0% found this document useful (0 votes)

53 views57 pagesProject Cash Flow Analysis Techniques

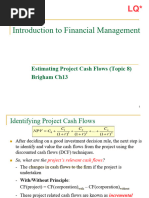

Chapter 12 discusses the principles and methodologies for analyzing project cash flows, focusing on incremental cash flows relevant to project valuation, forecasting cash flows for investments, and the impact of inflation. It outlines the steps for calculating cash flows, including depreciation, working capital, and capital expenditures, and provides examples of operating cash flow and net present value (NPV) calculations. The chapter also differentiates between expansion and replacement projects, emphasizing the importance of understanding cash flow differences in decision-making.

Uploaded by

engr.nakib.tcclCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

53 views57 pagesProject Cash Flow Analysis Techniques

Chapter 12 discusses the principles and methodologies for analyzing project cash flows, focusing on incremental cash flows relevant to project valuation, forecasting cash flows for investments, and the impact of inflation. It outlines the steps for calculating cash flows, including depreciation, working capital, and capital expenditures, and provides examples of operating cash flow and net present value (NPV) calculations. The chapter also differentiates between expansion and replacement projects, emphasizing the importance of understanding cash flow differences in decision-making.

Uploaded by

engr.nakib.tcclCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd