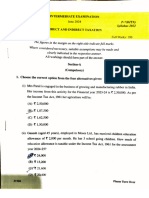

PGDM Seniors: Tax Planning and Financial Management

PGDM Seniors: Tax Planning and Financial Management

Download as ppt, pdf, or txt

You might also like

- Buckwold 21e - CH 4 Selected SolutionsDocument18 pagesBuckwold 21e - CH 4 Selected SolutionsLucy50% (2)

- Tax Planning With Refrence To Employee's RemunerationDocument34 pagesTax Planning With Refrence To Employee's RemunerationRishabh Jain83% (6)

- Unit 2 Income From SalariesDocument21 pagesUnit 2 Income From SalariesShreya SilNo ratings yet

- 1 Valuation of Perquisites 05 CRCDocument44 pages1 Valuation of Perquisites 05 CRCpratyush1200No ratings yet

- Chapter 04 Income From SalaryDocument36 pagesChapter 04 Income From SalaryWaqar AhmedNo ratings yet

- Unit 2 SalaryDocument131 pagesUnit 2 SalaryRekha BansalNo ratings yet

- Unit 2 Tax NotesDocument49 pagesUnit 2 Tax NotesP RajputNo ratings yet

- Income From EmploymentDocument19 pagesIncome From Employmentdpak bhusalNo ratings yet

- Salary Note 043704Document27 pagesSalary Note 043704mishalahammed540No ratings yet

- Income Under The Head SalaryDocument56 pagesIncome Under The Head Salaryjyoti_yadavNo ratings yet

- Notes On SalariesDocument18 pagesNotes On SalariesParul KansariaNo ratings yet

- Notes On Income From SalaryDocument5 pagesNotes On Income From SalaryNarendra KelkarNo ratings yet

- Tax Planning in Respect of Employee's Remuneration ProjrctDocument15 pagesTax Planning in Respect of Employee's Remuneration ProjrctPreyNo ratings yet

- Income From Salaries: 1. Employer-Employee RelationshipDocument25 pagesIncome From Salaries: 1. Employer-Employee RelationshipNanadan S NandaNo ratings yet

- Income from SalaryDocument13 pagesIncome from Salarybhupendra JainNo ratings yet

- Under Section 17Document6 pagesUnder Section 17ms1676514No ratings yet

- 2.1-Module 2-Part 1 PDFDocument4 pages2.1-Module 2-Part 1 PDFArpita ArtaniNo ratings yet

- Income From SalariesDocument24 pagesIncome From SalariesvnbanjanNo ratings yet

- Itl MCQDocument28 pagesItl MCQsaadnoor0554No ratings yet

- Income From SalariesDocument28 pagesIncome From SalariesAshok Kumar Meheta100% (2)

- Chapter 2: Salaries.: Computation of Income Under The Head Income From "Salaries"Document8 pagesChapter 2: Salaries.: Computation of Income Under The Head Income From "Salaries"Varun AadarshNo ratings yet

- Unit 2 Income From Salary Meaning of SalaryDocument34 pagesUnit 2 Income From Salary Meaning of SalaryrahulahujaNo ratings yet

- Unit 2 Tax NotesDocument49 pagesUnit 2 Tax NotesrahulahujaNo ratings yet

- Provident FundDocument9 pagesProvident Fundmohammed umairNo ratings yet

- Taxation - Direct and Indirect - Chapter 4 PPT MkJy53msNBDocument32 pagesTaxation - Direct and Indirect - Chapter 4 PPT MkJy53msNBRupal DalalNo ratings yet

- Salaries ITDocument14 pagesSalaries ITsaumyalilaNo ratings yet

- Acm 302 Unit-2 Ay 2024-25Document29 pagesAcm 302 Unit-2 Ay 2024-25rajavatatul063No ratings yet

- Salary Part 1Document4 pagesSalary Part 1887 shivam guptaNo ratings yet

- Income From SalaryDocument21 pagesIncome From SalaryAditya Avasare60% (10)

- Lecture-5.Income From Salaries (Sec-21)Document16 pagesLecture-5.Income From Salaries (Sec-21)imdadul haqueNo ratings yet

- 2.2-Module 2-Part 2 PDFDocument12 pages2.2-Module 2-Part 2 PDFArpita ArtaniNo ratings yet

- (Anuran) Taxation LawsDocument35 pages(Anuran) Taxation LawsAnuran BordoloiNo ratings yet

- 2.2 Module 2 Part 2Document12 pages2.2 Module 2 Part 2Arpita ArtaniNo ratings yet

- Income From SalaryDocument29 pagesIncome From SalaryIsmail SayyadNo ratings yet

- (Anuran) Taxation LawsDocument35 pages(Anuran) Taxation LawsAnuran BordoloiNo ratings yet

- Unit 1: Income From Salaries: Key PointsDocument220 pagesUnit 1: Income From Salaries: Key PointsAnkIt KRNo ratings yet

- Chapter 11 - Income TaxDocument5 pagesChapter 11 - Income TaxestamorabinNo ratings yet

- Chapter No: 1 Introduction-SalaryDocument23 pagesChapter No: 1 Introduction-SalaryMrunali kadamNo ratings yet

- Allowances Under Income Tax Act1961Document12 pagesAllowances Under Income Tax Act1961Sahil14JNo ratings yet

- Income Tax SalaryDocument28 pagesIncome Tax Salaryawanishbthk02No ratings yet

- Income From Salary (Section 12) : RsDocument8 pagesIncome From Salary (Section 12) : RsKashifNo ratings yet

- Chapter 11 Fringe Benefit TaxDocument25 pagesChapter 11 Fringe Benefit TaxVi ViNo ratings yet

- Bcoc 136 emDocument10 pagesBcoc 136 emArunNo ratings yet

- Income From SalaryDocument18 pagesIncome From SalaryKejal JainNo ratings yet

- Notes of Inome TaxDocument3 pagesNotes of Inome Taxjust4qasimNo ratings yet

- Acc 305 Module Three - Unit OneDocument8 pagesAcc 305 Module Three - Unit Onedesireheart1909No ratings yet

- Personal Income Tax Acts-1 - 034046Document10 pagesPersonal Income Tax Acts-1 - 034046temiladeadeyemi11No ratings yet

- HP - Practice Manual PDFDocument225 pagesHP - Practice Manual PDFtfytf7No ratings yet

- SALARY FormatDocument16 pagesSALARY FormatSorabh JainNo ratings yet

- Chapter-9 Salary IncomeDocument21 pagesChapter-9 Salary IncomeDhrubo Chandro RoyNo ratings yet

- WWW - Du.ac - in Fileadmin DU Academics Course Material TM 05Document24 pagesWWW - Du.ac - in Fileadmin DU Academics Course Material TM 05prince_arora90No ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Income Tax (B.com Ii)Document9 pagesIncome Tax (B.com Ii)iramanwarNo ratings yet

- Income Tax - SalaryDocument18 pagesIncome Tax - SalaryhanumanthaiahgowdaNo ratings yet

- AllowancesDocument7 pagesAllowancesBhavika ChughNo ratings yet

- Income Under The Head "Salaries": Shubhangi Gupta Roll No. 11 Financial Management Bhartiya Vidya BhavanDocument44 pagesIncome Under The Head "Salaries": Shubhangi Gupta Roll No. 11 Financial Management Bhartiya Vidya Bhavanhny0910No ratings yet

- 80.deductions or Allowances Allowed To Salaried EmployeeDocument11 pages80.deductions or Allowances Allowed To Salaried Employeekaweb87503No ratings yet

- Income Tax - SAlaryDocument24 pagesIncome Tax - SAlarymohamedshaheemkarumannilNo ratings yet

- Document 8Document30 pagesDocument 8anish ashokkumarNo ratings yet

- Victor Singh - CWCPS5027H - Q1 - Ay202223 - 16aDocument2 pagesVictor Singh - CWCPS5027H - Q1 - Ay202223 - 16agitu sorgtNo ratings yet

- Bill Track 02.03.2023Document14 pagesBill Track 02.03.2023Sridhar GandikotaNo ratings yet

- Taxation Malaysia Home Acca GlobalDocument12 pagesTaxation Malaysia Home Acca GlobalLee Yee Mei100% (1)

- WorksheetDocument1 pageWorksheetjoygie124apigoNo ratings yet

- Business Taxation AssignmentDocument7 pagesBusiness Taxation AssignmentThe Social KarkhanaNo ratings yet

- Cma Inter DT Idt Jun 24Document11 pagesCma Inter DT Idt Jun 24Pritam patelNo ratings yet

- 7 Seasons Front Office Daily Report: For The Day For The MonthDocument2 pages7 Seasons Front Office Daily Report: For The Day For The MonthRavinder NehraNo ratings yet

- B.L Jain & Sons: Particulars ParticularsDocument4 pagesB.L Jain & Sons: Particulars Particularsdeepak guptaNo ratings yet

- BC 103. Taxation IncomeDocument8 pagesBC 103. Taxation Incomezekekomatsu0No ratings yet

- Moshate KK (Pty) LTD TBDocument11 pagesMoshate KK (Pty) LTD TBNdamulelo SandaniNo ratings yet

- LHDNM Industry-Specific-Faqs Telecommunication Microsite BiDocument2 pagesLHDNM Industry-Specific-Faqs Telecommunication Microsite Bifareez nanNo ratings yet

- Transactions ReportDocument2 pagesTransactions ReportVinay KushwahaNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Ranjith R (RS)No ratings yet

- Tax Invoice: Gstin Drug Licence NoDocument1 pageTax Invoice: Gstin Drug Licence Nosatyam goyalNo ratings yet

- Tax 2 Finals ReviewerDocument6 pagesTax 2 Finals ReviewerSkylee SoNo ratings yet

- Haryana - Details of Wood IndustryDocument39 pagesHaryana - Details of Wood IndustryajitNo ratings yet

- Gopal HDFC-1Document3 pagesGopal HDFC-1Ashok RayNo ratings yet

- Income and Business TaxationDocument24 pagesIncome and Business TaxationFerdinand Carlos B. DadoNo ratings yet

- E Banking Project... P...Document69 pagesE Banking Project... P...Rohit Patil100% (1)

- McGraw Hill Connect Question Bank Assignment 1Document2 pagesMcGraw Hill Connect Question Bank Assignment 1Jayann Danielle MadrazoNo ratings yet

- Apr Jul BillDocument1 pageApr Jul BillShubham GuptaNo ratings yet

- GL Account Uploading Transaction EntryDocument4 pagesGL Account Uploading Transaction EntryshaiNo ratings yet

- Gaurav Salary Slip JulyDocument1 pageGaurav Salary Slip Julypramodchaudharyncc9upNo ratings yet

- Worksheet Exercise 2: 1. Write Down The Purchase Order Number On Space Provided Below: Purchase Order Number 4500019273Document14 pagesWorksheet Exercise 2: 1. Write Down The Purchase Order Number On Space Provided Below: Purchase Order Number 4500019273Andri Gunawan PurbaNo ratings yet

- FB Rec.Document1 pageFB Rec.tinaNo ratings yet

- Annual Premium Statement Prasanna2022Document2 pagesAnnual Premium Statement Prasanna2022PrasannaNo ratings yet

- CPA Exam ReviewDocument7 pagesCPA Exam ReviewJohn Allauigan MarayagNo ratings yet

- Bill of Supply For Electricity: Due Date: 16-07-2020Document1 pageBill of Supply For Electricity: Due Date: 16-07-2020Rãhûl SâïñíNo ratings yet

- Room QuotationDocument2 pagesRoom QuotationimporteveNo ratings yet