Portfolio Management of Money Market Funds

Portfolio Management of Money Market Funds

Download as pptx, pdf, or txt

You might also like

- Louisiana Bar Exam Must KnowDocument33 pagesLouisiana Bar Exam Must Knowbadmojo8100% (3)

- Types of Investmen T: Business Finance Quarter 2 - Module 1Document34 pagesTypes of Investmen T: Business Finance Quarter 2 - Module 1Bea Dione Pascual Cardinez100% (1)

- 1 +Traxion+-+Offering+Memo+FinalDocument431 pages1 +Traxion+-+Offering+Memo+Finalhectorsh13No ratings yet

- 3 - Long Term Sources of FinanceDocument49 pages3 - Long Term Sources of FinanceGaurav TewaniNo ratings yet

- Investment Banking: 2021 BatchDocument135 pagesInvestment Banking: 2021 Batchaditya.babarNo ratings yet

- 01 - Stocks Bonds Funds and ETFsDocument283 pages01 - Stocks Bonds Funds and ETFsGabriel TNo ratings yet

- Econ 111 - Monetary Economics: Summer Session I Tue-Thu, 5:00PM - 7:50PM Center Hall 216 Dr. Hisham FoadDocument18 pagesEcon 111 - Monetary Economics: Summer Session I Tue-Thu, 5:00PM - 7:50PM Center Hall 216 Dr. Hisham FoadJayant Kumar JhaNo ratings yet

- Mutual Funds - 1.1Document24 pagesMutual Funds - 1.1Ritik KhandelwalNo ratings yet

- Corporate FinanceDocument36 pagesCorporate FinanceCHARAK RAYNo ratings yet

- Guillemet Futures On Managed FuturesDocument4 pagesGuillemet Futures On Managed FuturesGuillemet FuturesNo ratings yet

- Mutual FundDocument27 pagesMutual FundDinesh sawNo ratings yet

- J M Financials: Investment Banking/ Securities /research / Financing and Distribution / Wealth MGNT/ Asset MGNTDocument29 pagesJ M Financials: Investment Banking/ Securities /research / Financing and Distribution / Wealth MGNT/ Asset MGNTJisha Puthanveettil MuraleedharanNo ratings yet

- TBACCharge 1Document42 pagesTBACCharge 1ZerohedgeNo ratings yet

- Introducción A Las FinanzasDocument47 pagesIntroducción A Las FinanzasLeslyNo ratings yet

- Unit 9Document21 pagesUnit 9aditipatil3733No ratings yet

- Financial Management: FINA 6212Document81 pagesFinancial Management: FINA 6212Yuhan KENo ratings yet

- Mutual FundsDocument23 pagesMutual FundsAaziya ANo ratings yet

- What Is A Mutual Fund?Document45 pagesWhat Is A Mutual Fund?pinkukoolNo ratings yet

- 2 Financial Markets and InstrumentsDocument31 pages2 Financial Markets and InstrumentsMd parvezsharifNo ratings yet

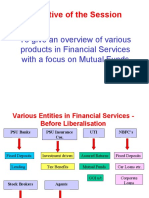

- Objective of The Session To Give AnDocument66 pagesObjective of The Session To Give Anganeshbba044No ratings yet

- Ch2ppt UpdatedDocument41 pagesCh2ppt UpdatedKoon Sing ChanNo ratings yet

- Unit 3 Student Book Outcome BDocument31 pagesUnit 3 Student Book Outcome Bnomanchowdhury2006No ratings yet

- Inve$Tment BankingDocument36 pagesInve$Tment BankingAnonymous So5qPSnNo ratings yet

- Time Value of Moneytks19Document63 pagesTime Value of Moneytks19Udita GopalkrishnaNo ratings yet

- 1-Fixed Income Defining ElementsDocument33 pages1-Fixed Income Defining Elementsdormammu 12No ratings yet

- Interest Rates and Interest Rate DeterminationDocument46 pagesInterest Rates and Interest Rate DeterminationiluvoracleNo ratings yet

- Asset Classes and Financial Instruments: Bodie, Kane and Marcus 9 Global EditionDocument48 pagesAsset Classes and Financial Instruments: Bodie, Kane and Marcus 9 Global EditionDyan Palupi WidowatiNo ratings yet

- Presentation1 PDFDocument27 pagesPresentation1 PDFAyesha NaseemNo ratings yet

- Recent Developments in Credit Derivatives Market and The Challenges For JapanDocument20 pagesRecent Developments in Credit Derivatives Market and The Challenges For Japansonakush1523No ratings yet

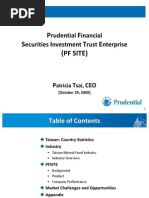

- Prudential Financial: Securities Investment Trust Enterprise (Patricia Tsai)Document27 pagesPrudential Financial: Securities Investment Trust Enterprise (Patricia Tsai)National Press FoundationNo ratings yet

- LU3 - Business Economic Forecasting NEWDocument26 pagesLU3 - Business Economic Forecasting NEWSHOBANA96No ratings yet

- US TreasuryDocument34 pagesUS Treasury吴孝伟No ratings yet

- FX MrktsDocument46 pagesFX MrktsSoe Group 1No ratings yet

- PhilippinesDocument25 pagesPhilippinesBrokennyNo ratings yet

- w11 3 Investing, Taxation and Debt Part 1 SVDocument26 pagesw11 3 Investing, Taxation and Debt Part 1 SVZhong MattNo ratings yet

- FRR-ALM Ch1Document69 pagesFRR-ALM Ch1Marek KurzyńskiNo ratings yet

- 7 Saving, Investment, and The Financial SystemDocument38 pages7 Saving, Investment, and The Financial SystemMUHAMMAD AWAIS100% (1)

- Definition of Money MarketsDocument21 pagesDefinition of Money Marketsnelle de leonNo ratings yet

- NISM All 1 To 12Document107 pagesNISM All 1 To 12Aakhazhya MNo ratings yet

- T11-Mutual FundsDocument43 pagesT11-Mutual Fundssujit guptaNo ratings yet

- Module 3 - Mutual Funds - StudentDocument68 pagesModule 3 - Mutual Funds - StudentDivtej SinghNo ratings yet

- Bond Markets: Financial Markets and Institutions, 10e, Jeff MaduraDocument38 pagesBond Markets: Financial Markets and Institutions, 10e, Jeff MaduraYoga AdiNo ratings yet

- BU FE445 - Lecture2Document31 pagesBU FE445 - Lecture2JolNo ratings yet

- Bodie Investments CH04Document28 pagesBodie Investments CH04rafat.jalladNo ratings yet

- RAMID Souhail Final Exam Case StudyDocument38 pagesRAMID Souhail Final Exam Case Studyjean.jacquesNo ratings yet

- Unit 1Document32 pagesUnit 1rishavNo ratings yet

- the-orange-bookDocument7 pagesthe-orange-bookDeepak KumarNo ratings yet

- Lecture2 2022Document47 pagesLecture2 2022ngbee222No ratings yet

- FMI - Module III - Mutual Funds - shared with students (1)Document56 pagesFMI - Module III - Mutual Funds - shared with students (1)Harsh GhaiNo ratings yet

- Basic Interest Rates Day 1Document15 pagesBasic Interest Rates Day 1Jovan SsenkandwaNo ratings yet

- Finmar ReportingDocument18 pagesFinmar ReportingJanna Rae BionganNo ratings yet

- Business Finance Q2 W1 Mod1checkedDocument13 pagesBusiness Finance Q2 W1 Mod1checkedLeonila Oca100% (5)

- Business Finance:: Lending and Job Creation in The 21 CenturyDocument31 pagesBusiness Finance:: Lending and Job Creation in The 21 CenturyyqqconstanceNo ratings yet

- Policy Considerations Before Bank Privatization - Country ExperienceDocument35 pagesPolicy Considerations Before Bank Privatization - Country ExperienceVikash KumarNo ratings yet

- Lecturenote 1 2 24Document27 pagesLecturenote 1 2 24채영No ratings yet

- Chap 2 - Material (Student)Document5 pagesChap 2 - Material (Student)Nguyễn TuấnNo ratings yet

- CH 01Document37 pagesCH 01dotpaprikaNo ratings yet

- Mutual Fund: Prof. Shriram NerlekarDocument167 pagesMutual Fund: Prof. Shriram Nerlekarhimanshu sikarwarNo ratings yet

- MarketDocument37 pagesMarketvcj87wbxnnNo ratings yet

- Financial Market & InstitutionsDocument37 pagesFinancial Market & Institutionsborsepratik30No ratings yet

- Mutual Funds: Sheenu Arora Jasmeet KaurDocument28 pagesMutual Funds: Sheenu Arora Jasmeet KaurSheenu AroraNo ratings yet

- Data (China) Interest Rate and Money Supply From 1983-2013 Year Interest Rate Money SupplyDocument7 pagesData (China) Interest Rate and Money Supply From 1983-2013 Year Interest Rate Money SupplyHogo DewenNo ratings yet

- China's Currency ConundrumDocument3 pagesChina's Currency ConundrumHogo DewenNo ratings yet

- Price Ratios and Valuation For Tenaga Nasional BHD (5347) From MorningstarDocument1 pagePrice Ratios and Valuation For Tenaga Nasional BHD (5347) From MorningstarHogo DewenNo ratings yet

- An Introduction To Portfolio ManagementDocument11 pagesAn Introduction To Portfolio ManagementHogo DewenNo ratings yet

- ConclusionDocument1 pageConclusionHogo DewenNo ratings yet

- Macroeconomic Determinants of Exchange Rate Pass-Through in India?Document15 pagesMacroeconomic Determinants of Exchange Rate Pass-Through in India?Hogo DewenNo ratings yet

- Response To Cholesky One S.D. Innovations: Response of LER To LER Response of LER To LEXDocument3 pagesResponse To Cholesky One S.D. Innovations: Response of LER To LER Response of LER To LEXHogo DewenNo ratings yet

- Empirical ResultsDocument6 pagesEmpirical ResultsHogo DewenNo ratings yet

- Econometric AssignmentDocument12 pagesEconometric AssignmentHogo DewenNo ratings yet

- Article Review and ConclusionDocument2 pagesArticle Review and ConclusionHogo DewenNo ratings yet

- Computation of DividendsDocument29 pagesComputation of DividendsGela Blanca SantiagoNo ratings yet

- Carp and Carper LawDocument44 pagesCarp and Carper LawCoreine Valledor-SarragaNo ratings yet

- Company Registration ProcessDocument53 pagesCompany Registration ProcessAhmed RazaNo ratings yet

- Credit Risk Interview QuestionsDocument2 pagesCredit Risk Interview QuestionsharshadspatilNo ratings yet

- Twiga Cement Annual Report Final 2012 PDFDocument76 pagesTwiga Cement Annual Report Final 2012 PDFSportskenya TmNo ratings yet

- Financial AccountingDocument36 pagesFinancial Accountingkhanafsha100% (2)

- Mini Test 01Document10 pagesMini Test 01HoàngTrungHiếuNo ratings yet

- Alloting SharesDocument3 pagesAlloting Sharesisaac setabiNo ratings yet

- Expectations TheoryDocument10 pagesExpectations TheorywanNo ratings yet

- Money and Banking Week 3Document16 pagesMoney and Banking Week 3Pradipta NarendraNo ratings yet

- DinoTech J V Exec Sum (1) X 2 X 2 Christian 12 30Document7 pagesDinoTech J V Exec Sum (1) X 2 X 2 Christian 12 30Christian DobrofskyNo ratings yet

- Liu Lejot & Arner Finance in Asia: Institutions, Regulation & PolicyDocument29 pagesLiu Lejot & Arner Finance in Asia: Institutions, Regulation & PolicyPaul LejotNo ratings yet

- Notes of Written AbilityDocument70 pagesNotes of Written AbilityMahi GaneshNo ratings yet

- Manufacturing EZDocument6 pagesManufacturing EZJoshua GenoviaNo ratings yet

- Ankit .M. Tripathi: University of MumbaiDocument47 pagesAnkit .M. Tripathi: University of MumbaipradeepbandiNo ratings yet

- Course Revision Corporate Finance 1 - ACCT 224: Revised Course (Brief) OutlineDocument4 pagesCourse Revision Corporate Finance 1 - ACCT 224: Revised Course (Brief) OutlineFoisal Ahmed MirzaNo ratings yet

- "Customer's Perception Towards Equity Trading With Anagram Stock Broking LimitedDocument48 pages"Customer's Perception Towards Equity Trading With Anagram Stock Broking Limitedkrishna9040No ratings yet

- Ic 38 Mock TestDocument71 pagesIc 38 Mock Testdeepuzz100% (1)

- Home Loans Project ReportDocument105 pagesHome Loans Project Reportkaushal2442No ratings yet

- Capital Adequacy Ratio - Wikipedia, The Free EncyclopediaDocument4 pagesCapital Adequacy Ratio - Wikipedia, The Free EncyclopediaTrần Kim ChungNo ratings yet

- Ratios Test PaperDocument7 pagesRatios Test Papermeesam2100% (1)

- Financial LitDocument23 pagesFinancial LitAnonymous swEjW5ncYNo ratings yet

- New Dgt-1 Form - Per 10-0817Document14 pagesNew Dgt-1 Form - Per 10-0817Jesslyn PermatasariNo ratings yet

- Revised CCG Checklist 2012Document15 pagesRevised CCG Checklist 2012Apa SughraNo ratings yet

- SFO Feb11Document96 pagesSFO Feb11AbgreenNo ratings yet

- 06 - Raising Equity CapitalDocument46 pages06 - Raising Equity CapitalAnurag PattekarNo ratings yet

- Characteristics of The Stocks and Bonds In: 7twelveDocument3 pagesCharacteristics of The Stocks and Bonds In: 7twelveadamcohen81No ratings yet

- "Introductory" Lecture: Orest V. Iftime University of Groningen, The Netherlands March 2013Document42 pages"Introductory" Lecture: Orest V. Iftime University of Groningen, The Netherlands March 2013Andreea PavelNo ratings yet