0% found this document useful (0 votes)

58 views35 pagesTypes of Capital Investment Decisions

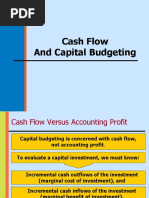

Capital budgeting is a critical process for analyzing long-term investment opportunities and making decisions that impact a firm's profitability and future direction. The capital budgeting process involves generating project proposals, estimating cash flows, evaluating and selecting projects, and implementing and reviewing them. Effective capital budgeting can enhance a firm's stock prices and ultimately maximize shareholder wealth.

Uploaded by

Hasnain BhuttoCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

58 views35 pagesTypes of Capital Investment Decisions

Capital budgeting is a critical process for analyzing long-term investment opportunities and making decisions that impact a firm's profitability and future direction. The capital budgeting process involves generating project proposals, estimating cash flows, evaluating and selecting projects, and implementing and reviewing them. Effective capital budgeting can enhance a firm's stock prices and ultimately maximize shareholder wealth.

Uploaded by

Hasnain BhuttoCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd