This document discusses installment liquidation of a partnership. It defines installment liquidation as a process where assets are realized and cash is periodically distributed to partners as it becomes available. It outlines key principles like distributing cash only after liabilities and expenses are paid, and using schedules to determine safe payment amounts to partners based on their capital account balances after considering possible losses. An example partnership is provided to illustrate the journal entries and statements required for installment liquidation over three months.

This document discusses installment liquidation of a partnership. It defines installment liquidation as a process where assets are realized and cash is periodically distributed to partners as it becomes available. It outlines key principles like distributing cash only after liabilities and expenses are paid, and using schedules to determine safe payment amounts to partners based on their capital account balances after considering possible losses. An example partnership is provided to illustrate the journal entries and statements required for installment liquidation over three months.

This document discusses installment liquidation of a partnership. It defines installment liquidation as a process where assets are realized and cash is periodically distributed to partners as it becomes available. It outlines key principles like distributing cash only after liabilities and expenses are paid, and using schedules to determine safe payment amounts to partners based on their capital account balances after considering possible losses. An example partnership is provided to illustrate the journal entries and statements required for installment liquidation over three months.

This document discusses installment liquidation of a partnership. It defines installment liquidation as a process where assets are realized and cash is periodically distributed to partners as it becomes available. It outlines key principles like distributing cash only after liabilities and expenses are paid, and using schedules to determine safe payment amounts to partners based on their capital account balances after considering possible losses. An example partnership is provided to illustrate the journal entries and statements required for installment liquidation over three months.

Download as PPTX, PDF, TXT or read online from Scribd

Download as pptx, pdf, or txt

You are on page 1/ 22

CHAPTER 5: PARTNERSHIP

INSTALLMENT LIQUIDATION

Prepared by: Daneen Mitchelle G. Gastar

LIQUIDATION Is the termination of business operations or the winding up of affairs. It is a process by which: Assets are converted into cash

Liabilities are settled and

Any remaining amount is distributed to the owners

VOLUNTARY

INVOLUNTARY

LIQUIDATION • Conversion of assets REALIZATION into cash

• Settlement of claims of LIQUIDATION creditors and owners SETTLEMENT OF CLAIMS INSTALLMENT LUMP SUM LIQUIDATION

METHODS OF LIQUIDATION LUMP-SUM INSTALLMENT ALL non-cash assets are SOME of the non-cash converted to cash. assets are converted to cash. Total gain/loss on the sale is Carrying amount of any unsold allocated to the partner’s non-cash asset is considered as capital balances based on a loss which is then allocated to their P/L ratios. the partner’s capital balances based on their P/L ratio.

Actual liquidation expenses Actual and ESTIMATED

are allocated to the FUTURE liquidation expenses partner’s capital balances are allocated to the partner’s capital balances based on their based on their P/L ratios. P/L ratios. LUMP-SUM INSTALLMENT

Liabilities to OUTSIDE Liabilities to OUTSIDE

CREDITORS are FULLY CREDITORS are settled. PARTIALLY/FULLY settled.

Liabilities to INSIDE Liabilities to INSIDE CREDITORS

are PARTIALLY/FULLY settled but CREDITORS are FULLY only after the full settlement of settled. the liabilities to outside creditors. Any remaining cash is Once both liabilities to outside distributed to the owners in and inside creditors have been FULL settlement of their settled, any remaining cash less cash set aside for future interests. liquidation expenses is distributed to the owners as partial settlement of their interests. INSTALLMENT LIQUIDATION

A PROCESS WHEREBY ASSETS ARE

REALIZED ON A PIECE-MEAL BASIS.

CASH IS PERIODICALLY DISTRIBUTED TO

PARTNERS AS IT BECOMES AVAILABLE. BASIC PRINCIPLES OF INSTALLMENT LIQUIDATION DISTRIBUTE NO CASH to partners until all liabilities and actual liquidation expenses have been paid.

DISTRIBUTE CASH after every

realization period by using schedules to determine cash payments to partners. SAFE PAYMENT SCHEDULE • Shows how much cash can be “safely” paid to the partners during installment liquidation, which avoids any overpayment.

• Cash will be distributed only to partners with “CREDIT

BALANCES” after distribution of all possible losses among the partners.

POSSIBLE LOSSES INCLUDES:

1. TOTAL VALUE OF UNSOLD NON-CASH ASSETS

2. CASH WITHHELD TO PAY ANTICIPATED LIQUIDATION

EXPENSES AND UNRECORDED LIABILITIES

3. ADDT’L POSSIBLE LOSSES DUE TO INABILITY OF OTHER

DEFICIENT PARTNER TO SETTLE THEIR DEFICIENCY SAFE PAYMENT SCHEDULE SCHEDULES TO DETERMINE CASH PAYMENT TO PARTNERS CASH PRIORITY PROGRAM BASIC FORMAT OF SCHEDULE OF SAFE PAYMENTS PARTNERSHIP NAME SCHEDULE OF SAFE PAYMENTS DATE PARTNER A PARTNER B PARTNER C TOTAL

TOTAL INTEREST XXX XXX XXX XXX

LESS: RESTRICTED INTEREST XXX XXX XXX XXX

FOR POSSIBLE LOSSES

FREE INTEREST/PAYMENT XXX XXX XXX XXX

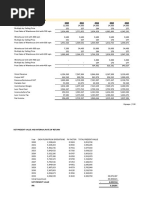

TO PARTNERS ILLUSTRATION: ASSUME THAT A, B, and C decided to liquidate their partnership. The statement of financial position as of APRIL 30, 2011 is given below. The partners share profit and loss in the ratio of 4:4:2, respectively.

A, B and C PARTNERSHIP STATEMENT OF FINANCIAL POSITION APRIL 30, 2011 ASSETS LIABILITIES AND PARTNER’S EQUITY CASH 16,000 LIABILITIES 89,600 NON-CASH ASSETS 272,000 B, LOAN 4,000 C, LOAN 6,400 A, CAPITAL 76,000 B, CAPITAL 48,000 C, CAPITAL 64,000 TOTAL 288,000 TOTAL 288,000 ADDITIONAL INFORMATION:

BOOK VALUE CASH REALIZED LOSS CASH WITHHELD

MAY-2011 120,000 90,000 30,000 5,000

JUNE-2011 100,000 60,000 40,000 2,000

JULY-2011 52,000 30,000 22,000

TOTAL 272,000 180,000 92,000 7,000

REQUIRED: PREPARE THE STATEMENT OF

LIQUIDATION FOR THE MONTHS OF MAY, JUNE AND JULY AND THE RELATED JOURNAL ENTRIES. JOURNAL ENTRIES: • TO RECORD THE MAY SALE OF NON-CASH ASSETS AND DISTRIBUTION OF LOSSES TO THE PARTNERS. MAY CASH 90,000 A, CAPITAL 12,000 B, CAPITAL 12,000 C, CAPITAL 6,000 NON-CASH ASSETS 120,000 • TO RECORD THE FULL PAYMEN OF LIABILITIES TO OUTSIDE CREDITORS LIABILITIES 89,600 CASH 89,600 • TO RECORD THE FIRST INSTALLMENT PAYMENT OF LIABILITIES TO PARTNER C C, LOAN 6,400 C, CAPITAL 5,000 CASH 11,400 • TO RECORD THE MAY SALE OF NON-CASH ASSETS AND DISTRIBUTION OF LOSSES TO THE PARTNERS. JUNE CASH 60,000 A, CAPITAL 16,000 B, CAPITAL 16,000 C, CAPITAL 8,000 NON-CASH ASSETS 100,000 • TO RECORD THE SECOND INSTALLMENT TO PARTNERS B, LOAN 2,400 A, CAPITAL 26,400 C, CAPITAL 34,200 CASH 63,000 • TO RECORD THE FINAL SALE OF NON-CASH ASSETS AND DISTRIBUTION OF LOSS TO THE PARTNERS. JULY CASH 30,000 A, CAPITAL 8,800 B, CAPITAL 8,800 C, CAPITAL 4,400 NON-CASH ASSETS 52,000 • TO RECORD THE FINAL INSTALLMENT PAYMENT TO PARTNERS B, LOAN 1,600 A, CAPITAL 12,800 B, CAPITAL 11,200 C, CAPITAL 6,400 CASH 32,000