0% found this document useful (0 votes)

72 viewsLeverage and Optimal Capital Structure

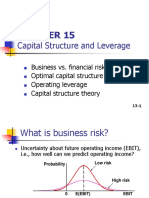

This document discusses leverage and optimal capital structure. It defines business risk as uncertainty about future operating income, and notes that business risk is unaffected by financing decisions. Operating leverage is the use of fixed costs, which increases business risk since fixed costs do not decline with sales. Financial leverage refers to the use of debt financing. While business risk depends on operating factors, financial risk depends on the capital structure and introduces additional risk for equity holders through interest expenses. The document provides an example comparing unleveraged and leveraged firms to illustrate how financial leverage increases expected return on equity but also increases risk. It concludes that an optimal capital structure balances higher expected returns against higher risk.

Uploaded by

Invisible CionCopyright

© © All Rights Reserved

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

72 viewsLeverage and Optimal Capital Structure

This document discusses leverage and optimal capital structure. It defines business risk as uncertainty about future operating income, and notes that business risk is unaffected by financing decisions. Operating leverage is the use of fixed costs, which increases business risk since fixed costs do not decline with sales. Financial leverage refers to the use of debt financing. While business risk depends on operating factors, financial risk depends on the capital structure and introduces additional risk for equity holders through interest expenses. The document provides an example comparing unleveraged and leveraged firms to illustrate how financial leverage increases expected return on equity but also increases risk. It concludes that an optimal capital structure balances higher expected returns against higher risk.

Uploaded by

Invisible CionCopyright

© © All Rights Reserved

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

/ 42

You might also like

- No ratings yetCHAPTER 16 Capital Structure Decisions the Basics cvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvvv62 pages