Abstract

We aim at analyzing in terms of a.s. convergence and weak rate the performances of the Multilevel Monte Carlo estimator (MLMC) introduced in [7] and of its weighted version, the Multilevel Richardson–Romberg estimator (ML2R), introduced in [12].

These two estimators permit to compute a very accurate approximation of

1 Introduction

In recent years, there has been an increasing interest in Multilevel Monte Carlo approach which delivers remarkable improvements in computational complexity in comparison with standard Monte Carlo in biased framework. We refer the reader to [8] for a broad outline of the ideas behind the Multilevel Monte Carlo method and various recent generalizations and extensions.

In this paper we establish a Strong Law of Large Numbers and Central Limit Theorem for two kinds of multilevel estimator,

Multilevel Monte Carlo estimator (MLMC) introduced by Giles in [7]

and the Multilevel Richardson–Romberg (weighted) estimator introduced in [12].

We consider a rather general and in some way abstract framework which will allow us to state these results

whatever the strong rate parameter is (usually denoted by β).

To be more precise, we will deal with the versions of these estimators designed to achieve a root mean squared error (RMSE) ε and establish these results as

Let

where

A standard Multilevel Monte Carlo (MLMC) estimator, as introduced by Giles in [7], reads

with

A Multilevel Richardson–Romberg (ML2R) estimator, as introduced in [12], is a weighted version of (1) which reads

with

with the convention

The calibration of the parameters is the result, a root

This calibration has been done in [12] for both estimators MLMC and ML2R under the following assumptions on the sequence

The second one, called strong approximation error assumption, states

Note that the strong error assumption can be sometimes replaced by the sharper

From now on, we set

where the finite real constant

where the finite real constant

The aim of this paper is to prove a Strong Law of Large Numbers (SLLN) and a Central Limit Theorem (CLT) for both estimators MLMC and ML2R calibrated using these optimal parameters. First notice that as these parameters have been computed under the constraint

so that

We will weaken the assumption on the sequence

with

In particular, we will prove that

where

The paper is organized as follows. In Section 2 we briefly recall the technical background for Multilevel Monte Carlo estimators. In Section 3 we stable our main results: a Strong Law of Large Numbers and a Central Limit Theorem in a quite general framework. Section 4 is devoted to the analysis of the asymptotic behavior of the optimal parameters, to the study of the weights of the ML2R estimator and to the bias of the estimators and its robustness. These are auxiliary results that we need for the proof of the main theorems, which we detail in Section 5. In Section 6 we apply these results first to the discretization schemes of Brownian diffusions, where we retrieve recent results by Ben Alaya and Kebaier in [2], and secondly to Nested Monte Carlo.

Notations.

Let

For every

If

We denote by

2 Brief background on MLMC and ML2R estimators

We follow [12] and recall briefly the construction of the optimal parameters derived from the optimization problem (3). The first step is a stratification procedure allowing us to establish the optimal allocation policy

a Multilevel estimator MLMC (1) or ML2R (2) writes

where

Given

using the Schwarz’s inequality (see [12, Theorem 3.6] for a detailed proof). The strong error assumption (${\mathrm{SE}_{\beta}}$) allows us to upper bound

The second step is to select

with

The depth parameter

We report in Tables 1 and 2 the ML2R and MLMC

values for

and

Notice that

Optimal parameters for the ML2R estimator.

Optimal parameters for the MLMC estimator.

In what follows, we will shorter these notations by setting

with

for ML2R and

with

for MLMC.

3 Main results

The asymptotic behavior, as ε goes to 0, of the parameters given in Tables 1 and 2 will be exposed in Section 4. We proceed here to the analysis of the asymptotic behavior of the estimator

3.1 Strong Law of Large Numbers

We will first prove a Strong Law of Large Numbers, namely

Theorem 3.1 (Strong Law of Large Numbers)

Let

Then, for every sequence of positive real numbers

3.2 Central Limit Theorems

A necessary condition for a Central Limit Theorem to hold will be that the ratio between the variance of the estimator and ε converges as

A necessary condition to obtain a CLT is to assume that

3.2.1 Case β > 1

In this case, note that following (${\mathrm{SE}_{\beta}}$) we have

Theorem 3.2 (Central Limit Theorem, β > 1

Assume (${\mathrm{SE}_{\beta}}$) for

with

Then the following statements hold.

ML2R estimator: Assume ((${\mathrm{WE}_{\alpha,\bar{R}}}$)) for all

(12)MLMC estimator: Assume ((${\mathrm{WE}_{\alpha,\bar{R}}}$)) for

Note that the variance of the first term

3.2.2 Case β ∈ ( 0 , 1 ]

In this case, we make the additional sharper assumption that

so that

We conclude that

Theorem 3.3 (Central Limit Theorem, 0 < β ⩽ 1

Assume (${\mathrm{SE}_{\beta}}$) for

Then the following statements hold.

ML2R estimator: Assume ((${\mathrm{WE}_{\alpha,\bar{R}}}$)) for all

(14)MLMC estimator: Assume ((${\mathrm{WE}_{\alpha,\bar{R}}}$)) for

We will see in the proof that the asymptotic variance corresponds to the variance associated to the correcting levels.

3.3 Practitioner’s corner

In the proof of Theorems 3.2 and 3.3 we will obtain the more precise expansion

where

When

When

For ML2R, owing to the expression of

For MLMC, we get

Impact of the weights 𝐖 j R j = 1 , … , R

When

4 Auxiliary results

This section contains some useful results for the proof of the Strong Law of Large Numbers and of the Central Limit Theorem. More in detail, we investigate the asymptotic behavior as

4.1 Asymptotic of the bias parameter and of the depth

An important property of MLMC and ML2R estimators is that

and we recall that this is the optimized bias found in [12] at R fixed.

Since the value of

where

We notice that

The optimal choice for the bias is the projection of

When we replace

Let us analyze the denominator

Since

which yields

For MLMC we may follow the same reasoning starting from

There exists

In what follows, we will always assume that

As

4.2 Asymptotic of the bias and robustness

As part of a Central Limit Theorem, we will be faced to the quantity

is the bias of the estimator.

This leads us to analyze carefully its asymptotic behavior as

The bias of Multilevel estimators is dramatically reduced compared to the Crude Monte Carlo, more precisely the following proposition is proved in [12]:

The following statements hold.

MLMC: Assume ((${\mathrm{WE}_{\alpha,\bar{R}}}$)) with

with

ML2R: Assume ((${\mathrm{WE}_{\alpha,\bar{R}}}$)) for all

where

We notice that the ML2R estimator requires and takes full advantage of a higher order of the expansion of the bias error

(${\mathrm{WE}_{\alpha,\bar{R}}}$),

whereas the MLMC estimator only needs a first order expansion.

As the computations were made under the constraint

and, for MLMC,

We set

For ML2R estimators, if

and

hence

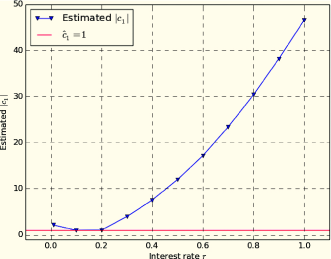

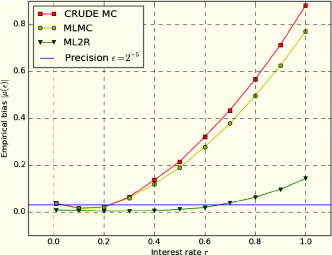

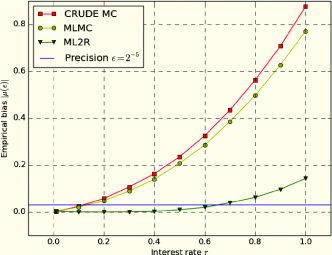

In Figures a and b we show the values of

compared to the value plugged in the simulations

In Figures a and b

we show the absolute value of the empirical bias for different values of r.

In the simulations, we fixed

Estimated

Euler scheme (

Milstein scheme (

Empirical bias

Euler scheme (

Milstein scheme (

4.3 Properties of the weights of the ML2R estimator

One significant difficulty in the proof of the Central Limit Theorem that we stated in Theorems 3.2 and 3.3,

is to deal with the weights

where the weights

Notice that

where

with the convention

As a consequence,

We will make an extensive use of the following properties, which are proved in Appendix A.

Let

The weights

(19)For every

Let

4.4 Asymptotic of the allocation policy and of the size

Let us analyze the allocation policy

the condition

Owing to Lemma 4.3 (c) with

Moreover, for all

If we set

The asymptotic of the estimator size

We have

Case

Case

where the constant

and

We notice that for

and the factor

Proof.

ML2R: The estimator size N reads

We notice that

MLMC: The result follows directly from the convergence of the series

as desired. ∎

5 Proofs

We will use the notations

where we set

These notations hold for both ML2R and MLMC estimators, where we set

where the bias

5.1 Proof of Strong Law of Large Numbers

The proof of the Strong Law of Large Numbers is a consequence of the following proposition.

Let

Proof.

ML2R: We first give the proof of (23) for the ML2R estimator.

As a first step we show that, for all

By Minkowski’s inequality,

Applying again Minkowski’s inequality, the

As

It follows from the expression of

Then, using that

Owing to Lemma 4.5, up to reducing

Moreover,

Then

with

Hence (23) holds with

MLMC: The proof for the MLMC estimator follows the same steps, by replacing

The Strong Law of Large Numbers follows as a consequence of Proposition 5.1.

Proof of Theorem 3.1.

Owing to the decomposition (22), equation (10) amounts to proving

As

To establish the a.s. convergence of

Hence, by Beppo–Levi’s Theorem,

5.2 Proof of the Central Limit Theorem

This subsection is devoted to the proof of Theorems 3.2 and 3.3.

In order to satisfy a Lindeberg condition, we will need the assumption

Since

One criterion to verify the

The following statements hold.

If there exists a

If there exists a random variable

The family

Now we are in a position to prove the Central Limit Theorem, in both cases

Proof of Theorems 3.2 and 3.3.

Owing to the decomposition (22) (with

where

ML2R: Formulas (12) and (14) amount to proving, as

and

with

In particular, since

which proves (26).

We will use Lindeberg’s Theorem for triangular arrays of martingale increments (see [10, Corollary 3.1, p. 58]) to establish (27). The random variables

Noticing that

The conclusion will follow from

and

Owing to the definition of

Case

and owing to the limit in Lemma 4.3 (d) with

Hence the convergence of the variance (28) holds for Theorem 3.2.

Case

We notice that

if

if

For (29), it follows from the expression of

Owing to the definition of

We conclude by showing that

Owing to the expression of

Moreover, using Lemma 4.5, up to another reduction of

Then (29) is proved and so is the first condition of Lindeberg’s Theorem.

For the second condition of Lindeberg’s Theorem we need to prove that, for every

Since the

We set

where we set

as

and the second condition of Lindeberg’s Theorem is proved.

MLMC:

The proofs are quite the same as for ML2R, up to the constant

We replace

which goes to 0, owing to the strict inequality assumption

6 Applications

6.1 Diffusions

In this subsection we retrieve a recent result by Kebaier and Ben Alaya (see [2]) obtained for MLMC estimators

and we extend it to the ML2R estimators and to the use of path-dependent functionals. Let

where

We know that

with

where

It is classical background that, under the above assumptions on

For the weak error expansion the existing results are less general. Let us recall as an illustration the celebrated Talay–Tubaro’s and Bally–Talay’s weak error expansions for marginal functionals of Brownian diffusions, i.e. functionals of the form

The following statements hold.

Regular setting (Talay–Tubaro [13]): If b and σ are infinitely differentiable with bounded partial derivatives and if

(33)where the coefficients

(Hypo-)Elliptic setting (Bally–Talay [1]): If b and σ are infinitely differentiable with bounded partial derivatives and if σ is uniformly elliptic in the sense that

or more generally if

For more general path-dependent functionals, no such result exists in general. For various classes of specified functionals depending on the running maximum or mean, some exit stopping time, first order weak expansions in

In this subsection we consider

We assume the weak error expansion (${\mathrm{WE}_{\alpha,\bar{R}}}$). We prove now that both estimators ML2R (2) and MLMC (1) satisfy a Strong Law of Large Numbers and a Central Limit Theorem when ε tends to 0.

Let

If

If

As a consequence, both ML2R and MLMC estimators satisfy Theorem 3.3 (case

Proof.

First, note that if F is a Lipschitz continuous functional, with Lipschitz coefficient

then

Assume now that

At this stage it remains to prove (34). The key is [2, Theorem 3], where it is proved that

where

We recall the notations of Jacod and Protter [11]

with

Here

We write, using that

where

Let two bounded Lipschitz continuous functionals be

Since

On the other hand, owing to (32), we prove that

By (36) and Lemma 5.2 (b) we have

with

6.2 Nested Monte Carlo

The aim of a nested Monte Carlo method is to compute by Monte Carlo simulation

where

and we set

where

where

so that

Still assuming that f is Lipschitz continuous. If

As a consequence, assumption (${\mathrm{SE}_{\beta}}$) and the

Proof.

Set

Assume without loss of generality that

Owing to Burkholder’s inequality, there exists a universal constant

Hence, as

Keeping in mind that

We conclude by setting

For the Central Limit Theorem to hold, the key point is the following lemma.

Assume that

Proof.

First note that

Let

with

We derive from the Strong Law of Large Numbers that

and by continuity of the function

We have now to study the convergence of the random sequence

Owing to the Central Limit Theorem and the independence of both terms on the right-hand side of the above inequality, we derive that

where

By Slutsky’s Theorem, we derive from (39), (40) and (41) that for every

Recall that

as desired. ∎

We are now in a position to prove that the nested Monte Carlo satisfies the assumptions of the Central Limit Theorem 3.3.

Assume that

As a consequence, the ML2R and MLMC estimators (2) and (1) satisfy a Central Limit Theorem in the sense of Theorem 3.3 (case

Proof.

We prove first the

Consequently, it suffices to show that

We saw in the proof of Proposition 6.4 that

We notice that

We prove now (43) using again Lemma 5.2 (b) with the convergence in law of

We notice that, if assumption (37) in Proposition 6.3 holds with

6.3 Smooth nested Monte Carlo

When the function f is smooth, namely

It is clear that

Computations similar to those carried out in Proposition 6.3 yield that, if

SLLN:

The first consequence is that the SLLN also holds for these modified estimators along the sequences of RMSE

CLT:

When (44) is satisfied with

which in turn ensures the

As a final remark, note that if the function fis convex,

These results can be extended to locally ρ-Hölder continuous functions with polynomial growth at infinity. For more details and a complete proof we refer to [9].

7 Conclusion

We proved a Strong Law of Large Numbers and a Central Limit Theorem for Multilevel estimators with and without weights and we exhibited two applications: the discretization schemes for diffusions, where we extend a result of Ben Alaya and Kebaier in [2], and the nested Monte Carlo, first mentioned in the Multilevel framework by Lemaire and Pagès in [12]. The Strong Law of Large Numbers is essentially a consequence of the strong error assumption (${\mathrm{SE}_{\beta}}$) (or of its reinforced version (9)), and of the estimator levels’ independence. The understanding of the behavior of the weights in the Multilevel Richardson–Romberg estimator is also crucial at this stage, as it is for the proof of the Central Limit Theorem which follows. Under some additional assumptions of

A Asymptotic of the weights

We focus our attention on the behavior of

with

and with the convention

For convenience, we set

The sequence

Claim (a) of Lemma 4.3 is then proved. As a consequence,

which proves claim (b) in Lemma 4.3. For the proof of claims (c) and (d), we will need the following:

Let

In particular, for all

Proof.

We write

First note that

as

Consequently,

Moreover, by definition we have

as desired. ∎

Proof of Lemma 4.3 (c) and (d).

(c) Let us consider the non-negative measure on

We notice that it is a finite measure since

Since, as we saw in Lemma A.1,

(d) If

If

Owing to Lemma A.1,

If

Let

where

This leads to analyze

Using that

since

References

[1] Bally V. and Talay D., The law of the Euler scheme for stochastic differential equations. I. Convergence rate of the distribution function, Probab. Theory Related Fields 104 (1996), no. 1, 43–60. 10.1007/BF01303802Search in Google Scholar

[2] Ben Alaya M. and Kebaier A., Central limit theorem for the multilevel Monte Carlo Euler method, Ann. Appl. Probab. 25 (2015), no. 1, 211–234. 10.1214/13-AAP993Search in Google Scholar

[3] Billingsley P., Convergence of Probability Measures, 2nd ed., Wiley Ser. Probab. Stat., John Wiley & Sons, New York, 1999. 10.1002/9780470316962Search in Google Scholar

[4] Bujok K., Hambly B. and Reisinger C., Multilevel simulation of functionals of Bernoulli random variables with application to basket credit derivatives, Methodol. Comput. Appl. Probab. 17 (2015), no. 3, 579–604. 10.1007/s11009-013-9380-5Search in Google Scholar

[5] Duffie D. and Glynn P., Efficient Monte Carlo simulation of security prices, Ann. Appl. Probab. 5 (1995), no. 4, 897–905. 10.1214/aoap/1177004598Search in Google Scholar

[6] Gerbi A. A., Jourdain B. and Clément E., Ninomiya–Victoir scheme: Strong convergence, antithetic version and application to multilevel estimators, Monte Carlo Methods Appl. 22 (2016), no. 3, 197–228. 10.1515/mcma-2016-0109Search in Google Scholar

[7] Giles M., Multilevel Monte Carlo path simulation, Oper. Res. 56 (2008), no. 3, 607–617. 10.1287/opre.1070.0496Search in Google Scholar

[8] Giles M. B., Multilevel Monte Carlo methods, Acta Numer. 24 (2015), 259–328. 10.1007/978-3-642-41095-6_4Search in Google Scholar

[9] Giorgi D., Ph.D. thesis, in progress. Search in Google Scholar

[10] Hall P. and Heyde C. C., Martingale Limit Theory and its Application, Probab. Math. Statist., Academic Press, New York, 1980. Search in Google Scholar

[11] Jacod J. and Protter P., Asymptotic error distributions for the euler method for stochastic differential equations, Ann. Probab. 26 (1998), no. 1, 267–307. 10.1214/aop/1022855419Search in Google Scholar

[12] Lemaire V. and Pagès G., Multilevel richardson-romberg extrapolation, preprint 2014, https://arxiv.org/abs/1401.1177v1; to appear in Bernoulli. 10.2139/ssrn.2539114Search in Google Scholar

[13] Talay D. and Tubaro L., Expansion of the global error for numerical schemes solving stochastic differential equations, Stoch. Anal. Appl. 8 (1990), no. 4, 483–509. 10.1080/07362999008809220Search in Google Scholar

© 2017 by De Gruyter