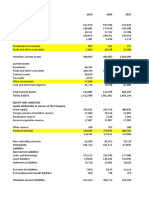

Inditex

Inditex

Download as pptx, pdf, or txt

You might also like

- Case 3-Mueller-Lehmkuhl GMBH Final CaseDocument8 pagesCase 3-Mueller-Lehmkuhl GMBH Final CaseQuyên QuyênNo ratings yet

- FsaDocument13 pagesFsaday6 favorite, loveNo ratings yet

- Forex Freedom - Break Free of The Bonds That Are Holding You BackDocument66 pagesForex Freedom - Break Free of The Bonds That Are Holding You BackJao100% (1)

- Petron Corp - Financial Analysis From 2014 - 2018Document4 pagesPetron Corp - Financial Analysis From 2014 - 2018Neil Nadua100% (1)

- Ferrari Excel Group1Document78 pagesFerrari Excel Group1DavidNo ratings yet

- Principles of Marketing (First Quarter)Document5 pagesPrinciples of Marketing (First Quarter)roseller100% (6)

- Essay To Be First Mover in A Business, You Do Not Have To Have Market AnalysisDocument3 pagesEssay To Be First Mover in A Business, You Do Not Have To Have Market AnalysisHaniatun HanieNo ratings yet

- FinShiksha Maruti Suzuki UnsolvedDocument12 pagesFinShiksha Maruti Suzuki UnsolvedGANESH JAINNo ratings yet

- Section A - Group 9Document17 pagesSection A - Group 9AniketNo ratings yet

- Financial Statement Model For The Clorox Company: Company Name Latest Fiscal YearDocument10 pagesFinancial Statement Model For The Clorox Company: Company Name Latest Fiscal YearArslan HafeezNo ratings yet

- Latihan Tugas ALK - Prospective AnalysisDocument3 pagesLatihan Tugas ALK - Prospective AnalysisSelvy MonibollyNo ratings yet

- Hoa Sen Group OfficialDocument28 pagesHoa Sen Group OfficialBảo TrungNo ratings yet

- M Saeed 20-26 ProjectDocument30 pagesM Saeed 20-26 ProjectMohammed Saeed 20-26No ratings yet

- Fauji Fertilizer Company Limited: Consolidated Balance SheetDocument5 pagesFauji Fertilizer Company Limited: Consolidated Balance Sheetnasir mehmoodNo ratings yet

- Sultan Drug Corporation-CaseDocument5 pagesSultan Drug Corporation-CaseSohad ElnagarNo ratings yet

- IndusDocument5 pagesIndusFateen HabibNo ratings yet

- Financial Statements Analysis: Arsalan FarooqueDocument31 pagesFinancial Statements Analysis: Arsalan FarooqueMuhib NoharioNo ratings yet

- Crescent Textile Mills LTD AnalysisDocument23 pagesCrescent Textile Mills LTD AnalysisMuhammad Noman MehboobNo ratings yet

- Drreddy - Ratio AnalysisDocument8 pagesDrreddy - Ratio AnalysisNavneet SharmaNo ratings yet

- AlaphabeatDocument22 pagesAlaphabeatsinghsourav12002No ratings yet

- Financial Plan For A Start UpDocument12 pagesFinancial Plan For A Start UpNayab ArshadNo ratings yet

- FIN 440 Group Task 1Document104 pagesFIN 440 Group Task 1দিপ্ত বসুNo ratings yet

- 5 EstadosDocument15 pages5 EstadosHenryRuizNo ratings yet

- Financial Analysis of Security Paper Limited (Ifra Arshad 2016-Ag-7558)Document9 pagesFinancial Analysis of Security Paper Limited (Ifra Arshad 2016-Ag-7558)IfraNo ratings yet

- DG Khan Cement Financial StatementsDocument8 pagesDG Khan Cement Financial StatementsAsad BumbiaNo ratings yet

- EVA ExampleDocument27 pagesEVA Examplewelcome2jungleNo ratings yet

- Vertical AnalysisDocument3 pagesVertical AnalysisJayvee CaguimbalNo ratings yet

- Final Report - Draft2Document32 pagesFinal Report - Draft2shyamagniNo ratings yet

- Report CalculationsDocument2 pagesReport CalculationsammassumairNo ratings yet

- Millat Tractors - Final (Sheraz)Document20 pagesMillat Tractors - Final (Sheraz)Adeel SajidNo ratings yet

- Hershey's Ratios AnalysisDocument21 pagesHershey's Ratios AnalysisJunciNo ratings yet

- Infosys Consolidated Financial Statements 03.2017Document12 pagesInfosys Consolidated Financial Statements 03.2017Anonymous 1cmtBqNo ratings yet

- Assignment 3 - SolutionDocument3 pagesAssignment 3 - Solutionshaeel ashrafNo ratings yet

- Ratio Analysis of Engro Vs NestleDocument24 pagesRatio Analysis of Engro Vs NestleMuhammad SalmanNo ratings yet

- 5 6120493211875018431Document62 pages5 6120493211875018431Hafsah Amod DisomangcopNo ratings yet

- Ratio AnalysisDocument9 pagesRatio AnalysisGg JjNo ratings yet

- Deferred Tax Asset Retirement Benefit Assets: TotalDocument2 pagesDeferred Tax Asset Retirement Benefit Assets: TotalSrb RNo ratings yet

- IFRS FinalDocument69 pagesIFRS FinalHardik SharmaNo ratings yet

- Ajinkya Patil - SIP ReportDocument23 pagesAjinkya Patil - SIP ReportNikeeta BhagatNo ratings yet

- Balance Sheet: AssetsDocument19 pagesBalance Sheet: Assetssumeer shafiqNo ratings yet

- Fundamental AnalysisDocument4 pagesFundamental AnalysisMuhammad AkmalNo ratings yet

- Final Analysis Indusind Bank Annual ReportpdfDocument45 pagesFinal Analysis Indusind Bank Annual ReportpdfVishalNo ratings yet

- Indus Dyeing & Manufacturing Co. LTD: Horizontal Analysis of Financial StatementsDocument12 pagesIndus Dyeing & Manufacturing Co. LTD: Horizontal Analysis of Financial StatementsSaad NaeemNo ratings yet

- Indus Dyeing & Manufacturing Co. LTD: Horizontal Analysis of Financial StatementsDocument12 pagesIndus Dyeing & Manufacturing Co. LTD: Horizontal Analysis of Financial StatementsSaad NaeemNo ratings yet

- FSP LinaDocument43 pagesFSP LinaAlina Binte EjazNo ratings yet

- Ratios Unsolved Company BDocument4 pagesRatios Unsolved Company BdebojyotiNo ratings yet

- Audited Financial Statement 2011Document31 pagesAudited Financial Statement 2011Angelica LanaNo ratings yet

- Donam Corporate FinanceDocument9 pagesDonam Corporate FinanceMAGOMU DAN DAVIDNo ratings yet

- MCB Financial AnalysisDocument30 pagesMCB Financial AnalysisMuhammad Nasir Khan100% (4)

- Company Overview - Davis IndustriesDocument5 pagesCompany Overview - Davis Industriessamarth halliNo ratings yet

- Extract From The Warehouse Group Financial Statement With Analyses - AlbanyDocument11 pagesExtract From The Warehouse Group Financial Statement With Analyses - Albanyjoehe2625No ratings yet

- A1.2 Roic TreeDocument9 pagesA1.2 Roic Treesara_AlQuwaifliNo ratings yet

- Act B - Horizontal AnalysisDocument5 pagesAct B - Horizontal AnalysisIsn't bitterness it's the truthNo ratings yet

- Profitability Ratio: Chittagong Independent University Assignment OnDocument6 pagesProfitability Ratio: Chittagong Independent University Assignment OnShafayet JamilNo ratings yet

- Project Company Subject Group Group Members: GC University FaisalabadDocument23 pagesProject Company Subject Group Group Members: GC University FaisalabadMuhammad Tayyab RazaNo ratings yet

- ABS-CBN Corporation and Subsidiaries Consolidated Statements of Financial Position (Amounts in Thousands)Document10 pagesABS-CBN Corporation and Subsidiaries Consolidated Statements of Financial Position (Amounts in Thousands)Mark Angelo BustosNo ratings yet

- W18826 XLS EngDocument11 pagesW18826 XLS EngNini HuanachinNo ratings yet

- ABC LTD.: Income Statement (Consolidated)Document7 pagesABC LTD.: Income Statement (Consolidated)Kushal PandyaNo ratings yet

- Rafhan Maize Products Company LTDDocument10 pagesRafhan Maize Products Company LTDALI SHER HaidriNo ratings yet

- Company Overview - Davis IndustriesDocument4 pagesCompany Overview - Davis IndustriesdeepikaNo ratings yet

- HP Autonomy QuestionDocument3 pagesHP Autonomy Questionqiaocheng2023No ratings yet

- Balance Sheet and Leverage RatiosDocument5 pagesBalance Sheet and Leverage Ratiosdudutomy67No ratings yet

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Case 1: Custom Fabricators, Inc.: Critical Success Factors Core CompetenciesDocument3 pagesCase 1: Custom Fabricators, Inc.: Critical Success Factors Core CompetenciesZed LadjaNo ratings yet

- Bitcoin ExplosionDocument15 pagesBitcoin Explosioninformation nabilNo ratings yet

- FAR 2 Finals Cheat SheetDocument8 pagesFAR 2 Finals Cheat SheetILOVE MATURED FANSNo ratings yet

- Focusing On Customers: Teaching NotesDocument45 pagesFocusing On Customers: Teaching NotesNop-q Djanlord Esteban BelenNo ratings yet

- Dove CaseDocument2 pagesDove CaseAmeya0% (1)

- Marketing Management Full Notes Mba AnirudhDocument308 pagesMarketing Management Full Notes Mba AnirudhKumaran Thayumanavan100% (1)

- Weather Forecasting and Energy Trading: Notes From The TrenchesDocument16 pagesWeather Forecasting and Energy Trading: Notes From The TrenchesviniNo ratings yet

- Internship Report in SipradiDocument25 pagesInternship Report in SipradiSanim Amatya38% (8)

- Reading Summary: Channel Management Group 8Document3 pagesReading Summary: Channel Management Group 8RohanMohapatraNo ratings yet

- Retailing: Types of RetailersDocument3 pagesRetailing: Types of RetailersNur SrianaNo ratings yet

- Project Report: Submitted byDocument44 pagesProject Report: Submitted byM O H I T S I N G HNo ratings yet

- Mastering FMCG Sales - For Sales and Marketing ProfessionalsDocument136 pagesMastering FMCG Sales - For Sales and Marketing ProfessionalsNavonil BasuNo ratings yet

- New STPDDocument40 pagesNew STPDAsad khanNo ratings yet

- Brochure Shahajiraje Mahavidyalaya Khatav... - 1Document7 pagesBrochure Shahajiraje Mahavidyalaya Khatav... - 1digitalromNo ratings yet

- Group6 - 07TP1Document21 pagesGroup6 - 07TP1Katherine BernalNo ratings yet

- Capital Structure Few ProblemsDocument2 pagesCapital Structure Few ProblemsKalyani ParmalNo ratings yet

- Portfolio Management Process (Condensed)Document17 pagesPortfolio Management Process (Condensed)sadamNo ratings yet

- 5paisa Capital Limited: Account Opening FormDocument13 pages5paisa Capital Limited: Account Opening FormYaswanth YasuNo ratings yet

- Crea Insights - Corporate BrochureDocument20 pagesCrea Insights - Corporate BrochureNajeemudeen K.PNo ratings yet

- 5c) Stock LedgerDocument2 pages5c) Stock LedgerMartin J PulsNo ratings yet

- Albrechts Value-Process FrameworkDocument22 pagesAlbrechts Value-Process FrameworkMariver LlorenteNo ratings yet

- Anog Nove Angel TolitsDocument3 pagesAnog Nove Angel TolitsArlene GarciaNo ratings yet

- Chapter 01 IntroductionDocument33 pagesChapter 01 IntroductionTanha RupontiNo ratings yet

- Practical Accounting II - 2nd PreboardDocument9 pagesPractical Accounting II - 2nd PreboardKim Cristian Maaño0% (1)

- All MCQ Managerial EconomicsDocument12 pagesAll MCQ Managerial Economicsasish kumar MohapatraNo ratings yet

- Determinants of SupplyDocument4 pagesDeterminants of SupplyBhea GutierrezNo ratings yet