Unit 2 - Global & Colombian Financial ServicesDocument8 pagesUnit 2 - Global & Colombian Financial ServicesHenry Fabian Diaz GaviriaNo ratings yet

- Overview of Financial Management and The Financial EnvironmentDocument37 pagesOverview of Financial Management and The Financial EnvironmentZardar Rafid Sayeed 2025078660No ratings yet

- Ans and Ques OracleDocument18 pagesAns and Ques OracleAMJ TELNo ratings yet

- Deferred AnnuityDocument22 pagesDeferred AnnuityCaitlin TishNo ratings yet

- 6-Constantino v. CuisiaDocument3 pages6-Constantino v. CuisiaChristian Ivan Daryl DavidNo ratings yet

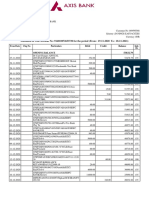

- Statement of Axis Account No:916010072653730 For The Period (From: 19-11-2020 To: 18-11-2021)Document7 pagesStatement of Axis Account No:916010072653730 For The Period (From: 19-11-2020 To: 18-11-2021)asphalt 9 legendsNo ratings yet

- Exercicios Chapter2e3 IPM BKMDocument8 pagesExercicios Chapter2e3 IPM BKMLuis CarneiroNo ratings yet

- Namma Kalvi 11th Accountancy Important 2 Mark and 3 Mark Questions em 218018Document2 pagesNamma Kalvi 11th Accountancy Important 2 Mark and 3 Mark Questions em 218018Madhumitha KNo ratings yet

- MoneyDocument6 pagesMoneyritoja770No ratings yet

- Multi-Class Text Classification With Scikit-LearnDocument20 pagesMulti-Class Text Classification With Scikit-LearnmohitNo ratings yet

- Amortization Schedule (SmartEMI 13383.02)Document2 pagesAmortization Schedule (SmartEMI 13383.02)ckrish918No ratings yet

- Escrow AgreementDocument4 pagesEscrow AgreementSaeed Al HemeiriNo ratings yet

- Ebill 100048857457Document6 pagesEbill 100048857457cahaya izNo ratings yet

- Accounting MCQsDocument59 pagesAccounting MCQsdhabekarsharvari07No ratings yet

- Working CapitalDocument7 pagesWorking CapitalSreenath SreeNo ratings yet

- UNION BANKDocument12 pagesUNION BANKbhargavaaddala5No ratings yet

- xpbLuNuw 2022-09-02T05 34 56Document1 pagexpbLuNuw 2022-09-02T05 34 56katealderson331No ratings yet

- Credit Risk Management of Sonali Bank LimitedDocument72 pagesCredit Risk Management of Sonali Bank Limitedsumaiya sumaNo ratings yet

- b1 English Unlimited Coursebook Pre Intpdf PDF FreeDocument178 pagesb1 English Unlimited Coursebook Pre Intpdf PDF FreeKeith Stone ArellanoNo ratings yet

- Home OwnershipDocument3 pagesHome OwnershipChrisNo ratings yet

- Short Story-SummaryDocument5 pagesShort Story-Summaryqueensmiling495No ratings yet

- Assignment 1 - Digital "SWOT" Analysis of Industry: StrengthsDocument3 pagesAssignment 1 - Digital "SWOT" Analysis of Industry: StrengthsPrashant BharadwajNo ratings yet

- Cash and Cash Equivalents C5 Valix 2006Document5 pagesCash and Cash Equivalents C5 Valix 2006Ghaill CruzNo ratings yet

- 04 BELL, Stephanie e Wray, L. Randall. Fiscal Effects On Reserves and The In-Dependence of The FedDocument11 pages04 BELL, Stephanie e Wray, L. Randall. Fiscal Effects On Reserves and The In-Dependence of The FedGuilherme UchimuraNo ratings yet

- CSR ApplicationDetails SVCBank 2023Document1 pageCSR ApplicationDetails SVCBank 2023chaitanya5310No ratings yet

- Internship Report On Faysal Bank Limited by Naeem AhmedDocument36 pagesInternship Report On Faysal Bank Limited by Naeem AhmedNaeem Ahmed75% (12)

- Financial AccountingDocument11 pagesFinancial AccountingSHIKHA DWIVEDINo ratings yet