Historical Materialism 29.4 (2021) 70–113

brill.com/hima

The Commodities Fetish? Financialisation and

Finance Capital in the US Oil Industry

Adam Hanieh

Professor, Institute of Arab and Islamic Studies, University of Exeter, Exeter,

United Kingdom

A.Hanieh@exeter.ac.uk

Abstract

This article explores the financialisation of the world’s most important commodity,

oil. It argues that much of the literature on the financialisation of commodities tends

to adopt a dualistic approach to financial markets and physical producers, where

financial and non-financial activities are assumed to be externally-related and counterposed to one another. The article locates the roots of this analytical separation in

a mistaken acceptance of the fetish character of interest-bearing capital (IBC) – a

view that the exchange of loanable sums of capital represents a relationship between

money-capitalists rather than a relationship to the moment of production. Against

such dichotomous readings, the article argues that the financialisation of oil needs to

be understood as part of the reworking of ownership and control across the oil commodity circuit, expressed through the combined centralisation and concentration of

capital over the money, productive and commercial moments. This argument is demonstrated through an original empirical investigation of the US oil industry, including

20 years of weekly trading data on the New York Mercantile Exchange (NYMEX) and a

detailed study of more than 160 oil and energy-related firms in the US. By mapping the

structural weight and connections between different capitalist actors involved in accumulation across the oil sector, we gain a better understanding of the ultimate dynamics (and beneficiaries) of the carbon economy.

Keywords

financialisation – oil – finance capital – climate change

© Koninklijke Brill NV, Leiden, 2021 | doi:10.1163/1569206X-12342075

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

1

71

Introduction

The last two decades have seen considerable debate around the concept of

financialisation, a term that first originated in Marxist works but which is now

widely employed across a variety of different theoretical traditions.1 In its

most general sense, financialisation captures the clear ascendance of financial

markets, and the evident ways in which financial imperatives have come to

impose themselves over every sphere of human life.2 A frequently cited definition locates financialisation as ‘the increasing role of financial markets, financial motives, financial actors, and financial institutions in the operation of the

domestic and international economies’.3 This shift has been enabled through

the development of myriad financial instruments and techniques, most significantly those based upon the securitisation of assets and derivative contracts. Taken as whole, these new instruments have greatly expanded the size

of global financial markets and the volume of cross-border financial flows.4

Amidst this growing weight of financial markets and processes, a key focus

of debate has been the potential relationship between financialisation and

increased price volatility for various commodities.5 Discussion around this

topic initially emerged in the first decade of the current century, when an array

of new financial actors (including investment banks, hedge funds, pension

funds, and asset management firms) began to direct huge amounts of capital

into commodity futures markets – centralised exchanges where contracts to

buy and sell specified amounts of a commodity at some point in the future

are traded. The involvement of these financial actors in commodity futures

upended the traditional structure of commodity markets, particularly the hitherto dominant role of individuals and firms that were directly engaged in the

production and exchange of physical commodities.6 Commodities were said to

have become ‘financialised’ – transformed into new financial assets that could

be traded and speculated on in financial markets, with little concern towards

physical delivery. For many analysts, these speculative activities served to disconnect commodity prices from market ‘fundamentals’ (such as supply and

1 The author would like to thank the Historical Materialism editorial board, Demet Dinler,

Mazan Labban, Jeffrey R. Webber, Rafeef Ziadah, and the other anonymous reviewers of this

article for their generous engagement and critical comments on the arguments below.

2 Krippner 2005; Mader, Mertens and van der Zwan (eds.) 2020; Epstein (ed.) 2005; Martin

2002.

3 Epstein (ed.) 2005, p. 3.

4 Durand 2014.

5 McGill 2018.

6 Clapp 2015.

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�72

Hanieh

demand), and were thus seen as the prime culprit in an unprecedented spike

in commodity prices that occurred across a broad range of different markets

between 2003 and 2008 – including energy, agriculture, and metals.7

Much of this work on commodity financialisation is extremely rich and

carries important real-world implications, not least for poorer countries that

may be highly dependent upon global food and energy imports. Nonetheless,

the near-exclusive focus of this literature on the question of price formation

has served to elide other fundamental questions, most notably the relationship between financialisation and the changing patterns of capital ownership

and control across the wider commodity circuit. In this respect, much of the

literature on commodity financialisation tends to adopt a dualistic approach

to financial markets and physical producers, where financial and nonfinancial activities are assumed to be externally-related and counterposed to

one another. Within this framing, a supposedly determinant financial sphere

imposes itself upon the moments of production and circulation of value; in

turn, these latter moments are treated as discrete and ancillary to processes of

financial accumulation.

In what follows, I argue that the roots of this prevailing analytical separation

of the financial and non-financial spheres lie in a mistaken acceptance of the

fetish character of interest-bearing capital (IBC) – a view that the exchange of

loanable sums of capital represents a relationship between money-capitalists

rather than a relationship to the moment of production. Against such dichotomous readings, my goal is to draw out how the financialisation of commodities

is ‘internally related’8 to the moments of production and circulation within

a unitary circuit of capital.9 Most specifically, I will show that financialisation needs to be understood as part of the reworking of capitalist power over

commodity circuits, expressed through the combined centralisation and concentration of capital over the money, productive and commercial moments.

Building upon other Marxist work, I argue that this process of class formation is embodied in the increased power of a distinct class of finance capital –

understood here as the entwined ownership and control of capital across the

commodity circuit in toto (and not in the distorted sense of ‘bank control of

industry’ that is sometimes advanced in the literature).

7 Masters 2008.

8 Ollman 2003.

9 Ollman’s explication of the concept of ‘internal relations’ is based upon Marx’s perspective

that the relations existing between objects (and concepts) should not be considered external

to the objects themselves but as part of what actually constitutes them. Any object under

study needs to be seen as ‘relations, containing in themselves, as integral elements of what

they are, those parts with which we tend to see them externally tied’ (Ollman 2003, p. 25).

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

73

These arguments are developed below through a focus on the world’s most

important commodity – oil. In the initial part of the paper, I lay out some of

the Marxist debate around financialisation, with particular attention to the

concepts of interest-bearing capital and finance capital. I then turn to a survey of the general literature on the financialisation of commodities, including

oil. Following this theoretical framing, the second half of the paper presents

an original empirical investigation of the composition of class power across

the oil commodity circuit in the United States. This empirical analysis first

examines US oil contracts on the New York Mercantile Exchange (NYMEX),

one of the most important futures markets in the world and where futures

and options contracts for the global oil benchmark, West Texas Intermediate

(WTI), are traded. Here, I analyse 20 years of weekly trading data to show how

oil has been financialised, i.e. abstracted from its concrete use value to become

a financial asset traded by large financial institutions – including investment

banks, Asset Management Firms, and hedge funds/private equity firms. I then

present a detailed study of more than 160 oil and energy-related firms in the

US, mapping the nature of capital ownership across these firms and their relationship to oil’s financial markets. This analysis confirms that the leading drivers of the financialisation of oil are simultaneously deeply imbricated in the

entire oil value chain, from exploration and production through to pipelines,

transportation, and storage, and from services and refining and processing

through to the generation and transformation of power.

At a more general level, this argument is intended as a contribution to

strategic debates around efforts to halt anthropogenic climate change. Most

notably, by mapping the structural weight and connections between different

capitalist actors involved in accumulation across the oil sector, we gain a better understanding of the ultimate dynamics (and beneficiaries) of the carbon

economy. Banks, investment funds and other institutional holders of moneycapital are not simply passive vehicles that profit from their investments in

oil companies (and who might, therefore, be collectively ‘shamed’ into doing

otherwise).10 Rather, the complex relationship between oil’s financialisation

and its necessary production (and circulation) as a physical commodity is

reflected in the growing overlap of capital ownership across all moments of

the oil circuit. The class of finance capital that superintends this process must

10

This is not meant as a criticism of divestment campaigns as a tactic that can play a significant role in confronting and raising awareness around the different actors involved in

climate change. On the contrary, it is to argue for a more structural consideration of the

systemic role played by these financial actors within the oil circuit.

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�74

Hanieh

be viewed as a leading, and systemic, driver of climate change – not simply an

accidental or contingent epiphenomenon.

2

Financialisation, Interest-Bearing Capital, and Finance Capital

Broadly speaking, the literature on financialisation encompasses three distinct

theoretical concerns. The first of these relates to the roots of financialisation

and its implications for capitalist periodisation – whether to understand financialisation as indicative of a new stage or marker of neoliberal capitalism,11 a

symptom of capitalist stagnation in an environment of monopoly and overaccumulation,12 or the outcome of declining profit rates and long-term structural crisis.13 A second focus of the literature explores the varied implications

of financialisation for social, political, and economic power. Here, contributions have investigated the role of financialisation in enabling US hegemony

and emergent patterns of geopolitical competition,14 as well as the distributional impacts of financialisation on wealth and inequality.15 Finally, a third

strand of the literature analyses how financialisation is changing institutional and behavioural patterns – including those of banks,16 households and

individuals,17 and firms.18

Work across these three themes has generated significant insights. Nonetheless, a basic problem continues to mark much of the literature: a high

degree of imprecision and ambiguity around what the term financialisation

11

12

13

14

15

16

17

18

Arrighi 1994; Boyer 2000; Lapavitsas 2013; Fine 2010a.

Bellamy Foster 2010; Ivanova 2017.

Brenner 2006; Harman 2009; Roberts 2016; Shaikh 2011.

Crotty 2005; Duménil and Lévy 2004; Panitch and Gindin 2012.

Stockhammer 2012; Zalewski and Whalen 2010; Lapavitsas 2013; Montgomerie 2009.

Dos Santos 2009.

Martin 2002; van der Zwan 2014.

Froud, Haslam, Johal and Williams 2000; Stockhammer 2004. As is evident from the works

cited in this paragraph, financialisation is very much a twenty-first century concept. One

important exception to this is Giovanni Arrighi’s influential book, The Long Twentieth

Century (1994), which presciently captured many of the themes in more recent debate.

Drawing upon Braudel and Wallerstein, Arrighi argued that world hegemons typically

experience a period of financial expansion during their phase of decline. This financial

expansion is a result of the pressures of overaccumulation, and (somewhat paradoxically)

allows the declining hegemon to realise on-going returns on investment by financing the

rise of the new hegemon. Arrighi’s argument is distinct from much of the recent financialisation literature in that it explicitly sees financial expansion as a recurrent historical

phase of capitalist development at the world scale (see Christophers 2015 for a discussion

of this point).

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

75

actually means.19 As Fine points out, financialisation is often understood

somewhat tautologically as simply meaning ‘more’ finance20 – with little effort

given to clarifying what distinguishes financial from non-financial activities, or

to precisely locating the place of finance within the overall circuit of capital.

In this respect, Christophers has commented that the concept lies ‘somewhere

in between’ the extremes of ‘powerful and innovative theory … and superficial

and redundant label’, claiming that it has made an ‘at best, debatable’ specific

theoretical contribution to social science.21 Christophers and others22 underline here the large array of different meanings attached to financialisation that

have generated a set of associated empirical and methodological challenges:

which indicators to use in measuring financialisation, what time frames to

consider in comparing different case studies, and how to distinguish the trajectories of financialisation across various parts of the world market.23

Given these well-founded critiques, how might financialisation be better understood in an analytical sense – i.e. in ways that can avoid the tautological and overly-descriptive (and therefore redundant) definitions so

often encountered in the literature? In this regard, one of the more robust

theoretical accounts is that offered by Ben Fine, who tethers his understanding of finance and financialisation to a conceptualisation of value24 and its

movement through the wider circuit of capital – most explicitly through his

use of Marx’s category of interest-bearing capital (IBC).25 Following Marx,

Fine understands IBC as surplus capital – capital drawn from idle money or

‘hoards’ – that is lent by money-capitalists to other capitalists for the purposes

of producing profit. This loanable capital may be put to use in the exploitation of living labour, thereby generating surplus value, a part of which the

lender of IBC then appropriates in the phenomenal form of interest. IBC may

also be lent to other economic agents (e.g. merchants, governments, landowners, workers) for activities that are not productive of surplus value26 –

19

20

21

22

23

24

25

26

Christophers 2015.

Christophers and Fine 2020, p. 21.

Christophers 2015, p. 187.

Stockhammer 2004; Christophers 2015; Davis 2017; Christophers and Fine 2020.

Hanieh 2016; Rethel 2010.

For a recent discussion on Marxian value theory and financialisation, see Christophers

and Fine 2020. In this discussion, Christophers notes that if we are to understand financialisation, then how ‘we think value theory remains indispensable … [it] cannot be

dodged’ (Christophers and Fine 2020, pp. 25–6). Fine presents a defence of the classical

Marxist view of finance as unproductive of value, while Christophers remains unsatisfied

with this perspective (see also Christophers 2018).

Fine 2010a, 2010b, 2013; Christophers and Fine 2020.

Harvey 1982, p. 257.

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�76

Hanieh

nonetheless, the ultimate source of the interest appropriated by the lender

remains the total surplus value produced at a societal level.

As with all his conceptual categories, Marx grounded his understanding of

IBC in its historical genesis (see, in particular, Capital Volume III and Theories

of Surplus Value), arguing that IBC’s ‘antiquated form’ was usurer’s capital and

‘its twin brother, merchant’s capital’, which existed as ‘antediluvian forms of

capital … long preced[ing] the capitalist mode of production and … found in

the most diverse economic formations of society’.27 With the development of

capitalism, interest-bearing capital moves from being a separate sphere (i.e.

usurers or merchant’s capital) to being one that is incorporated – ‘subjugated’

is how Marx frequently refers to this process – within the sphere of value

production.

According to Fine, IBC today sits ‘at the heart of financialization … in that

IBC has expanded enormously both intensively (within existing activities)

and extensively (to new areas of applications) over the past three decades’.28

Financialised capitalism, in other words, is defined by the unprecedented

enlargement of IBC throughout all spheres of human activity, such that it now

mediates all capitalist social relations – including those between capitals, as

well as those between capital and labour.29 The huge expansion of financial

markets – facilitated by the proliferation of new financial instruments that link

past, present and future – is a direct form of appearance of this envelopment

of all aspects of social life by IBC. As Fine notes, this understanding of financialisation helps move the discussion beyond the ‘amorphous and unstructured definition arising from Epstein30 in which financialization is seen simply

as more of finance and its effects’.31

Within this account of financialisation, there are two key features of IBC

that deserve emphasis. The first of these is that IBC is not directly productive

of surplus value – although it may expand the possibility for value production (through its role in intensifying productivity or speeding up the turnovertime of capital within the productive sphere). In turn, when the owner of IBC

advances a sum of money to another capitalist, they gain ownership rights

over value that is yet to be produced. Marx described these drawing rights as

‘fictitious capital’, ownership titles (such as shares, bonds, etc.) that represent

a claim on ‘a future stream of revenues generated by an asset, and which can

27

28

29

30

31

Marx 1959, p. 593, cited in McNeill 2021, pp. 281–2.

Christophers and Fine 2020, p. 23.

McNally 2009, p. 56.

Epstein (ed.) 2005.

Christophers and Fine 2020, p. 21.

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

77

be bought and sold independently of the asset itself’.32 This is ‘value created

in exchange ahead of the production and realization of (surplus) value’.33 And

because fictitious capital represents a title of ownership to future value, it has

a price that can be traded ‘in anticipation of the actual production and realization of value in the future’.34 As a consequence of stagnant profit rates and

the persistent overaccumulation of capital, the volume of fictitious capital has

expanded to unprecedented levels35 and has become ‘the object of incessant

trading in globalised financial markets … lodged in very powerful financial

conglomerates possessing the capacity to dictate their policies to governments

through a variety of economic channels and political institutions’.36

A second key feature of IBC flows from this first observation. While IBC does

not directly produce value, but rather appropriates part of the total surplus

value, this act of appropriation appears to us as if value has been generated by

the productive capitalist in exchange with the lender of IBC (M – M′). Marx

describes this form of appearance as a fetish – or relation ‘turned upside down

in the consciousness of men’37 – because it seems to us that the lender of IBC

only has relations with other capitalists and not with the wage-worker, yet ultimately the source of the value appropriated by the money-capitalist is actually

found in the labour – capital relation.38 In other words, we mistake the form of

appearance that the value-relation takes in our consciousness (surplus money

begetting more money through the process of exchange) for the relation

itself.39 In this respect, Marx is insistent on repeatedly drawing attention to IBC

32

33

34

35

36

37

38

39

McNeill 2021, p. 283.

Labban 2010, p. 545.

Labban 2010, p. 545; see also Harvey 1982.

Durand 2014.

Chesnais 2016, p. 37.

Marx 1971, p. 476.

See McNeill 2021, Chapter 5, for an illuminating discussion of this point. Elsewhere, Marx

writes: ‘One portion of profit, as opposed to the other, separates itself entirely from the

relationship of capital as such and appears as arising not out of the function of exploiting wage-labour, but out of the wage-labour of the capitalist himself. In contrast thereto,

interest then seems to be independent both of the labourer’s wage-labour and the capitalist’s own labour, and to arise from capital as its own independent source. If capital

originally appeared on the surface of circulation as a fetishism of capital, as a valuecreating value, so it now appears again in the form of interest-bearing capital, as in its

most estranged and characteristic form.’ (Marx 1959, p. 829, cited in McNeill 2021.)

Sayer 1987. I draw this argument from Sayer 1987, which presents a highly perceptive

account of ideological forms and the process of abstraction. See Banaji 2010 for an analogous argument around the relation between wages and the concept of unfree labour.

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�78

Hanieh

as a fetish, describing it inter alia as the ‘pure fetish form’,40 ‘the consummate

automatic fetish’,41 the ‘mystification of capital in its most extreme form’,42 ‘the

most extreme inversion and materialisation of production relations’,43 and

‘the complete objectification, inversion, and derangement of capital … a Moloch

demanding the whole world as a sacrifice belonging to it of right’.44

Much of the discussion around commodity financialisation is marked precisely by an uncritical internalisation of this kind of fetishism. Specifically,

there is a tendency to take the ideological forms that reality takes – a sharp

discontinuity between finance and the so-called ‘real’ economy – as reality

itself, instead of recognising financial accumulation as a specific moment of

the circuit of capital (represented in the exchange of IBC) that is distinct but

nonetheless internally-related45 to the labour – capital relation. Analytically

and methodologically, this fetish translates into a kind of dualism, which

treats financial markets as a disconnected and autonomous site of accumulation, rather than focusing attention on the mutually-constituted relationships

between financial markets and the circulation and production of physical

commodities.

A critique of this fetish can provide significant insight into a theme that has

not been adequately explored in the wider literature on commodities: the relationship between financialisation and processes of capitalist class formation. By

approaching the fetish as an ‘inversion’ of reality, we can see financialisation as

not simply an expansion of IBC in the form of fictitious capital through vastly

widened financial markets, but as actually representing the tendential combination of the financial, productive, and commercial circuits within closely

linked ownership structures. In other words, at the level of class composition, financialisation embodies a closer imbrication of the financial and nonfinancial spheres – despite the formal appearance otherwise – and the growing

together of these different moments of accumulation under the hegemony of

what is best described as ‘finance capital’.46 The latter term is used here advisedly, to indicate the increasingly integrated and monopolised control over

different moments of the circuit of capital by a tightly linked class of capital

owners (not at all in the frequently misconstrued sense of ‘the domination of

40

41

42

43

44

45

46

Marx 1959, p. 393.

Marx 1971, p. 455.

Marx 1971, p. 494.

Marx 1971, p. 462.

Marx 1971, p. 456; italics in original.

Ollman 2003.

Harvey 1982; Serfati 2011; Chesnais 2016.

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

79

banks over industry’).47 As François Chesnais notes, finance capital represents

the ‘simultaneous and combined centralisation/concentration of money capital, industrial capital, and merchant or commercial capital’,48 regardless of the

different institutional paths this might take globally. Rejecting any firm division between the productive, financial, and commercial spheres – in effect,

refusing to take the fetish as reality – is not simply a matter for contemporary capitalism. As Jairus Banaji demonstrates so convincingly,49 the growing

together of different types of capital (e.g. merchant and industrial capitals)

within single ownership structures was precisely the path taken in the actual

historical development of capitalism. Indeed, as cited above, this is in accordance with Marx’s own comments on the early historical genesis of IBC as usurers’ capital.

3

The Financialisation of Oil

Given this general theoretical framework, it is now possible to turn more concretely to the financialisation of oil. As noted earlier, a massive influx of new

financial flows entered global commodity markets through the first decade of

the 2000s, with one study estimating a 45-fold increase in these flows between

2001 and 2011, reaching $450 billion in 2011.50 These investments predominantly

came from an array of new financial actors not traditionally known for their

involvement in commodities, and who had been permitted to enter the commodity business following the de-regulation of commodity markets in the early

2000s. This was a moment of intense change in US financial markets – and a

47

48

49

50

As is well-known, the term finance capital originates in the classic work of Rudolf

Hilferding (1981) who suggested the domination of banks over industry as a defining and

universal feature of advanced capitalism (subsequently adopted by Lenin as part of his

theorisation of imperialism). There is no space here to provide a full genealogy of the term

(see Overbeek 1980; Harvey 1982; Lapavitsas 2009), but contemporary notions of finance

capital have moved away from simply equating finance capital with banks or financial

corporations. Instead, a focus is placed on the increasingly unified control over different

moments of the circuits of capital, articulated through the ‘contradiction-laden flow of

interest-bearing capital’ (Harvey 1982, p. 317). Harvey terms this a ‘process view of finance

capital’ (Harvey 1982, p. 283). Krippner 2005, for example, discusses this in relation to the

US; Chesnais 2016 for US, Britain, France, Germany; Serfati 2011 analyses transnational

corporations through the lens of finance capital; Hanieh 2019 looks at finance capital and

Islamic banking in the Gulf states of the Middle East.

Chesnais 2016, p. 8; italics in original.

Banaji 2010, 2020.

Bicchetti and Maystre 2012, p. 4.

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�80

Hanieh

salient reminder that law is always the midwife of market innovation – with

a raft of new regulations (notably the Commodity Futures Modernization Act

of 2000) opening US commodity markets to global investors and allowing

large investment banks and other financial institutions to trade in commodity derivatives with little regulatory oversight.51 Derivative contracts traded on

commodity futures markets consequently grew sevenfold in volume between

2000 and 2010.52

Oil is the largest, most liquid, and most interconnected of these futures

markets.53 Oil futures enable traders to fix a price for selling (or purchasing) a

set quantity of oil (specified in barrels) at a particular future date. Such derivatives can be bought and sold on a range of futures markets, the most prominent of which are the NYMEX (where the North American oil benchmark, West

Texas Intermediate (WTI), is traded) and the Intercontinental Exchange (ICE),

where Brent Oil futures can be bought and sold. Although the oil contracts

traded on NYMEX and ICE contain commitments to deliver physical oil at

some point in the future, close to 100% of these contracts are never physically delivered. Instead, these are paper transactions, with traders ‘offsetting’

their positions by buying or selling the equal and opposite trade towards the

end of the contract expiry period.54 These contracts are useful to oil producers (or consumers) who seek to guarantee a particular price for their sale (or

purchase) of oil in future months.55 But as with any futures market, these contracts also allow traders who do not own or want any physical barrels to trade

in ‘paper barrels’ – with the hope that the future price of these barrels will

appreciate.56

51

52

53

54

55

56

Omarova 2013; Conlon 2018.

UNCTAD 2011, p. 15.

Alquist and Kilian 2007; Büyükşahin, Haigh, Harris, Overdahl and Robe 2008; Tang and

Xiong 2010.

This kind of offsetting trade is necessary for NYMEX WTI Futures because physical delivery of oil is obligatory at the expiration of contract. In contrast, ICE Brent Oil futures

contain an option for cash settlement rather than physical delivery.

For example, an oil producer might sell a futures contract for 1000 barrels per day for

October 2020 at $50 per barrel. When October arrives, the actual price of oil per barrel is

compared to $50, with the producer paying the counterparty (who bought the contract)

the difference if the price is higher than $50, or receiving the difference from the counterparty if the price is less than $50. If the NYMEX price ends up as $40 for October, then

the producer will sell their physical oil for that lower price, but will also receive $10 ‘on

paper’ from the counterparty to the hedge. The end result is that the producer is paid the

equivalent of $50 per barrel.

The theoretical possibility of delivery, however, is important – as this provides a link

between prices in the futures market and those in the spot (physical) market. If a contract

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

81

Through the early 2000s, billions of dollars were directed into oil futures

by financial firms and other institutional investors (such as hedge funds) who

looked to the highly profitable opportunities presented by this trade in paper

barrels. At the most general level, the ‘financialisation of oil’ refers specifically

to these kinds of investments – activity in oil futures that is ‘driven purely

by financial interests through the large-scale entry of financial investors’.57

According to one well-known former hedge fund manager, Michael Masters,

the total increase in demand for ‘paper barrels’ in the oil futures market

between 2003 and 2008 reached 848 million barrels, a figure that was roughly

equivalent to the increase in physical demand for oil from China.58 Although

this was a generalised phenomenon experienced across the food, metals, and

agricultural sectors, the influx of financial flows into oil futures far surpassed

that of other commodities – for the large financial firms who drove these flows,

oil had become a distinct financial asset within a portfolio of wider investment

strategies.

Significantly, however, this deepening financialisation of oil occurred alongside an unprecedented spike in the price of oil, which rose from $32 per barrel

in 2003 to a peak of $147 in mid-2008. Because of the particular way that oil

prices are actually set – essentially the ‘spot’ or physical price is closely linked

to the price of a paper barrel in the futures market59 – the increased financial

flows into oil futures were seen by many as a key explanation for this dramatic

rise in prices. Indeed, the US Congress launched an investigation into this

57

58

59

for delivery in October matures, for example, then the amount paid for this oil on delivery

must be equal to the October spot price.

Staritz, Newman, Tröster and Plank 2018, p. 4.

Masters 2008. Masters also claimed that speculators had stockpiled ‘via the futures market, the equivalent of 1.1 billion barrels of petroleum, effectively adding eight times as

much oil to their own stockpile as the United States has added to the Strategic Petroleum

Reserve over the last five years’ (Masters 2008).

For most of the twentieth century, oil was mostly traded using long-term contracts in

which prices were set (or ‘administered’) by oil majors or large oil-producing countries

(see Fattouh 2011). With the establishment of the NYMEX WTI contract in 1983 (and the

Brent oil contract in the same year), trade in oil increasingly shifted towards a marketbased pricing system reliant on the futures market. As a leading energy industry expert

puts it: ‘What must be recognised is that futures … evolved in many cases from conduits

providing access to physical supplies into platforms performing functions of price discovery and information processing. Spot prices are often influenced by the futures markets,

with causality being reversed compared to what is implied by conventional wisdom. A

trader buying a physical cargo of oil sometimes does not realise that they become an

unwilling participant in the derivative markets through the reverse link between forward

and spot prices. This means that the traditional distinction between the physical and

derivative traders becomes fuzzy.’ (Kaminski 2012, p. 8.)

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�82

Hanieh

relationship in 2008, which saw several Senate hearings and testimonies from

a range of high profile industry experts. Importantly, over this period, oil sat

at the centre of a broader boom in commodity prices with the nominal prices

of metals increasing by 230%, the price of food doubling, and those of fertilizers increasing fourfold.60 For many poorer countries dependent on food and

energy imports, these rising prices had profoundly negative implications.61

The large econometrics literature exploring the link between financialisation and the price of oil has mostly centred upon the issue of speculation, and

is plagued by a range of methodological problems stemming from its neoclassical assumptions.62 These problems include the conceptual categories used (e.g.

how to separate ‘speculation’ from legitimate ‘risk management’),63 difficulties

in differentiating economic actors (e.g. data that cannot distinguish between

actors who are both speculators and producers at the same time),64 and issues

of endogeneity (e.g. how to model expectations around the so-called ‘fundamentals’ of supply and demand, when these expectations affect both physical

and financial traders).65 Largely as a result of these inherent methodological

limitations, the mainstream economics literature is completely unsatisfactory.

Indeed, one recent meta-study surveying the findings of 100 empirical studies

concluded that the number of those where speculation was found to have a

statistically positive impact on commodity markets was about equivalent to

the number where it was found to have a statistically negative impact.66

60

61

62

63

64

65

66

Baffes and Haniotis 2010.

Of course, for major commodity exporters, such as the Gulf Arab states, this price boom

provided an enormous financial windfall that significantly impacted their place in global

and regional economies (Hanieh 2018).

See Adams, Collot and Kartsakli 2020 and Fattouh, Kilian and Mahadeva 2013 for summaries of this literature.

For a discussion of this issue, see McGill 2018, who notes: ‘It is … extremely difficult to

articulate a definition of speculation that is not in some way tautological or at least

redundant.’ (p. 10.)

As Jennifer Clapp has pointed out in relation to agricultural commodity markets, it is very

difficult to distinguish between hedging or financial speculation undertaken by commodity trading firms (Clapp 2015).

A larger issue here is the mistaken assumption that prices should correspond to ‘fundamentals’ in the absence of speculation. As Marx himself noted, the price-form itself necessarily deviates from supply and demand in order to be adequate to ‘a mode of production

whose laws can only assert themselves as blindly operating averages between constant

irregularities’ (Marx 1990, p. 196). I am indebted to Demet Dinler for this observation.

Haase, Zimmermann and Zimmermann 2016. The paper measured the impact of speculation on six variables: price, returns, risk, premiums, spreads, volatility, and spill-over.

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

83

Moving beyond the narrow focus on speculation – as Anna Zalik perceptively comments, all ‘[f]uture pricing is by definition speculative’67 – there is

strong evidence that increased financial activity in commodity futures has a

significant impact on price volatility in conjunction with other supply and

demand factors.68 There is an intuitive logic to this – following the deregulation of commodity markets the spot prices of most commodities became

referenced to future prices, and today both producers and traders make decisions based upon these ‘benchmark’ prices.69 Indeed, in the case of oil, the

price announced daily for WTI and Brent is a direct quote of what a ‘paper

barrel’ costs on the futures market (not, as is widely but mistakenly thought,

the actual price of a physical barrel of oil). In light of this, a large range of studies across different commodities and geographies has confirmed the ways in

which price formation is now connected to the volume and volatility of financial activity in futures markets.70

In comparison to this extensive literature on the question of price dynamics –

and echoing the critique made in the preceding section – the impact of financialisation on other moments of the commodity circuit remains relatively

underexplored.71 There is, as Staritz et al. note,72 a ‘perception of commodity

derivatives as investment vehicles disconnected from physical markets and

real-world processes of commodities production and trading’.73 Nonetheless,

there is an emerging body of work that analyses how the financialisation of

commodities has accentuated the power of large traders and financial firms –

and weakened the position of labour – across the value chain. This can manifest itself in the subordination of smaller firms, frequently located in the Global

South, to financial imperatives set by futures markets in the North. In this manner, financialisation not only squeezes conditions of labour across the entire

67

68

69

70

71

72

73

Zalik 2010, p. 554.

Nissanke 2011.

Ederer, Heumesser and Staritz 2016, p. 463.

Clapp and Helleiner 2012; Tang and Xiong 2010; Newman 2009; Bargawi and Newman

2017; Basak and Pavlova 2016; Ederer, Heumesser and Staritz 2016; Staritz, Newman,

Tröster and Plank 2018.

McGill 2018; Staritz, Newman, Tröster and Plank 2018.

Staritz, Newman, Tröster and Plank 2018.

They also note that while Global Commodity Chain (GCC) and other related approaches

have examined the role of lead firms in disciplining and extracting value across the value

chain, this literature has ‘largely neglected the role of finance and financial markets in

shaping the structure and functioning of commodity chains and the outcomes for different actors in commodity sectors’ (Staritz, Newman, Tröster and Plank 2018, p. 2).

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�84

Hanieh

value chain,74 it can also widen class differentiation75 and expose smaller producers and traders to increased volatility and risk.76 Furthermore, for countries

that are heavily reliant upon particular commodity exports – as Zambia77 and

Chile are with copper78 – financial markets can create significant pressures to

restructure tax laws and weaken various social and environmental regulations.

There has been little examination of these broader issues in the literature

on oil, which, as McGill notes,79 largely continues to treat financialisation as

a purely financial phenomenon restricted to the futures market, rather than a

process whose effects are deeply connected to the dynamics of production and

trading. The one significant exception to this is the work of Mazan Labban,80

whose understanding of financialisation pivots around the category of fictitious capital. For Labban, oil futures markets ultimately need to be understood

as sites in which fictitious capitals – titles to future yet-to-be realised value –

can be bought and sold.81 With greater amounts of oil ‘traded in financial

markets than in spot markets … major oil companies have increasingly turned

towards financial markets for shorter term returns on their investments’.82

As a result, the financialisation of oil has transfigured how prices are formed,

moving away from price determination based on the availability of physical

supplies of oil towards prices that reflect the trading of fictitious capitals in

financial markets.83 There is thus no direct causal relation between the price of

oil and levels of investment in the physical supply of oil. Importantly, however,

Labban is at pains to stress that this does not mean that the effect of physical

production and trading of oil has disappeared or is no longer important. Oil is

traded in both physical and financial markets simultaneously,84 and thus the ‘oil

market’ is composed of two internally-related abstractions – ‘a physical commodity circulating in physical (and financial) markets and its representation as a financial asset [or fictitious capital, AH] circulating in financial (and

74

75

76

77

78

79

80

81

82

83

84

Labban 2014.

Newman 2009.

Staritz, Newman, Tröster and Plank 2018; Bargawi and Newman 2017; Isakson 2015.

Kesselring, Leins and Schulz 2019.

Arboleda 2020.

McGill 2018, p. 647.

Labban 2010, 2014.

For Labban, financial derivatives are a clear embodiment of fictitious capital – they have

no intrinsic value but are instead tied to the difference ‘between the spot price of an

underlying asset and an agreed-upon price at an expiration date specified in the contract’

(Labban 2010, p. 545).

Labban 2010, p. 542.

Labban 2010, p. 547.

Ibid.

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

85

physical) markets’.85 There is a different materiality and temporality encountered in both these markets, but they are linked and thus mutually-formed.

One of the significant features of this argument is that it avoids the dualism often encountered in debates around the financialisation of oil (or other

commodities). The ‘fundamentals’ of oil do matter – i.e. levels of production,

availability of supplies, downstream demand for oil products, infrastructure

bottlenecks and so forth – but they do so in their mediation through financial markets and their effects on expectations around future conditions.86 As

Labban comments:

Oil companies have not become purely financial outfits. Their profits may

have derived increasingly from financial investments and larger portions

of their income are likely to be expended on dividends to shareholders,

stock buyback (partly to compensate management), and interest and

debt reduction. But investment in production still occurs, except now it is

‘disciplined investment’, i.e. disciplined by the dictates of financial logic

and centered on the creation of ‘ever-greater shareholder value’. Indeed,

oil companies continue to invest in production and in the expansion

of reserves precisely because their ‘capitalization’, their market value,

based as it were on perception about their ability to generate profit, is

tied to the profitability of oil … Thus, even when profits seem to derive

from financial markets and investment is disciplined by the dictates of

finance, profits are fundamentally tied to the production and realization

of value from the production and trade of physical oil, in order for wealth

in the form of ‘financial claims on expected future earnings’ to materialize as profit. And this ultimately depends on the ability of oil to make the

salto mortale [‘leap of faith’]87 in the market.88

Labban’s observation here is a sharp reminder that processes of financialisation – ultimately a reflection of large quantities of surplus capital seeking

valorisation in the form of IBC – cannot be separated from the moment of

commodity production. In reality, both the financial and productive spheres

comprise internally-related moments within the broader circuit of capital,

85

86

87

88

Labban 2010, p. 542.

Labban 2010, p. 548. Indeed, one indication of this is the close attention that commodity

traders on NYMEX pay towards ‘real world’ factors such as wars, supply-side restrictions,

weather, and so forth.

Labban is referring here to the moment of realisation of value, when the commodity is

actually sold in the market place.

Labban 2010, p. 550.

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�86

Hanieh

M – C … P … C′ – M′. Elsewhere, Labban comments, ‘financialization cannot

emancipate accumulation from the production (and realization) of value and

therefore it can only proceed alongside the extraction of value in the labour

process, even when that is deferred to the future’.89 As noted earlier, much of

the mainstream discussion of financialisation – and not a small proportion of

Marxist work – tends to ignore this crucial point and adopt a dualist framing

of the financial and productive moments, with the financial sphere conceived

as separate from, and in opposition to, so-called ‘real’ activities. There is, as

Powell observes,90 a tendency within this wider literature to treat financial

activities as ‘residual and speculative [which] unnecessarily dichotomizes the

relationship between industry and finance’.

Bringing these insights together with the earlier discussion of IBC and

finance capital, how might patterns of capital control and ownership – i.e.

processes of class composition – reflect these interdependencies between the

financialisation of oil and the wider oil commodity circuit? In the remainder

of this paper, I attempt to answer this question through an empirical investigation of the US oil industry. To do so, this firstly requires a closer look at

the longer-term dynamics of the oil futures market, with the principal aim of

understanding the activities that take place on this market and, most significantly, the key financial actors who are involved in the buying and selling of

futures and options contracts. I then turn to examining the relations between

these same financial actors and the production and circulation of oil (as value)

through its circuit – stretching from oilfield exploration, transport and storage,

through to the sale of petroleum products and the generation of power.

4

The Financialisation of US Oil Markets

A key indicator of the financialisation of oil is the tremendous growth in

the trade of oil futures and options, which provide a commitment to deliver

a particular quantity and quality of crude oil at some specified point in the

future.91 These contracts are bought and sold on exchanges, the two most

important of which are the New York Mercantile Exchange (NYMEX, for West

Texas Intermediate oil) and the Inter-Continental Exchange (ICE, for Brent

89

90

91

Labban 2014, p. 478.

Powell 2018.

A futures contract is an agreement to buy or sell oil at a certain price in the future. An

options contract gives the holder the right (but not the obligation) to buy or sell on the

specified date. In addition to the grade of oil, these contracts specify the volume, price,

time period, and location where the oil should be delivered.

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

87

oil). These two exchanges are critical to the world oil market – since the prices

of WTI and Brent are the two main global ‘benchmarks’ through which the

prices of the myriad other kinds of crude oil from across the world are set and

commensurated.92

The discussion here will focus on the market for WTI, which is a light sweet

crude produced from a large number of different oil fields in the US. Unlike

sea-borne Brent, WTI crude is delivered by an extensive system of pipelines

and rail to the land-locked destination of Cushing, Oklahoma.93 Due to this

arrangement, the price of WTI can be heavily impacted by transportation bottlenecks or limited storage capacity. WTI underlies the WTI Light Sweet Crude

Oil futures and options contracts that have been listed since 1983 on the NYMEX

(a division of the CME, Chicago Mercantile Exchange), one of the most liquid

and deep financial markets in the world. NYMEX WTI contracts are dated for

delivery by calendar month (for example, June 2021) and can be traded up to

ten years in advance. WTI is the main oil benchmark for North America, with

most of the oil produced, traded, and imported into the US priced at a differential to WTI.

One reflection of the sheer growth in the NYMEX WTI market over recent

years is the prodigious expansion in the market’s average daily volume (ADV),

which measures the average number of WTI contracts that exchange hands

each day. Between 2007 and 2020, the ADV of WTI futures and options traded

on NYMEX has more than doubled, from 0.485 to 1.1 million contracts (NYMEX/

COMEX 2020 and 2008).94 Each NYMEX contract represents 1000 barrels of oil,

so the latter figure is equivalent to a daily trade of around 1.1 billion barrels of

oil. Figures such as these received significant headlines during the commodity

spike of 2003–8, with some analysts pointing out that the ‘paper barrel’ trade

was much higher than daily physical oil usage in the US – in 2020, around

70 times more paper barrels were traded each day than actually used – and

that this provided strong evidence for excessive levels of speculation in the

market.95

92

93

94

95

Oil drawn from other locations is priced at a differential to these benchmarks. These price

differentials are dependent upon various factors, including the physical differences of the

oil (such as viscosity, sulphur content, density and so forth), the cost of transportation,

and the demand for particular refined products.

Known as ‘the pipeline crossroads of the world’, the Cushing system is made up of 24

pipelines and 15 storage terminals. Over 13% of US oil is stored there, with an inbound

and outbound capacity of 6.5 million barrels per day.

NYMEX/COMEX Exchange ADV Report – Monthly Report.

While such comparisons are attention-grabbing they are nonetheless somewhat misleading. They do not account for the fact that futures contracts cover the delivery of oil over an

entire month, not a single day, and that contracts of varying maturity are bought and sold

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�88

Hanieh

While market volume is one indication of the high levels of liquidity and

activity in NYMEX WTI, a more insightful measure is Open Interest (OI). Any

contract in the futures market has two sides, a buyer and seller, and is referred

to as ‘open’ until the contract either expires or the buyer takes an offset position (an opposite position in another contract to cancel out the first one). OI

refers to the number of contracts that are open or active, i.e. the number of

total contracts minus those that have been offset. Higher levels of open interest indicate that additional capital is entering the market, while decreasing

levels of open interest show that money is leaving the market – in this sense,

OI is a more revealing metric than volume for financial involvement in WTI

because it captures the quantities of new money that are flowing into oil

futures and options.96

OI data are reported by the Commodity Futures Trading Commission

(CFTC), an independent US government agency that regulates futures markets such as the NYMEX WTI. Utilising the CFTC’s Commitment of Traders

Report (CoT) – a weekly publication that records levels of OI across different

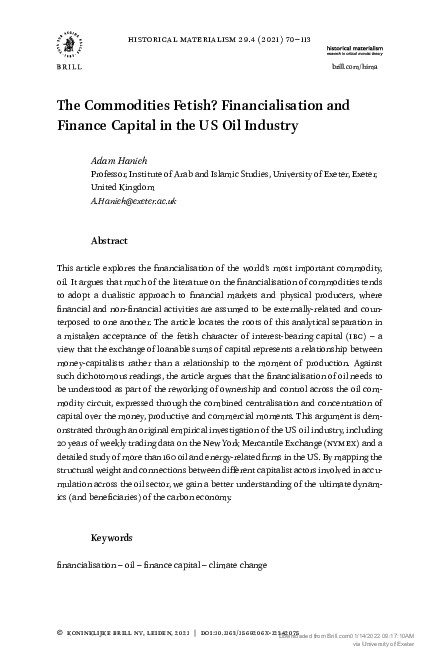

categories of traders and commodities – Figures 1 and 2 present an analysis of

Open Interest in the NYMEX WTI contract (futures and options) since 2000.

The graphs confirm the very significant increase in the size of the oil futures

market over this period, with total OI growing around 375% in the last two

decades. Particularly rapid growth is noticeable between 2003 and 2008, coincident with the commodity price spike of that period. However, total OI has

not dropped since that earlier spike, and figures for 2020 exceeded those of

2008 despite the significant impact of Covid-19 on global oil prices.

The CFTC’s CoT report divides OI into three main categories of market

participants that are shown in Figures 1 and 2. The first of these are labelled

commercial traders, firms that deal directly with physical oil, including producers (such as oil companies), oil traders (those who transport and store

oil), and end-consumers of oil or oil products (such as oil refiners or airlines).

Commercial traders use the futures and options market in order to hedge

against any potential adverse movements in prices, and, through the 1980s and

1990s, they constituted the majority of participants in the oil market. Since

96

in each day’s trading activity. Fundamentally, the problem here is a comparison between

a stock (volume of contracts) and a flow (daily usage). For a discussion of these issues,

see Ripple 2006.

For example, suppose trader A sells a contract to trader B, who, a few hours later, decides

to close their position by selling the same contract on to trader C. The volume of this

sequence would be 2 (two exchanges have taken place) but the OI would be one (only one

contract is open).

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�89

The Commodities Fetish?

Figure 1

Open Interest in NYMEX WTI (futures and options) by Trader Category (2000–20)

Figure 2

Proportion of OI in NYMEX WTI (futures and options) by Trader Category

(2000–20)

Source: Büyükşahin, Haigh, Harris, Overdahl and Robe 2008 for

2000–8 figures; CFTC Weekly CoT Reports for subsequent years

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�90

Hanieh

that time, however, the proportion of OI involving commercial traders has

dropped very significantly, from around 43% in 2000 to 18% in 2020.

The second type of market participants shown in Figures 1 and 2 are swap

dealers.97 Swap dealers are large financial institutions that earn fees through

selling off-exchange derivatives contracts (so-called over-the-counter, or OTC,

derivatives). The customers for these OTC derivatives may be commercial

traders needing to hedge risks around oil price movements, or hedge funds

and other kinds of speculative traders looking to invest in oil beyond the standardised contracts offered on the exchange. Because swap dealers are dealing in a large number of OTC derivatives with a variety of different positions,

there can be a potential net risk to this activity.98 In order to minimise this risk,

swap dealers calculate the aggregate exposure on their off-exchange contracts

and then buy or sell the equivalent (opposite) contracts on NYMEX in order to

maintain a neutral position.99 This on-exchange activity is reflected in Figures 1

and 2, and in 2020 sat at around 30% of total OI. Since 2008, the leading swap

dealers in the oil futures market have been three large US investment banks,

JP Morgan Chase, Goldman Sachs, and Morgan Stanley.100 In 2020, these three

banks held commodity swaps with a total notional value of over $340 billion

between them, far more than any other US bank and making up around 70%

of all commodity swaps held by the ten largest financial holding companies in

the US.101

97

98

99

100

101

Up until 2009, the CoT report included swap dealers in its figures for commercial traders.

Many analysts claimed that this led to a massive overstatement of the commercial category and thus underplayed the impact of speculative activities on the oil price. Following

widespread objection to this so-called ‘swap dealer loophole’, the CFTC began to differentiate these categories from 2009 onwards. For this reason, the data points for 2000–8

are drawn from a table presented by Büyükşahin, Haigh, Harris, Overdahl and Robe 2008,

who had earlier access to granular data from the CFTC. The figures for subsequent years

are calculated by the author from the weekly CoT.

Swap dealers are financial intermediaries who attempt to match buyers and sellers as

much as possible. They will sell derivatives that are both ‘long’ (i.e. sold with the expectation of an increase in price) or ‘short’ (sold with an expectation of a decrease in price).

But if the number of long positions exceeds the number of short positions for a particular

price (or vice versa) then the swap dealer may face a loss.

In other words, it is only the residual net amount left outstanding from the buying and

selling of OTC derivatives that swap dealers need to balance through their trade on

NYMEX. For this reason, the data in Figures 1 and 2 do not actually include the majority

of swap-dealer trade in oil futures (which takes place privately and off-exchange, and is

not subject to CFTC reporting). The data thus significantly understate the overall level of

swap-dealer involvement in oil contracts.

Masters and White 2008.

These figures have been calculated by the author using FR Y-9C forms, consolidated

financial statements that must be submitted by large financial holding companies to the

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

91

The final category of traders shown in Figures 1 and 2 is managed money. As

the name suggests, managed money encompasses those institutions that manage other people’s money and invest in oil contracts with the hope of making

a profit, i.e. institutions that are interested purely in the trade of ‘paper barrels’. Managed money traders are now the dominant actors in NYMEX WTI,

making up more than 50% of total OI in 2020 (up from 20% in 2000). A key

reason for this significant growth is the emergence of managed funds – such as

commodity index funds or Exchange Traded Funds (ETFs) – that are linked to

specific commodity indices and allocate money in commodity futures depending on the movement of those indices.102 Most commodity indexes are heavily skewed towards energy and crude oil in particular (oil, for example, makes

up more than 43% of the leading commodity index, the S&P GSCI),103 and

for this reason, the emergence of these funds has led to a significant increase

in financial flows – mediated by managed money traders – into the NYMEX

WTI market.

There are a large number of financial institutions involved in the managed

money trade.104 These include the same investment banks noted above, who,

in addition to their role as swap dealers, offer ‘services to clients for hedging

and speculative purposes, including commodity investment products [such

102

103

104

US Federal Reserve each quarter. FR Y-9C forms are publicly available from the Federal

Financial Institutions Examination Council, <https://www.ffiec.gov/NPW>.

These funds pool money from thousands of different investors and allocate this capital to

particular investments depending on the movement of an underlying index. In the case

of commodities, the most important of these indices is the S&P GSCI, which tracks 25 different commodities across the energy, metals, agriculture, and livestock sectors. A fund

tracking the S&P GSCI would make investments into these 25 commodities according

to a particular weighting that is periodically reviewed. The allocation of capital through

these funds can be passive, in other words, the distribution of investments is automatically recalibrated depending on the movement of the underlying index; or it can be active,

i.e. determined by fund managers who select investments based upon a variety of (often

proprietary) factors. These funds can entail a high degree of risk and leverage, and the

attempt to ameliorate this risk is a further reason that fund managers are active within

commodity derivative markets.

Revealingly, this index was established in 1991 by Goldman Sachs as the Goldman

Sachs Commodity Index. It was bought by Standard and Poor’s in 2007 and renamed the

S&P GSCI.

The CFTC does not provide public information on the individual financial institutions

that are involved in the swap dealing and managed money activities shown in Figures 1

and 2. However, it is possible to piece together some broad indications of who these institutions are through a variety of other sources, including academic studies, press and

industry reports, the financial statements of banks and other firms, and the formal reporting requirements of large financial holding companies to the US Federal Reserve (e.g. the

FR Y-9C form referred to in footnote 101).

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�92

Hanieh

as ETFs] … they have been also active as proprietary traders speculating on

commodity prices on their own account’.105 It is difficult to provide a precise

empirical estimation of the role of investment banks in these kind of activities,

but Goldman Sachs, Morgan Stanley, and JP Morgan each reported that around

15% of their total trading revenues came from commodity derivatives in 2020

(much more than any other investment bank).106 Alongside these investment

banks, other prominent financial actors within the managed money category

include hedge funds, private equity firms, and asset management companies –

all of whom may trade oil contracts directly or manage investment funds on

behalf of a pool of other investors. Some of these actors are also involved in

‘volatility trading’ – the buying and selling of options aimed at profiting from

large movements in the price of oil.107 Additionally, they may engage in buying and selling OTC derivatives linked to oil, and thus – as major counterparties to the swap dealers noted above – indirectly act to increase the overall OI

on NYMEX.

Taken as a whole, the relative involvement of these three market participants – commercial, swap dealers, and managed money – indicates how much

the oil futures market is driven by so-called non-commercial participants

(managed money and swap dealers) who enter the market in order to trade

(and hopefully profit from) the price movements of ‘paper barrels’. The data

presented in Figures 1 and 2 confirm the considerable growth in the noncommercial categories over the last two decades, which together now represent more than 80% of total OI in oil. These trends are a striking indication

105

106

107

Heumesser and Staritz 2013, p. 23.

Calculated by author from annual financial statements. While these figures are for commodities in general, energy derivatives (mostly for crude oil) make up by far the largest component of total trade in global commodity derivatives (World Federation of

Exchanges 2020, pp. 3, 33).

Volatility traders employ a complex array of strategies that involve the simultaneous

purchase of put and call options (see Schofield 2008). Profit depends on the magnitude

and speed of changes in the price of oil contracts (in either direction) and not on the

price itself and, for this reason, instability can become desirable and extremely lucrative

(e.g. the rapid crash in the price of oil that occurred with the negative pricing of WTI

in April 2020). Due to the significant risks involved in its production and consumption

(geopolitical, environmental and others), oil has an inherent volatility, and in 2007 the

Chicago Board Option Exchange (CBOE) began publishing an index that measures oil

volatility (the Crude Oil Volatility Index, OVX). Since that time, numerous ETFs have been

launched that track the OVX. It is, however, difficult to determine the levels of volatility

trading in oil from publicly-available data, or to identify the precise actors involved in

this kind of speculation. I am indebted to one of the anonymous reviewers of this paper

for highlighting this important issue, which carries numerous intriguing implications in

need of further study.

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�93

The Commodities Fetish?

of oil’s financialisation, i.e. oil has become an object that is traded by financial

institutions, within financial markets, and which is abstracted from its concrete

use value as an essential element of all capitalist commodity production.

5

Mapping Finance Capital across the Oil Commodity Circuit

It is evident that a diverse set of financial actors drives this growth of noncommercial activity in oil futures. These actors include large US investment

banks as well as other kinds of financial institutions who combine asset management, hedge fund, and private equity activities. They may engage directly

in the oil futures market for their own purposes, or trade on behalf of other

clients to whom they offer hedging and investment services. The explosive

growth in the oil futures market over recent decades reflects a market that has

now become dominated by these financial actors; in this sense, the financialisation of oil appears as a phenomenon that has weakened the role and weight

of traditional commercial actors – oil producers, refiners, traders and so forth.

What happens, however, if we reject the kind of commercial/noncommercial dichotomy implicitly adopted in most studies of the financialisation of oil (and in the CFTC data utilised in the preceding section), and consider

the ways in which the large financial institutions driving the dynamics of the

oil futures market are also simultaneously embedded within other moments

of the oil commodity circuit? To this end, Table 1 (see Appendix) examines

nine US-based financial conglomerates that are leading components of the

non-commercial Open Interest captured in Figures 1 and 2 above (i.e. acting

as swap dealers or managed money). Clearly these nine firms are not the only

financial actors active on NYMEX and other commodity markets, but they are

the foremost firms of their kind in the world, and can be considered representative of the broader financial interests driving the growth in oil futures. Given

this fact, Table 1 captures the involvement of these firms in the oil commodity

circuit beyond financial markets – in other words, their direct participation in

the actual production and realisation of oil-as-value, and their integral position as both beneficiaries and drivers of the ‘real-world’ carbon economy.

The conglomerates examined in the table encompass three broad groups of

financial services. The first of these are asset management firms, large financial firms that pool surplus capital from various sources (e.g. wealthy individuals, companies, pensions, or other institutions) and direct this into equities,

bonds, or other investment instruments (including commodities such as oil).

The three firms listed in Table 1 (Vanguard, Blackrock, and State Street) are

the top-ranking asset management firms in the world and collectively control

Historical Materialism 29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�94

Hanieh

more than $15 trillion in assets – around one-third of the total assets held by

the top 20 asset management firms globally, and an amount exceeding China’s

GDP in 2019.108 Usually referred to as the ‘Big Three’, these firms are also among

the largest global managers of commodity index funds and Exchange Traded

Funds – in 2020, ETFs issued by these three firms were estimated to hold more

than 80% of total global ETF assets, including several directly tracking the

movement of commodity futures such as WTI.109

The second group of firms shown in Table 1 are the large investment banks,

JP Morgan, Morgan Stanley, and Goldman Sachs. As noted, these well-known

banks are major financial actors on NYMEX – as the leading swap dealers and

also as money managers and investors in their own right. More generally, these

banks offer a range of investment funds that may be passive or actively managed, and which track a diverse range of equities and bonds across different

sectors, indexes and geographies. In addition to these kinds of portfolio investments, investment banks offer a range of financial services to corporate, individual and government clients. They also typically have specialised units for

private equity, venture capital, or other kinds of direct investment into infrastructure, real estate, or private firms.

The final institutions shown in Table 1 are the three hedge funds/private

equity firms, Blackstone Group, Carlyle Group, and Riverstone Holdings. As

with asset management firms and investment banks, these firms have been

central actors driving the financialisation of oil through their managed money

activities on NYMEX futures. Indeed, many studies of oil futures markets simply describe the non-commercial category of traders (misleadingly) as ‘hedge

funds’. In addition to their hedge fund activities, the three firms listed in the

table control major private equity funds that invest in private (non-listed) firms

with the goal of maximising short-term return – often obtained through taking on high levels of debt and using the target company’s assets as collateral.

Blackstone and Carlyle are the two largest PE firms in the world, controlling

$545 billion and $223 billion of assets in 2020 respectively, while Riverstone

Holdings runs an energy-focused PE fund with $41 billion in assets.

The data in Table 1 (collated in late 2020) must be situated in the context of

a massive boom in US oil production that took place between 2009 and 2014.

With the steady rise in world oil prices over this period, the development of

so-called ‘non-conventional’ oil and gas supplies – reserves that are difficult

and more expensive to extract than conventional fossil fuels – were strongly

incentivised. Of particular relevance here is US shale, crude oil and gas held

108

109

Thinking Ahead Institute 2020, p. 44.

<https://www.etf.com/sections/etf-league-tables/etf-league-table-2020–12–15>.

Historical Materialism

29.4 (2021) 70–113

Downloaded from Brill.com01/14/2022 09:17:10AM

via University of Exeter

�The Commodities Fetish?

95

in shale or sandstone of low permeability that is extracted through fracturing the rock by pressurised liquid (hence the term ‘fracking’). High global oil

prices drove large investments into shale field development between 2009

and 2014, which led to significant improvement in extraction technologies for

these non-conventional supplies. This shale boom was also closely connected

to the deepening financialisation of the US economy following the 2008–9

global financial crash, with the pools of surplus capital generated by policy

responses to the crisis seeking valorisation in the fracking industry as IBC.110

The net result was a major increase in US domestic oil production, which tripled between 2009 and 2014, and propelled the United States into the top rank

of oil producers globally. Remarkably, the US became a net exporter of oil in

early 2011, and overtook Saudi Arabia to become the world’s largest producer

in 2013.

Given this boom in US oil production, how are the nine financial conglomerates shown in Table 1 embedded in the wider commodity circuit – specifically

through the ownership and control of firms involved in development of hydrocarbon reserves, as well as further mid- and downstream activities? In this

respect, Table 1 reveals these conglomerates’ deep involvement with over 160