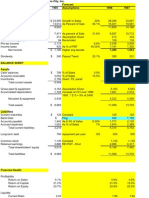

Dell's Working Capital

Dell's Working Capital

Download as ppt, pdf, or txt

You might also like

- Nike Case AnalysisDocument9 pagesNike Case AnalysisUyen Thao Dang96% (54)

- Fonderia Di Torino ExcelDocument10 pagesFonderia Di Torino Excelpeachrose12100% (1)

- Group 10 - Case 1 - Gainesboro Machine Tools CorporationDocument4 pagesGroup 10 - Case 1 - Gainesboro Machine Tools CorporationYubaraj Adhikari100% (1)

- List of Case Questions: Case #5: Fonderia Di Torino S.P.A Questions For Case PreparationDocument4 pagesList of Case Questions: Case #5: Fonderia Di Torino S.P.A Questions For Case Preparationdd100% (2)

- Answers - Cost of Capital Wallmart Inc.Document11 pagesAnswers - Cost of Capital Wallmart Inc.Arslan HafeezNo ratings yet

- Nike Case Final Group 4Document15 pagesNike Case Final Group 4Monika Maheshwari100% (1)

- Marriott ExcelDocument2 pagesMarriott ExcelRobert Sunho LeeNo ratings yet

- Dell's Working Capital - Case Analysis - G05Document2 pagesDell's Working Capital - Case Analysis - G05Srikanth Kumar Konduri100% (11)

- Dell Working CapitalDocument6 pagesDell Working CapitalNavi Spl50% (2)

- Analysis of DELLDocument12 pagesAnalysis of DELLMuhammad Afzal100% (1)

- Case 7 - Dell's Working Capital (Syndicate 3) PDFDocument14 pagesCase 7 - Dell's Working Capital (Syndicate 3) PDFfullataniaNo ratings yet

- Hill Country Snack Foods Co - UDocument4 pagesHill Country Snack Foods Co - Unipun9143No ratings yet

- Tire City AnalysisDocument1 pageTire City AnalysisNikhil Kangutkar80% (10)

- Fonderia Di Torino Case Study GroupDocument15 pagesFonderia Di Torino Case Study GroupFarhan SoepraptoNo ratings yet

- Midland Energy Resources Inc SolutionDocument2 pagesMidland Energy Resources Inc SolutionAashna MehtaNo ratings yet

- Flash Memory IncDocument7 pagesFlash Memory IncAbhinandan SinghNo ratings yet

- Assignment For MCIDocument3 pagesAssignment For MCIkashanr82100% (1)

- Nike, Inc Cost of Capital Case StudyDocument19 pagesNike, Inc Cost of Capital Case StudyChristine Son60% (5)

- Investment Analysis and Tri Star Lockheed - FULL FINALDocument8 pagesInvestment Analysis and Tri Star Lockheed - FULL FINALCheytan Thakar100% (3)

- Midland Energy Resources FinalDocument5 pagesMidland Energy Resources FinalpradeepNo ratings yet

- Nike CaseDocument7 pagesNike CaseNindy Darista100% (1)

- New Heritage Doll CompanyDocument5 pagesNew Heritage Doll CompanyRahul LalwaniNo ratings yet

- CONTEC8000S英文正文140430Document60 pagesCONTEC8000S英文正文140430Lucy Fernanda MillanNo ratings yet

- Dell Working Capital SolutionDocument10 pagesDell Working Capital SolutionIIMnotes100% (1)

- Dell's Working Capital SolutionDocument22 pagesDell's Working Capital SolutionShaikh Saifullah KhalidNo ratings yet

- Dell Working CapitalDocument3 pagesDell Working CapitalShashank Agarwal89% (9)

- Dell's Working Capital: Case BriefDocument6 pagesDell's Working Capital: Case BriefTanya Ahuja100% (1)

- Dell Case StudyDocument4 pagesDell Case StudyDamian Arias100% (3)

- Dell's Working Capital v0.2Document6 pagesDell's Working Capital v0.2MrDorakonNo ratings yet

- Dell Working CapitalDocument9 pagesDell Working CapitalAdiansyach PatonangiNo ratings yet

- Dell Working Capital CaseDocument2 pagesDell Working Capital CaseIshan Rishabh Kansal100% (2)

- Case Study Debt Policy Ust IncDocument10 pagesCase Study Debt Policy Ust IncIrfan MohdNo ratings yet

- Hill Country Snack Foods Co - UDocument4 pagesHill Country Snack Foods Co - Unipun9143No ratings yet

- Nike INCDocument7 pagesNike INCUpendra Ks50% (2)

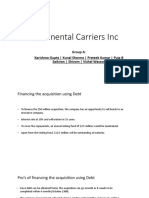

- Continental CarriersDocument10 pagesContinental Carriersnipun9143No ratings yet

- Debt Policy at UST IncDocument5 pagesDebt Policy at UST Incggrillo73No ratings yet

- Final Presentasi MCI by Grup 5Document23 pagesFinal Presentasi MCI by Grup 5Prayogi Purnapandhega0% (1)

- Midland CaseDocument5 pagesMidland CaseJessica Bill100% (3)

- Accounting For Frequent Fliers CaseDocument15 pagesAccounting For Frequent Fliers CaseGlenPalmer50% (2)

- Fonderia DI TorinoDocument19 pagesFonderia DI TorinoA100% (3)

- Marriott CorporationDocument9 pagesMarriott CorporationMichelle Rodríguez100% (1)

- Nike, Inc. - Cost of CapitalDocument9 pagesNike, Inc. - Cost of CapitalPutriNo ratings yet

- Analysis Slides-WACC NikeDocument25 pagesAnalysis Slides-WACC NikePei Chin100% (3)

- Midland Energy Resources (Final)Document4 pagesMidland Energy Resources (Final)satherbd21100% (3)

- Midland FinalDocument8 pagesMidland Finalkasboo6No ratings yet

- Midland Energy Resources Case Study: FINS3625-Applied Corporate FinanceDocument11 pagesMidland Energy Resources Case Study: FINS3625-Applied Corporate FinanceCourse Hero100% (1)

- Fonderia Di Torino (Final)Document4 pagesFonderia Di Torino (Final)Tracye Taylor100% (2)

- Investment Detective CaseDocument3 pagesInvestment Detective CaseWidyawan Widarto 闘志50% (2)

- UST IncDocument16 pagesUST IncNur 'AtiqahNo ratings yet

- Midland Energy A1Document30 pagesMidland Energy A1CarsonNo ratings yet

- Dell S Working Capital 1Document20 pagesDell S Working Capital 1deni1456No ratings yet

- Dells Working Capital1Document20 pagesDells Working Capital1Saurabh PratihastaNo ratings yet

- Dell's Working Capital: Click To Edit Master Subtitle Style B.B.Chakrabarti Professor of Finance IIM CalcuttaDocument20 pagesDell's Working Capital: Click To Edit Master Subtitle Style B.B.Chakrabarti Professor of Finance IIM CalcuttaOmkar DeshpandeNo ratings yet

- CASE 17: Dell's Working Capital: Financial Management AssignmentDocument8 pagesCASE 17: Dell's Working Capital: Financial Management AssignmentAamir KhanNo ratings yet

- Dell's Working Capital - FinalDocument7 pagesDell's Working Capital - FinalSubrata BasakNo ratings yet

- Dell's Working Capital - SG7Document14 pagesDell's Working Capital - SG7rudy antoNo ratings yet

- Dell Computer: Working Capital Management Financing GrowthDocument15 pagesDell Computer: Working Capital Management Financing GrowthSudipta ChatterjeeNo ratings yet

- Dell's Working Capital Syndicate 4Document16 pagesDell's Working Capital Syndicate 4agnieimaniawildanNo ratings yet

- Dell Working Capital Management Write UpDocument1 pageDell Working Capital Management Write UpSalil AggarwalNo ratings yet

- Dell's Working Capital: Presented byDocument11 pagesDell's Working Capital: Presented byRahul NeelakantanNo ratings yet

- Dell Computer CorporationDocument19 pagesDell Computer Corporationkartiki_thorave6616No ratings yet

- Paulo Coelho - Veronika Decides To DieDocument11 pagesPaulo Coelho - Veronika Decides To Dieapi-26751591No ratings yet

- Srimad Bhagavad Gita (Hindi, Sanskrit, English)Document119 pagesSrimad Bhagavad Gita (Hindi, Sanskrit, English)nss1234567890No ratings yet

- Questions and Answers 1957-1958 by Holy MotherDocument452 pagesQuestions and Answers 1957-1958 by Holy Motherapi-3719687No ratings yet

- More Answers of The Mother by Holy MotherDocument421 pagesMore Answers of The Mother by Holy Motherapi-3719687No ratings yet

- Upanishad PDFDocument320 pagesUpanishad PDFSaamratAshokaNo ratings yet

- On Thoughts and Aphorisms by Holy MotherDocument388 pagesOn Thoughts and Aphorisms by Holy Motherapi-3719687No ratings yet

- The Renaissance in India by Shri AurobindoDocument484 pagesThe Renaissance in India by Shri Aurobindoapi-3719687No ratings yet

- Questions and Answers 1955 by Holy MotherDocument448 pagesQuestions and Answers 1955 by Holy Motherapi-3719687No ratings yet

- Karmayogin by Shri AurobindoDocument488 pagesKarmayogin by Shri Aurobindoapi-3719687No ratings yet

- Ken A and Other Up Ani ShadsDocument459 pagesKen A and Other Up Ani ShadsdevendrameherNo ratings yet

- Words of The Mother by Holy MotherDocument386 pagesWords of The Mother by Holy Motherapi-3719687No ratings yet

- Questions and Answers 1950-1951 by Holy MotherDocument432 pagesQuestions and Answers 1950-1951 by Holy Motherapi-3719687No ratings yet

- 08 Questions and Answers 1956Document430 pages08 Questions and Answers 1956Robert WilliamsNo ratings yet

- Isha Upanishad TamilDocument607 pagesIsha Upanishad Tamilram_soft200383% (6)

- Mirra Alfassa - Questions and Answers - Volume 4 - 1954 (Sri Aurobindo Ashram Trust)Document484 pagesMirra Alfassa - Questions and Answers - Volume 4 - 1954 (Sri Aurobindo Ashram Trust)giovannagarritanoNo ratings yet

- Essays Divine and Human - Sri Aurobindo PDFDocument529 pagesEssays Divine and Human - Sri Aurobindo PDFjj_dokovNo ratings yet

- Prayers and Meditations by Holy MotherDocument403 pagesPrayers and Meditations by Holy Motherapi-3719687No ratings yet

- 03 04CollectedPlaysAndStoriesDocument1,018 pages03 04CollectedPlaysAndStoriesMonica MonasterioNo ratings yet

- Enta MatramunaDocument3 pagesEnta Matramunaapi-3719687100% (1)

- Kandu KandumDocument2 pagesKandu Kandumapi-3719687No ratings yet

- 361robin CasDocument2 pages361robin Casapi-3719687No ratings yet

- World Watch CaseDocument31 pagesWorld Watch Caseapi-3719687100% (1)

- Band em at AramDocument1,206 pagesBand em at AramdevendrameherNo ratings yet

- 01EarlyCulturalWritings PDFDocument808 pages01EarlyCulturalWritings PDFDSSidgiddiNo ratings yet

- World Watch QuestionsDocument6 pagesWorld Watch Questionsapi-3719687No ratings yet

- COMPETNDocument23 pagesCOMPETNapi-3719687No ratings yet

- Ulaganath Madan-FinalDocument9 pagesUlaganath Madan-Finalapi-3719687100% (4)

- Strategy & HR Linkage Basics of HRM - Dec 2006Document67 pagesStrategy & HR Linkage Basics of HRM - Dec 2006api-3719687No ratings yet

- Blackman-Dodds - Day 2Document4 pagesBlackman-Dodds - Day 2api-3719687No ratings yet

- South West Airlines-Day 2Document7 pagesSouth West Airlines-Day 2api-3719687100% (2)

- EvsDocument18 pagesEvsaaaassNo ratings yet

- DC Current Injection Into The Network From PV Grid InvertersDocument5 pagesDC Current Injection Into The Network From PV Grid Inverterschristian brasselNo ratings yet

- British Steel V Cleveland Bridge (1981) 24 BLR 94, Robert Goff J.Document1 pageBritish Steel V Cleveland Bridge (1981) 24 BLR 94, Robert Goff J.Eslam AshourNo ratings yet

- RetailCo 2 Case AnalysisDocument5 pagesRetailCo 2 Case AnalysisDino De LeonNo ratings yet

- Electrical QBDocument27 pagesElectrical QBLakshmiVishwanathanNo ratings yet

- Lloyd Industries Inc.: Installation InstructionsDocument6 pagesLloyd Industries Inc.: Installation InstructionsDongNo ratings yet

- Thieves of State Why Corruptio Sarah Chayes PDFDocument136 pagesThieves of State Why Corruptio Sarah Chayes PDFEngr Siraj RahmdilNo ratings yet

- Defradar - GDPR Competence Development QuestionnaireDocument2 pagesDefradar - GDPR Competence Development QuestionnaireJakobović DomagojNo ratings yet

- Peta Persebaran Asf Di Indonesia: 1. Medan 2. Lampung 3. Pontianak 4. Jawa 5. Bali 6. NTT 7. Manado 8. PapuaDocument3 pagesPeta Persebaran Asf Di Indonesia: 1. Medan 2. Lampung 3. Pontianak 4. Jawa 5. Bali 6. NTT 7. Manado 8. PapuaCt ZahraNo ratings yet

- Benq Corporation: Hsink Hsink Hsink HsinkDocument3 pagesBenq Corporation: Hsink Hsink Hsink HsinkRUSTAM YUWONONo ratings yet

- Comprehensive Agrarian Reform Program (CARP)Document29 pagesComprehensive Agrarian Reform Program (CARP)Robyne UyNo ratings yet

- Geared DC Instrument Motor 1308 SeriesDocument1 pageGeared DC Instrument Motor 1308 SeriesIdehen KelvinNo ratings yet

- Khan 2013Document7 pagesKhan 2013Juan VillanuevaNo ratings yet

- Short Introduction To The Sony Vegas Movie StudioDocument15 pagesShort Introduction To The Sony Vegas Movie StudioAttila NagyNo ratings yet

- Harry Potter - Book of Evil-Machine Translated 0-20Document491 pagesHarry Potter - Book of Evil-Machine Translated 0-20zerosamaNo ratings yet

- Stusb 4761Document29 pagesStusb 4761Richard XuNo ratings yet

- Primary Mental AbilitiesDocument10 pagesPrimary Mental AbilitiesLhyda ElibadoNo ratings yet

- Talend Open Studio For Big Data: User GuideDocument592 pagesTalend Open Studio For Big Data: User GuideNavaneethNo ratings yet

- KR-301 ControlDocument16 pagesKR-301 ControlSreekanthMylavarapuNo ratings yet

- Green Bites 4Document31 pagesGreen Bites 4dielsebastian04No ratings yet

- Pentax CST-225 ManualDocument175 pagesPentax CST-225 ManualCarlos Trenary100% (1)

- Automatic Ticket Assignment AIML Online Capstone Group 6Document21 pagesAutomatic Ticket Assignment AIML Online Capstone Group 6Richa AnandNo ratings yet

- SEACUT DeliverablesDocument2 pagesSEACUT DeliverablesAr-Reb AquinoNo ratings yet

- Practicum LPDocument8 pagesPracticum LPShah Rul MalikNo ratings yet

- All Questions Are CompulsoryDocument2 pagesAll Questions Are CompulsoryRisha MalNo ratings yet

- Maxus V90 Owner's ManualDocument255 pagesMaxus V90 Owner's ManualLuis Ibaceta V.No ratings yet

- Wholesale Food Warehouse Risk Control Plan WorkbookDocument74 pagesWholesale Food Warehouse Risk Control Plan Workbooknicoleta_grosu87No ratings yet

- Charles DarwinDocument2 pagesCharles DarwinAlison McCartneyNo ratings yet

- (已压缩)XCMG PeaCock Forklift (6 7t)Document6 pages(已压缩)XCMG PeaCock Forklift (6 7t)chenqiushuo99No ratings yet