Recording Business Transactions in Primary Books

Recording Business Transactions in Primary Books

Download as ppt, pdf, or txt

You might also like

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDocument131 pagesFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- Accounting TransactionsDocument28 pagesAccounting TransactionsPaolo100% (1)

- Journal To Final AccountsDocument38 pagesJournal To Final Accountsguptagaurav131166100% (5)

- Information System For Managers CompleteDocument350 pagesInformation System For Managers Completenkr2294No ratings yet

- How To Deliver Consumer Insigh PDFDocument8 pagesHow To Deliver Consumer Insigh PDFmaNo ratings yet

- Com Stack Configuration PDFDocument99 pagesCom Stack Configuration PDFkakathi100% (1)

- Building BridgesDocument42 pagesBuilding BridgesMelrose Valenciano83% (12)

- 02-General Ledger AccountingDocument96 pages02-General Ledger AccountingRirinNo ratings yet

- BUSN7008 Week 2 Recording Business TransactionsDocument37 pagesBUSN7008 Week 2 Recording Business TransactionsberfamenNo ratings yet

- Double EntryDocument14 pagesDouble EntryHuleshwar Kumar Singh100% (1)

- The Financial StatementDocument35 pagesThe Financial Statementmouhammad mouhammadNo ratings yet

- Presentation On Accounting BasicDocument20 pagesPresentation On Accounting BasicKrishna Kumar SinghNo ratings yet

- Lecture#3 ContinueDocument45 pagesLecture#3 ContinueBeluga GamerTMNo ratings yet

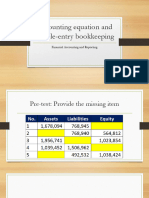

- Accounting Equation and Double Entry BookkeepingDocument29 pagesAccounting Equation and Double Entry BookkeepingArvin ToraldeNo ratings yet

- CFAB Accounting Chap02 Accounting EquationDocument38 pagesCFAB Accounting Chap02 Accounting EquationHoa NguyễnNo ratings yet

- Basic AccountingDocument32 pagesBasic AccountinghectorbaladingNo ratings yet

- By: Ms. Pakeezah ButtDocument18 pagesBy: Ms. Pakeezah ButtHusnain MustafaNo ratings yet

- Accounting Concepts and ProcessDocument39 pagesAccounting Concepts and Processtlalengmohapi256No ratings yet

- PA NoteDocument73 pagesPA NoteChi PhanNo ratings yet

- Financial Accounting - Information For Decisions - Session 1 - Chapter 2 PPT pBGEaElvpiDocument27 pagesFinancial Accounting - Information For Decisions - Session 1 - Chapter 2 PPT pBGEaElvpimukul3087_305865623No ratings yet

- Chapter3+4UsingT-Accounts 2Document37 pagesChapter3+4UsingT-Accounts 2الغيثيNo ratings yet

- Debit and CreditDocument33 pagesDebit and CreditBasma ShaalanNo ratings yet

- Session 2 - Income Statement and Transaction AnalysisDocument42 pagesSession 2 - Income Statement and Transaction Analysishieucaiminh155No ratings yet

- Types of Accounting AccountsDocument44 pagesTypes of Accounting AccountsAzhar Hussain100% (2)

- 2 Accounting StatementsDocument50 pages2 Accounting Statementswanangwa nyasuluNo ratings yet

- CHAPTER 1 - PPT Intro To AccountingDocument14 pagesCHAPTER 1 - PPT Intro To AccountingAmrinNo ratings yet

- PPT 2 - Business TransactionDocument29 pagesPPT 2 - Business Transactionthinkaboutbe14No ratings yet

- Lesson 2 - Recording The Business TransactionsDocument6 pagesLesson 2 - Recording The Business TransactionsUnknownymousNo ratings yet

- Chapter 02Document50 pagesChapter 02Huy HoangNo ratings yet

- CH 2 Accounting TransactionsDocument52 pagesCH 2 Accounting TransactionsGizachew100% (1)

- Supplementary 1 - Financial StatementsDocument21 pagesSupplementary 1 - Financial StatementsQuốc Khánh100% (1)

- BUSN1001 Week 2 Lecture Notes S22018 - 1 Slide Per PageDocument29 pagesBUSN1001 Week 2 Lecture Notes S22018 - 1 Slide Per PageXinyue WangNo ratings yet

- Chapter 7Document39 pagesChapter 7juls100% (1)

- Debit and Credit Rules of AccountingDocument17 pagesDebit and Credit Rules of Accountingarafatchan4189No ratings yet

- Debit and CreditDocument32 pagesDebit and CreditBasma ShaalanNo ratings yet

- Topic 6 Accounting SystemDocument21 pagesTopic 6 Accounting SystemkengabluxNo ratings yet

- Basics of AccountingDocument30 pagesBasics of AccountingNaina_Dwivedi_6514No ratings yet

- FINA2010 Financial Management: Lecture 2: Financial Statement AnalysisDocument68 pagesFINA2010 Financial Management: Lecture 2: Financial Statement AnalysismoonNo ratings yet

- Rules of Determining Debit & Credit PDFDocument26 pagesRules of Determining Debit & Credit PDFasadurrahman40100% (1)

- Accounting Mechanics Basic RecordsDocument30 pagesAccounting Mechanics Basic Recordsvaibhav bhavsarNo ratings yet

- Module 4 - Double Entry Bookkeeping System and The Accounting EquationDocument9 pagesModule 4 - Double Entry Bookkeeping System and The Accounting EquationMark Christian BrlNo ratings yet

- Accounting - Basics - Deloitte. 1Document56 pagesAccounting - Basics - Deloitte. 1Shubh100% (1)

- Accountancy PPT 1Document22 pagesAccountancy PPT 1sakshamNo ratings yet

- The Recording Process: Pertemuan Ke-3Document39 pagesThe Recording Process: Pertemuan Ke-3Nadhiela AdaniNo ratings yet

- Finance+Webinar 13.12.2022++updatedDocument42 pagesFinance+Webinar 13.12.2022++updatedJasmine ChoudharyNo ratings yet

- FABM1 - Lesson 2Document18 pagesFABM1 - Lesson 2christinejgualbertoNo ratings yet

- Grade 9update9learnersampleDocument11 pagesGrade 9update9learnersampleJohanet NawrattelNo ratings yet

- Chapter 11 Bookkeeping EntrepDocument37 pagesChapter 11 Bookkeeping EntrepJacel GadonNo ratings yet

- Introduction To Financial Accounting (FFA/FAB) : DR Ahmad AlshehabiDocument55 pagesIntroduction To Financial Accounting (FFA/FAB) : DR Ahmad AlshehabiKye SimpsonNo ratings yet

- Professional Accounting PackageDocument72 pagesProfessional Accounting PackageAnmol poudelNo ratings yet

- Lecture 4 - Income StatementDocument78 pagesLecture 4 - Income StatementMutesa ChrisNo ratings yet

- Accounting BasicsDocument21 pagesAccounting BasicsasifparwezNo ratings yet

- Financial AccountingDocument14 pagesFinancial Accountingnalla maheshNo ratings yet

- Accounting - 2. The Accounting ProcessDocument19 pagesAccounting - 2. The Accounting ProcessChi Kei KeungNo ratings yet

- 4ACCN002W Lecture 2 - TaggedDocument47 pages4ACCN002W Lecture 2 - Taggedredwaanmo19No ratings yet

- Chapter 2Document25 pagesChapter 2Jose Carlos SouzaNo ratings yet

- L2 - Accounting Equation & Transaction Analysis - Edited With AnsswerDocument39 pagesL2 - Accounting Equation & Transaction Analysis - Edited With AnsswerEslam SamyNo ratings yet

- Accounting FundamentalsDocument40 pagesAccounting FundamentalsPriyanka GoswamiNo ratings yet

- Accounting Equation & Financial ReportingDocument36 pagesAccounting Equation & Financial ReportingAnelisa IvyNo ratings yet

- Week 2 Slides - Balance SheetDocument15 pagesWeek 2 Slides - Balance SheetThura HtetNo ratings yet

- 29.8fin AccountingDocument97 pages29.8fin AccountingVrushie100% (1)

- Notes of Double Entry System and Journal EntryDocument35 pagesNotes of Double Entry System and Journal Entryjune100% (1)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Dr. Erlinda D. San Juan, PHDDocument2 pagesDr. Erlinda D. San Juan, PHDGlenn Binasahan ParcoNo ratings yet

- Lady MacbethDocument3 pagesLady Macbethapi-357833762No ratings yet

- Samplex WillsDocument2 pagesSamplex WillsPaula Jane EscasinasNo ratings yet

- Grila Programe (Digitala) Next GenDocument1 pageGrila Programe (Digitala) Next GenMarius MihailaNo ratings yet

- Organizational Analysis: A Case Study of TVS Motor CompanyDocument46 pagesOrganizational Analysis: A Case Study of TVS Motor CompanyHemant RanaNo ratings yet

- CASE DIGEST Capitol WirelessDocument2 pagesCASE DIGEST Capitol WirelessErica Dela Cruz100% (3)

- Circ3 2004Document2 pagesCirc3 2004Gavin HenningNo ratings yet

- 2016 Bluto RL & Reba: Service ManualDocument33 pages2016 Bluto RL & Reba: Service ManualjackNo ratings yet

- Sampung Halamang GamotDocument5 pagesSampung Halamang GamotSister RislyNo ratings yet

- List of Common Irregular Past Tense VerbsDocument3 pagesList of Common Irregular Past Tense VerbsAli RazaNo ratings yet

- Water Quality Measurement Using PH Sensor With Raspberry PiDocument5 pagesWater Quality Measurement Using PH Sensor With Raspberry Pippg gggNo ratings yet

- Conjunctions: in Spite Of/ Despite His Money, He Is Not HappyDocument5 pagesConjunctions: in Spite Of/ Despite His Money, He Is Not HappyGV Lê Thị Thuý Hà 24 THPT Sông LôNo ratings yet

- Matrimonial RitesDocument8 pagesMatrimonial RitesBryan YuNo ratings yet

- Gandhi Irwin Pact Upsc Notes 43Document2 pagesGandhi Irwin Pact Upsc Notes 43Jekobin YumnamNo ratings yet

- Sample Observation Schedule 1 2Document5 pagesSample Observation Schedule 1 2Rica RegisNo ratings yet

- Diploma Year 1 General Building and Construction NotesDocument147 pagesDiploma Year 1 General Building and Construction Notessimonwanjiku598No ratings yet

- Caliwan V OcampoDocument1 pageCaliwan V Ocampo001nooneNo ratings yet

- Pattern High Resolution Melman and Pi TarturumiesDocument10 pagesPattern High Resolution Melman and Pi Tarturumiesfarkasnemkati100% (2)

- Chapter - 02 Tense VOLUME 1 EXERCISE PRACTICE (1-57)Document43 pagesChapter - 02 Tense VOLUME 1 EXERCISE PRACTICE (1-57)kirti singlaNo ratings yet

- Dav DZ570KDocument96 pagesDav DZ570KNguyen van HienNo ratings yet

- Namil Vs ComelecDocument2 pagesNamil Vs ComelecOceane AdolfoNo ratings yet

- Dispatch listCOST RICADocument1 pageDispatch listCOST RICADavid YepezNo ratings yet

- CHAPTER 3 - The Revised Chart of AccountsDocument16 pagesCHAPTER 3 - The Revised Chart of AccountsRafael VictoriaNo ratings yet

- Environmental Management Plan - Method StatementDocument3 pagesEnvironmental Management Plan - Method StatementmemekenyaNo ratings yet

- MV 82Document2 pagesMV 820selfNo ratings yet

- Economic Development After World War IIDocument10 pagesEconomic Development After World War IIhira khalid kareemNo ratings yet