0% found this document useful (0 votes)

43 viewsLecture 3-Linear Programming

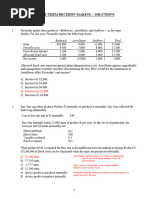

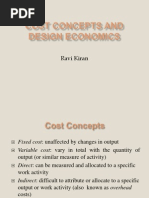

This document discusses linear programming and its applications. It begins with an introduction to linear programming and its key assumptions. It then outlines the steps to formulate a linear programming problem: [1] determining the objective variable and function, [2] constructing constraint statements, [3] solving graphically, [4] establishing the feasible region, and [5] determining the optimal solution. It provides two examples - one involving production planning for two products with constrained resources, and another involving production planning for boxes and tins. It concludes with discussions on shadow prices, short-term decision making, make-or-buy decisions, and product line closure decisions.

Uploaded by

admiremukureCopyright

© © All Rights Reserved

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

43 viewsLecture 3-Linear Programming

This document discusses linear programming and its applications. It begins with an introduction to linear programming and its key assumptions. It then outlines the steps to formulate a linear programming problem: [1] determining the objective variable and function, [2] constructing constraint statements, [3] solving graphically, [4] establishing the feasible region, and [5] determining the optimal solution. It provides two examples - one involving production planning for two products with constrained resources, and another involving production planning for boxes and tins. It concludes with discussions on shadow prices, short-term decision making, make-or-buy decisions, and product line closure decisions.

Uploaded by

admiremukureCopyright

© © All Rights Reserved

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

/ 40