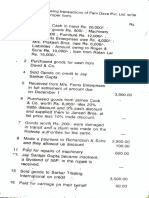

Rectification of Error Important Adjustment for ca foundation

Rectification of Error Important Adjustment for ca foundation

Download as pdf or txt

You might also like

- ELE Case Analysis Made With ChatGPTDocument27 pagesELE Case Analysis Made With ChatGPTNikhil Seth100% (1)

- All About The DripDocument17 pagesAll About The DripNaitik Jain100% (1)

- Rectification of Errors - QuestionsDocument6 pagesRectification of Errors - QuestionsBhargav RavalNo ratings yet

- ROE - Class Work SolutionDocument15 pagesROE - Class Work Solutiontokyo3384No ratings yet

- Screenshot 2024-12-09 at 8.11.26 PMDocument3 pagesScreenshot 2024-12-09 at 8.11.26 PMDev DuttNo ratings yet

- Rectification of ErrorsDocument63 pagesRectification of Errorspeven28003No ratings yet

- 3 - Trial Balance To PL Account - ExamplesDocument49 pages3 - Trial Balance To PL Account - ExamplesDivyansh Pandey100% (2)

- Journal, Ledger, TB & Final AccountsDocument11 pagesJournal, Ledger, TB & Final AccountsSanjay Dutta100% (1)

- MAA Assignment RKDocument9 pagesMAA Assignment RKKrishna RayasamNo ratings yet

- 1june 2009 1 J E Accounts 2Document18 pages1june 2009 1 J E Accounts 2Pravah ShuklaNo ratings yet

- Basics & Journal Entry of AccountancyDocument45 pagesBasics & Journal Entry of AccountancyPrincipal MHK, AnklleshwarNo ratings yet

- What Are The 3 Types of Accounts in Accounting?: What Is An Account?Document8 pagesWhat Are The 3 Types of Accounts in Accounting?: What Is An Account?ShubhamNo ratings yet

- EntryDocument4 pagesEntryShankha MaitiNo ratings yet

- tally practical q1Document2 pagestally practical q1yashchauhan13700No ratings yet

- 5 FMA Sesskion-5Document4 pages5 FMA Sesskion-5Ashish KumawatNo ratings yet

- CA Foundation Accounts Recodring of Transactions StudentsDocument57 pagesCA Foundation Accounts Recodring of Transactions StudentsRockyNo ratings yet

- Financial Accounting & AnalysisDocument3 pagesFinancial Accounting & Analysisdasdona577No ratings yet

- Correction of ErrorsDocument5 pagesCorrection of Errorsmuhammad arifNo ratings yet

- CNP 2211 Account Suggested AnswerDocument16 pagesCNP 2211 Account Suggested AnswermridulNo ratings yet

- Rectification of Errors: Accountancy - II 1Document3 pagesRectification of Errors: Accountancy - II 1M JEEVARATHNAM NAIDUNo ratings yet

- 5.Rules of Debit and CreditDocument11 pages5.Rules of Debit and CreditjetshrisinghNo ratings yet

- Exam Paper - Financial Accounting - SolnDocument5 pagesExam Paper - Financial Accounting - SolnakkyNo ratings yet

- CFN 9305 Accounts Suggested Answers PDFDocument4 pagesCFN 9305 Accounts Suggested Answers PDFDivya PunjabiNo ratings yet

- Paper5 Solution Set1Document15 pagesPaper5 Solution Set1Alokkumar BeheraNo ratings yet

- Financial Management & Cost Accounting: Lesson 6 Introduction To JournalDocument4 pagesFinancial Management & Cost Accounting: Lesson 6 Introduction To JournalAmit Kr GodaraNo ratings yet

- Accounting For Receivables: Both AR and NR Are Called Trade ReceivablesDocument7 pagesAccounting For Receivables: Both AR and NR Are Called Trade ReceivablesKhaled Abo YousefNo ratings yet

- Unit 2C - II Rectification of ErrorsDocument62 pagesUnit 2C - II Rectification of Errorsrandom07111No ratings yet

- JournalDocument20 pagesJournalgili khannaNo ratings yet

- Particulars: Rs. RsDocument7 pagesParticulars: Rs. RsAnmol ChawlaNo ratings yet

- 110-Chapter 3 - Books of Original Entry-Journal - WMDocument21 pages110-Chapter 3 - Books of Original Entry-Journal - WMaaditya kumar jhaNo ratings yet

- Answer Key of Rectification of Errors 2Document3 pagesAnswer Key of Rectification of Errors 2menekyakiaNo ratings yet

- Assignment QuestionsDocument12 pagesAssignment QuestionsyogendradilwalaNo ratings yet

- Adobe Scan 15 Apr 2024Document17 pagesAdobe Scan 15 Apr 2024irfu1323No ratings yet

- Acctg Na Di Pa TaposDocument1 pageAcctg Na Di Pa TaposCharles BeringuelNo ratings yet

- t s grewal solution ch 18_watermarkDocument52 pagest s grewal solution ch 18_watermarkDeepak SinghNo ratings yet

- Rectifiation of Error With Suspense AccountDocument3 pagesRectifiation of Error With Suspense AccountSudharshan GNo ratings yet

- Special Journals Part 2Document4 pagesSpecial Journals Part 2rahlroy79No ratings yet

- Chapter - 05 Rectification of ErrorsDocument5 pagesChapter - 05 Rectification of ErrorsPayal SinghNo ratings yet

- Correction of Errors and Suspense AccountDocument34 pagesCorrection of Errors and Suspense AccountPatric CletusNo ratings yet

- Journal EntriesDocument2 pagesJournal EntriespratyushNo ratings yet

- Forfeiture of Shares AhanaDocument3 pagesForfeiture of Shares AhanapranavNo ratings yet

- Accounting For Share Capital - DPP 09 (Of Lec 10) - Kautilya 2025Document5 pagesAccounting For Share Capital - DPP 09 (Of Lec 10) - Kautilya 2025singh.akshat20077No ratings yet

- Accounting IntroductionDocument4 pagesAccounting Introductionpranav1931129No ratings yet

- XII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)Document7 pagesXII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)naviagrawal2006No ratings yet

- Basic Jornal Accounting Pratice 1Document20 pagesBasic Jornal Accounting Pratice 1Lakshya AgrawalNo ratings yet

- XII-D-Issue of Shares Test TPSDocument2 pagesXII-D-Issue of Shares Test TPSumangchh2306No ratings yet

- Adobe Scan Aug 29, 2022-1Document5 pagesAdobe Scan Aug 29, 2022-1Piyush GoyalNo ratings yet

- Tally Prime-1Document8 pagesTally Prime-1Sanjeev kumarNo ratings yet

- TallyDocument23 pagesTallySatya PalNo ratings yet

- Faa AssignmentDocument4 pagesFaa AssignmentHitesh SinghNo ratings yet

- Show Your Working Clearly.: AccountancyDocument8 pagesShow Your Working Clearly.: AccountancyYash SardaNo ratings yet

- Sample PaperDocument5 pagesSample PaperPriyanshi KarNo ratings yet

- FA Question Bank TT1-1Document14 pagesFA Question Bank TT1-1rock SINGHALNo ratings yet

- MB131 - 2003 - 10 (October)Document31 pagesMB131 - 2003 - 10 (October)nilshalinNo ratings yet

- Class 11 Final QDocument13 pagesClass 11 Final QadabandwanNo ratings yet

- Analysis of Transactions-Recording Process-Journal EntriesDocument30 pagesAnalysis of Transactions-Recording Process-Journal Entrieshammad buttNo ratings yet

- Ledger and Trial BalanceDocument24 pagesLedger and Trial BalanceMd.Amir hossain khan100% (1)

- Accounting NotesDocument4 pagesAccounting NotesGhulam MustafaNo ratings yet

- Yuvraj Sahni Xii Commerce C AccountsDocument27 pagesYuvraj Sahni Xii Commerce C AccountskalomaNo ratings yet

- Journal Ledger & Trial BalanceDocument11 pagesJournal Ledger & Trial BalanceTushar SahuNo ratings yet

- 9 Product ManagementDocument45 pages9 Product Managementjasonwong.viaNo ratings yet

- Sample TestDocument15 pagesSample TestSoofeng LokNo ratings yet

- FINA 5120 - Fall (1) 2022 - Session 1 - The Corporation Financial Statements - 26aug22Document75 pagesFINA 5120 - Fall (1) 2022 - Session 1 - The Corporation Financial Statements - 26aug22Yilin YANGNo ratings yet

- Cambridge IGCSE: Accounting 0452/12Document16 pagesCambridge IGCSE: Accounting 0452/12jpranav611.hNo ratings yet

- MATH3075 3975 Course Notes 2012Document104 pagesMATH3075 3975 Course Notes 2012ttdbaoNo ratings yet

- Support ResistanceDocument128 pagesSupport Resistancemonucool100% (1)

- Retained Earnings Short TestDocument2 pagesRetained Earnings Short TestAngelica CastilloNo ratings yet

- 1 - Intro To FinanceDocument23 pages1 - Intro To FinanceYudna YuNo ratings yet

- Gome ElectricalsDocument6 pagesGome ElectricalsAmit Srivastava100% (1)

- Chapter 1 Introduction To Finance For EntrepreneursDocument36 pagesChapter 1 Introduction To Finance For EntrepreneursKS YamunaNo ratings yet

- International Marketing V1ADocument10 pagesInternational Marketing V1Asolvedcare100% (1)

- Amb220 Exam NoteDocument59 pagesAmb220 Exam NoteYING ZUONo ratings yet

- Group No 3 AssignmentDocument4 pagesGroup No 3 AssignmentWinifridaNo ratings yet

- Junr ProjectDocument44 pagesJunr ProjectAvinash GunnaNo ratings yet

- Service Failures and Recovery in Tourism and Hospitality: A Practical ManualDocument15 pagesService Failures and Recovery in Tourism and Hospitality: A Practical Manualanita galihNo ratings yet

- Courageous Growth Six Strategies For Continuous Growth OutperformanceDocument12 pagesCourageous Growth Six Strategies For Continuous Growth OutperformanceiamamitxsinghNo ratings yet

- (2021 2022) ACCA FM 基础 答案册Document22 pages(2021 2022) ACCA FM 基础 答案册luoyifei1988No ratings yet

- (Free Version 2.0) Map of 119 E-Commerce MetricsDocument1 page(Free Version 2.0) Map of 119 E-Commerce Metricsmateus miyanoNo ratings yet

- MKTG101 Marketing Fundamentals: Associate Professor Ross GordonDocument46 pagesMKTG101 Marketing Fundamentals: Associate Professor Ross Gordonnatalievns1999No ratings yet

- Kwame Nkrumah University of Science and Technololgy College of Arts and Social Sciences School of BusinessDocument5 pagesKwame Nkrumah University of Science and Technololgy College of Arts and Social Sciences School of BusinessYAKUBU ISSAHAKU SAIDNo ratings yet

- Ashapura Minchem Pvt. LTDDocument63 pagesAshapura Minchem Pvt. LTDPravin chavdaNo ratings yet

- The IHSEnergy JVHandbookDocument24 pagesThe IHSEnergy JVHandbooktubi251103No ratings yet

- Research ProposalDocument19 pagesResearch ProposalAdnan Yusufzai75% (4)

- Cash Vs Accrual Accounting 1Document65 pagesCash Vs Accrual Accounting 1Nassir CeellaabeNo ratings yet

- 2 Just For FEET Case Analysis REWRITEDocument7 pages2 Just For FEET Case Analysis REWRITEJuris Renier MendozaNo ratings yet

- Assignment#1 JhbeloyDocument1 pageAssignment#1 JhbeloyJeffrey BeloyNo ratings yet

- Game Results - ZensimuDocument5 pagesGame Results - Zensimuyash10.gaurNo ratings yet

- As Business (Workbook)Document142 pagesAs Business (Workbook)Muhammad RafayNo ratings yet