Impairing The Microsoft - Nokia Pairing

Impairing The Microsoft - Nokia Pairing

Download as pptx, pdf, or txt

You might also like

- EVA Analysis: Case: Vyaderm PharmaceuticalsDocument56 pagesEVA Analysis: Case: Vyaderm Pharmaceuticalsjk kumarNo ratings yet

- Working Capital Management: Case: ALAC InternationalDocument55 pagesWorking Capital Management: Case: ALAC Internationaljk kumarNo ratings yet

- 2012 Fuel Hedging at JetBlue AirwaysDocument181 pages2012 Fuel Hedging at JetBlue Airwaysjk kumar100% (3)

- Estimation of Cost of Capital: Case: The Boeing 7E7Document125 pagesEstimation of Cost of Capital: Case: The Boeing 7E7jk kumarNo ratings yet

- Group6 - Vyaderm PharmaceuticalsDocument7 pagesGroup6 - Vyaderm PharmaceuticalsVaishak AnilNo ratings yet

- Siemens Electric Motor Works (A) Process-Oriented CostingDocument12 pagesSiemens Electric Motor Works (A) Process-Oriented Costingjk kumar100% (1)

- Strategic Financial ManagementDocument8 pagesStrategic Financial Managementdivyakashyapbharat1No ratings yet

- Obscurity: Undesirability: P/E: Screening CriteriaDocument21 pagesObscurity: Undesirability: P/E: Screening Criteria/jncjdncjdnNo ratings yet

- CVP Analysis: Case: Aussie Pies (A)Document35 pagesCVP Analysis: Case: Aussie Pies (A)jk kumar100% (1)

- Convertible Securities: Case: Mogen IncDocument93 pagesConvertible Securities: Case: Mogen Incjk kumarNo ratings yet

- Syn 7 - Introduction To Debt Policy and ValueDocument11 pagesSyn 7 - Introduction To Debt Policy and Valuerudy anto100% (1)

- Fojtasek MemoDocument2 pagesFojtasek MemoRahul Rajappa0% (2)

- Facebook Inc.: The Initial Public Offerings (A) : Ruskin Lisa Crystal WeiDocument32 pagesFacebook Inc.: The Initial Public Offerings (A) : Ruskin Lisa Crystal WeiThái Hoàng NguyênNo ratings yet

- Mother - Please Speak Out: Income Statement For The Year Ended March 31, 2019 ($000s) Net Sales 100,000Document3 pagesMother - Please Speak Out: Income Statement For The Year Ended March 31, 2019 ($000s) Net Sales 100,000Jayash Kaushal0% (2)

- M&A Case Competition: - Roche Acquisition of GenentechDocument19 pagesM&A Case Competition: - Roche Acquisition of GenentechJuan Diego Vasquez BeraunNo ratings yet

- Michael McClintock Case1Document2 pagesMichael McClintock Case1Mike MCNo ratings yet

- 6 Polaroid Corporation 1996Document64 pages6 Polaroid Corporation 1996jk kumarNo ratings yet

- White Hills Children's MuseumDocument23 pagesWhite Hills Children's Museumjk kumarNo ratings yet

- Terrapower Harvard Business School Teaching Note: 5-815-050 Courseware 5-816-705Document6 pagesTerrapower Harvard Business School Teaching Note: 5-815-050 Courseware 5-816-705jk kumarNo ratings yet

- Bond Valuation: Case: Atlas InvestmentsDocument853 pagesBond Valuation: Case: Atlas Investmentsjk kumarNo ratings yet

- The Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of GilletteDocument366 pagesThe Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of Gillettejk kumarNo ratings yet

- Partnership AcctgDocument4 pagesPartnership Acctgcessbright100% (1)

- Test Bank For Analysis For Financial Management 10th Edition by Higgins PDFDocument18 pagesTest Bank For Analysis For Financial Management 10th Edition by Higgins PDFRandyNo ratings yet

- Advac 2 Prelims 1 - PALACIODocument4 pagesAdvac 2 Prelims 1 - PALACIOPinky DaisiesNo ratings yet

- FACD Project - Allergan-Pfizer DealDocument5 pagesFACD Project - Allergan-Pfizer DealSaksham SinhaNo ratings yet

- Koito Case Questions 2,3,4Document2 pagesKoito Case Questions 2,3,4Simo RajyNo ratings yet

- PGP MAJVCG 2019-20 S3 Unrelated Diversification PDFDocument22 pagesPGP MAJVCG 2019-20 S3 Unrelated Diversification PDFBschool caseNo ratings yet

- LoeaDocument21 pagesLoeahddankerNo ratings yet

- Case Analysis - Compania de Telefonos de ChileDocument4 pagesCase Analysis - Compania de Telefonos de ChileSubrata BasakNo ratings yet

- Bond Problem - Fixed Income ValuationDocument1 pageBond Problem - Fixed Income ValuationAbhishek Garg0% (2)

- FinValley 5.0 Case StudyDocument3 pagesFinValley 5.0 Case StudyBrennan BarnettNo ratings yet

- Canadian Pacific LTDDocument6 pagesCanadian Pacific LTDDeep Ray0% (3)

- Group 6 - Transforming Luxury Distribution in AsiaDocument5 pagesGroup 6 - Transforming Luxury Distribution in AsiaAnsh LakhmaniNo ratings yet

- Sealed Air Case Questions PDFDocument1 pageSealed Air Case Questions PDFKaran VoraNo ratings yet

- Marriott CorporationDocument8 pagesMarriott CorporationtarunNo ratings yet

- Case Analysis - Natureview FarmDocument11 pagesCase Analysis - Natureview Farmayush singla100% (1)

- Green Bonds - Itau BBA FrameworkDocument36 pagesGreen Bonds - Itau BBA FrameworkAndre d'AlvaNo ratings yet

- Barilla SpA Case Study 1Document4 pagesBarilla SpA Case Study 1Ankit KumarNo ratings yet

- Gillette - Indonesia TemplateDocument3 pagesGillette - Indonesia TemplateSona VardanyanNo ratings yet

- Why Is Soft Drink Industry So Profitable?: Barriers To EntryDocument3 pagesWhy Is Soft Drink Industry So Profitable?: Barriers To EntryVenkatesh BoddepalliNo ratings yet

- Caso Dupont - Keren MendesDocument17 pagesCaso Dupont - Keren MendesKeren NovaesNo ratings yet

- Case 32Document6 pagesCase 32patelnayan22No ratings yet

- LVMH - TiffanyDocument24 pagesLVMH - TiffanySagarika JindalNo ratings yet

- Krispy Kreme Doughnuts: "It Ain't Just The Doughnuts That Are Glazed!"Document9 pagesKrispy Kreme Doughnuts: "It Ain't Just The Doughnuts That Are Glazed!"dmaia12No ratings yet

- Case Bidding For Antamina: This Study Resource Was Shared ViaDocument6 pagesCase Bidding For Antamina: This Study Resource Was Shared ViaRishavLakraNo ratings yet

- Dupit Corporation: Representatives, More Commonly Known As Tech RepsDocument3 pagesDupit Corporation: Representatives, More Commonly Known As Tech RepsDeepak GuptaNo ratings yet

- Supporting Sheet - UV21001Document15 pagesSupporting Sheet - UV21001BikramdevPadhiNo ratings yet

- Sealed Air Corporation v1.0Document8 pagesSealed Air Corporation v1.0KshitishNo ratings yet

- Deluxe Corporation Case StudyDocument3 pagesDeluxe Corporation Case StudyHEM BANSALNo ratings yet

- Autumn 2011 - Midterm Assessment (25089)Document8 pagesAutumn 2011 - Midterm Assessment (25089)Marwa Nabil Shouman0% (1)

- 12oct2019 Netflix DTDocument9 pages12oct2019 Netflix DTDimitra TaslimNo ratings yet

- M&a Assignment - Syndicate C FINALDocument8 pagesM&a Assignment - Syndicate C FINALNikhil ReddyNo ratings yet

- General Mills' PaperDocument9 pagesGeneral Mills' PaperSarah McDermottNo ratings yet

- FS Mo IiiDocument67 pagesFS Mo Iiiarul kumarNo ratings yet

- LP Laboratories CaseDocument4 pagesLP Laboratories CaseAkash GuptaNo ratings yet

- Group30 Assignment 1Document7 pagesGroup30 Assignment 1Rajat GargNo ratings yet

- Section A - Group 2 - PRA 8Document5 pagesSection A - Group 2 - PRA 8sakshi agarwalNo ratings yet

- Citic Tower 2Document5 pagesCitic Tower 2Aakash Singh BJ22162No ratings yet

- Group 04-IndiaMart IPO Case AnalysisDocument23 pagesGroup 04-IndiaMart IPO Case AnalysisakshayNo ratings yet

- Iron Gate - InputDocument1 pageIron Gate - InputShshank0% (1)

- 7.1 Case Study Intro - Local Motors - Universidade de Illinois em Urbana-Champaign - CourseraDocument3 pages7.1 Case Study Intro - Local Motors - Universidade de Illinois em Urbana-Champaign - CourseraAlexandre SilvaNo ratings yet

- AppleDocument12 pagesAppleVeni GuptaNo ratings yet

- Samanvya BuildingDocument5 pagesSamanvya BuildingShiladitya Swarnakar0% (1)

- CaseDocument2 pagesCaseJenish RanaNo ratings yet

- Alpha CorporationDocument8 pagesAlpha CorporationBharat NarulaNo ratings yet

- Swati Anand - FRMcaseDocument5 pagesSwati Anand - FRMcaseBhavin MohiteNo ratings yet

- Questions On Mellon Financial and The Bank of New YorkDocument1 pageQuestions On Mellon Financial and The Bank of New YorkudayNo ratings yet

- Group 2Document54 pagesGroup 2Vikas Sharma100% (2)

- UVA-F-1264: Printicomm's Proposed Acquisition of Digitech: Negotiating Price and Form of PaymentDocument14 pagesUVA-F-1264: Printicomm's Proposed Acquisition of Digitech: Negotiating Price and Form of PaymentKumarNo ratings yet

- Case Submission On: Mellon Financial and The Bank of New YorkDocument3 pagesCase Submission On: Mellon Financial and The Bank of New Yorkneelakanta srikarNo ratings yet

- Ex 1Document3 pagesEx 1Adahyl Garcez60% (5)

- Atlantic Bundle Case Study - Group M2Document6 pagesAtlantic Bundle Case Study - Group M2ShivaniNo ratings yet

- WPP Group and Its AcquisitionsDocument76 pagesWPP Group and Its AcquisitionsKunal MehtaNo ratings yet

- Marriott - Spread SheetDocument13 pagesMarriott - Spread Sheetjk kumarNo ratings yet

- Classic Pen Company: Developing An ABC ModelDocument22 pagesClassic Pen Company: Developing An ABC Modeljk kumarNo ratings yet

- ABC - Ashokleyland MDP 2017Document41 pagesABC - Ashokleyland MDP 2017jk kumarNo ratings yet

- Case: The Boeing 7E7Document183 pagesCase: The Boeing 7E7jk kumarNo ratings yet

- Boeing 7E7 - UV6426-XLS-ENGDocument85 pagesBoeing 7E7 - UV6426-XLS-ENGjk kumarNo ratings yet

- 3 Ribbons AnDocument2 pages3 Ribbons Anjk kumarNo ratings yet

- BEA Associates - Enhanced Equity Index FundDocument16 pagesBEA Associates - Enhanced Equity Index Fundjk kumarNo ratings yet

- British Petroleum LimitedDocument593 pagesBritish Petroleum Limitedjk kumarNo ratings yet

- European Option: Basic (No Dividend) ModelDocument8 pagesEuropean Option: Basic (No Dividend) Modeljk kumarNo ratings yet

- Arvind's Net Worth: Exhibit 1: Before Tax Salary and Other Benefit Details of Mr. Arvind As On 30 May 2018Document2 pagesArvind's Net Worth: Exhibit 1: Before Tax Salary and Other Benefit Details of Mr. Arvind As On 30 May 2018jk kumarNo ratings yet

- 2012 Fuel Hedging at JetBlue Airways U - V6685-XLS-ENG-3Document123 pages2012 Fuel Hedging at JetBlue Airways U - V6685-XLS-ENG-3jk kumar100% (1)

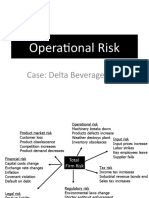

- Delta Beverage Group, Inc. - FINALDocument23 pagesDelta Beverage Group, Inc. - FINALjk kumarNo ratings yet

- Joint Venture: Case: Hero Honda Motors (India) LTD.: Is It Honda That Made It A Hero?Document37 pagesJoint Venture: Case: Hero Honda Motors (India) LTD.: Is It Honda That Made It A Hero?jk kumarNo ratings yet

- Creative Accounting: A Literature Review: Brijesh YadavDocument13 pagesCreative Accounting: A Literature Review: Brijesh YadavAnonymous ckTjn7RCq8No ratings yet

- Module 1 - Business Combination (IFRS 3)Document15 pagesModule 1 - Business Combination (IFRS 3)MILBERT DE GRACIANo ratings yet

- 12 Accountancy Sp02Document15 pages12 Accountancy Sp02Rahul PareekNo ratings yet

- Classroom Exercises On Business Combinations and Consolidation - Date of AcquisitionDocument6 pagesClassroom Exercises On Business Combinations and Consolidation - Date of AcquisitionalyssaNo ratings yet

- Sec 17q June 2021Document40 pagesSec 17q June 2021Kendrick UyNo ratings yet

- Balance Sheet BasicsDocument24 pagesBalance Sheet Basicsnavya sreeNo ratings yet

- Tax RemediesDocument19 pagesTax RemediesRocky MarcianoNo ratings yet

- Fa - End TermDocument21 pagesFa - End Termmadhurialamuri100% (3)

- Corp Ass 1Document18 pagesCorp Ass 1samuel debebeNo ratings yet

- What Is An AssetDocument6 pagesWhat Is An AssetrimpyNo ratings yet

- Accounting Compress PDFDocument9 pagesAccounting Compress PDFJade jade jadeNo ratings yet

- Fair Value of Net AssetsDocument8 pagesFair Value of Net AssetsGanbilegBatnasanNo ratings yet

- Admission Test No. 2Document5 pagesAdmission Test No. 2Mitesh Sethi0% (1)

- Business ValuationsDocument29 pagesBusiness ValuationsRishabh singh100% (1)

- Cambridge Ordinary LevelDocument12 pagesCambridge Ordinary LevelPei TingNo ratings yet

- P18 CFR CMA Final - PaperDocument6 pagesP18 CFR CMA Final - PaperhritikdabhadeNo ratings yet

- Strategic Planning Excel TemplateDocument98 pagesStrategic Planning Excel TemplateNeil Nadua100% (1)

- Team PRTC Afar-Finpb - 5.21Document16 pagesTeam PRTC Afar-Finpb - 5.21Nanananana100% (2)

- Intangible Assets and Its TypesDocument3 pagesIntangible Assets and Its TypesKhaled ShabanNo ratings yet

- TA.2011 - NCA Held For SaleDocument42 pagesTA.2011 - NCA Held For SaleJay-L TanNo ratings yet

- Tampoa Ae211 Unit 1 Assessment ProblemsDocument12 pagesTampoa Ae211 Unit 1 Assessment ProblemsJahna Kay TampoaNo ratings yet

- Chapter Six Consolidation of Financial Statements Under Purchase AccountingDocument15 pagesChapter Six Consolidation of Financial Statements Under Purchase AccountingMelody Lisa100% (1)

- Solution Chapter 17Document87 pagesSolution Chapter 17Sy Him88% (8)

- Internal Reconstruction NotesDocument16 pagesInternal Reconstruction NotesAkash Mehta100% (1)

- Intercorporate Acquisitions and Investments in Other EntitiesDocument31 pagesIntercorporate Acquisitions and Investments in Other EntitiesSayed Farrukh AhmedNo ratings yet

- Worksheet-10 Retirement of A PartnerDocument12 pagesWorksheet-10 Retirement of A Partnerchanikran404No ratings yet

- Fair Value Accounting, Financial Economics and The Transformation of ReliabilityDocument15 pagesFair Value Accounting, Financial Economics and The Transformation of ReliabilityThe SalsaNo ratings yet