The weekly debt report provides an update on the debt markets and makes recommendations for investors. It suggests short-term income funds for the current uncertain interest rate environment. Yields on new 10-year government bonds were estimated to trade between 8.60-8.90% for the week. The RBI unexpectedly hiked rates by 25 basis points. Wholesale inflation declined to a 5-month low of 6.16% in December. Deposit growth continues to outpace credit growth in the banking system.

The weekly debt report provides an update on the debt markets and makes recommendations for investors. It suggests short-term income funds for the current uncertain interest rate environment. Yields on new 10-year government bonds were estimated to trade between 8.60-8.90% for the week. The RBI unexpectedly hiked rates by 25 basis points. Wholesale inflation declined to a 5-month low of 6.16% in December. Deposit growth continues to outpace credit growth in the banking system.

The weekly debt report provides an update on the debt markets and makes recommendations for investors. It suggests short-term income funds for the current uncertain interest rate environment. Yields on new 10-year government bonds were estimated to trade between 8.60-8.90% for the week. The RBI unexpectedly hiked rates by 25 basis points. Wholesale inflation declined to a 5-month low of 6.16% in December. Deposit growth continues to outpace credit growth in the banking system.

The weekly debt report provides an update on the debt markets and makes recommendations for investors. It suggests short-term income funds for the current uncertain interest rate environment. Yields on new 10-year government bonds were estimated to trade between 8.60-8.90% for the week. The RBI unexpectedly hiked rates by 25 basis points. Wholesale inflation declined to a 5-month low of 6.16% in December. Deposit growth continues to outpace credit growth in the banking system.

Strategy recommended: Given the present scenario of uncertainty on the direction of the interest rate movement, short term income funds with 2-3 years Average Maturity may be the right bet for any kind of investors while the investors who wish to stay invested for more than 18 months or two years may consider Income, Dynamic Income funds and Gilt funds (although with reduced expectations). Selective Dynamic funds which are managed actively can be suitable for medium term say for 6-12 months. Investors those who do not want MTM risk can choose Ultra Short term funds as they are low risk low return products. Outlook for the week:

We feel that the new 10-year G Sec yields could trade in the 8.60% - 8.90% band for the week. G Sec:

Indian bond markets saw yields inching up during the week ended Jan 31, 2014. G sec market opened the week on a cautious note tracking considerable weakness in the domestic currency and also amidst some caution ahead of the monetary policy review scheduled for next day.

The RBI surprised the market by hiking 25 bps in policy rates at its third quarter review of monetary policy on Tuesday. Gilt prices ended lower during the day. Gilt prices ended down on Wednesday on caution ahead of the outcome of the US FOMC meeting.

Prices of the G sec ended lower on Thursday tracking further tapering announced by the FOMC at its meeting and its resultant negative impact on the domestic currency. The apprehension over the G-Sec auction scheduled for the week also dampened the market. Prices of the gilts ended higher on Friday due to better than expected demand at the RBIs weekly gilt auction.

Hence, the yields of the new 10 year benchmark G Sec 8.83% GS 2023 ended higher by 3 bps at 8.77% (Rs. 100.37) on Friday in comparison to the previous weeks close of 8.74%.

Weekly Debt Report

Retail Research

Debt Market Update

contd

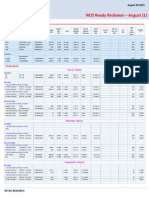

Change in the values of debt benchmarks and securities during the week:

Third Quarter Review of Monetary Policy for 2013-14:

The RBI has surprised the market by hiking 25 bps in Repo rate at its Third Quarter Review of Monetary Policy for 2013-14 especially to bring down inflation by a substantial margin. The LAF Reverse Repo Rate was accordingly adjusted to 7.00%. The rate on Marginal Standing Facility was also hiked to 9%. Further, the RBI has set the disinflationary target for headline CPI at 8% by January 2015 and 6% by January 2016. T bill Auction:

The T-Bill auctions held last week were fully subscribed. The cut-off for 91-Days T-Bill was set at Rs 97.83, implying a yield of 8.9% (previous week yield 8.69%). The cut-off for 182-Days T-Bill was set at Rs 95.73, implying a yield of 8.95%. The central bank announced the sale of 91 Day T-Bill (for Rs. 4,000 crore) and 364 Day T-bill (for Rs. 3,000 crore) on 5 Feb. Liquidity, Call & CBLO:

The systemic liquidity in the banking system saw marginally improvement compared to the last week due to

government spending. The net infusion from the LAF window was a daily average of Rs. 34,347 crore for last week (Rs. 36,660 crore in previous week). The inter bank call rates hovered around 8.35% levels on Friday. The CBLO rates were positioned at 8% level.

Weekly Debt Report

Retail Research

Debt Market Update

contd

Gilt Securities Yields Movements in last 4 weeks :

Currency:

The USD appreciated against the Euro by 1.42% for the week ended 31st January 2014.

The dollar depreciated against the yen by 0.09%.

The USD appreciated against the Pound by 0.36% . Change in CD Rates:

Weekly Debt Report

Retail Research

Debt Market Update

contd

Change in CP Rates:

Commodity price Changes:

Gold & Crude oil:

International crude oil prices (WTI) ended higher by 0.88% for the week ended 31st January 2014 . International gold prices fell by 1.94% for the week ended 31st January 2014 . Forthcoming Auctions:

Corporate Bonds:

The 1 year bond ended at 9.7% compared to the previous week close of 9.55%. The 10-year AAA bond traded at 9.6% compared to the previous week close 9.52%. Weekly Debt Report

Retail Research

Debt Market Update

contd

Global Updates: India:

Indias foreign exchange reserves inch higher to $292.24 bn as of Jan 24, from $292.08 bn in the earlier week. Indias fiscal deficit reached $82 bn during April-December, or 95.2% of the full year target, compared with 78.8% a year earlier.

IRDA indefinitely defers provisions in its Standard Proposal Form for Life Insurance after getting critical comments on it.

India's drug regulator orders Ranbaxy to furnish a comprehensive explanation for the violation of manufacturing practices at its Toansa plant.

IRDA unveils simplified standard products to be sold by life insurance companies through Common Services Centers to increase insurance penetration in rural markets.

RBI Governor Raghuram Rajan says the withdrawal of pre-2005 notes is not intended to check black money but to prevent counterfeiting.

SEBI Chairman says that the regulator will shortly come out with a long term policy for the mutual fund industry which will help deepen the penetration of the industry into non metro markets.

Government collects Rs.60cr by selling Inflation Indexed National Savings Securities or retail inflation bonds. Asia:

China official non-manufacturing PMI fell to 53.4 in January from 54.6 in December. Japan's core consumer prices rose 1.3% in December from a year earlier, following a 1.2% gain in November. Singapore's Ministry of Manpower (MoM) says unemployment remained low at a seasonally adjusted 1.8% in the December quarter, and was unchanged from the third quarter.

Chinas industrial profits in December rose 6% to 942.5 bn yuan from a year earlier. Weekly Debt Report

Retail Research

Debt Market Update

contd

US:

US existing home sales rose 1% in December to a seasonally adjusted 4.87 mn units, compared with 4.82 mn units in November.

US personal consumption rose a seasonally adjusted 0.4% in December compared to November's revised spending growth of 0.6%; personal income was however virtually unchanged in December.

US Chicago PMI dropped to 59.6 in January, down from a revised reading of 60.8 in December. US University of Michigan Consumer Sentiment index slipped to 81.2 in January, down from the 82.5 posted in December.

US employment cost index rose to a seasonally adjusted 0.5% in the fourth quarter of 2013 compared to 0.4% in the preceding quarter.

US durable goods orders declined 4.3% in December compared with a revised 2.6% gain in November. US Pending Home Sales index dropped sharply to 92.4 in December, down 8.7% from a downwardly revised 101.2 in November UK: UK net consumer credit rose by 2.3bn pounds in December, up from a revised 1.8bn pounds in November.

UKs GDP rose 0.7% in the Q4 2013 as compared to 0.8% growth in previous quarter; on a yearly basis, GDP grew 2.8% in Q4. Euro Zone:

European Central Bank leaves its key interest rates unchanged at 0.25% for a second straight month. The Eurozone CPI slipped in January to 0.7% compared to 0.8% in December. The Eurozone unemployment rate fell slightly to 10.7% in December from 10.8% a month earlier. Eurozone consumer confidence rose to -11.7 in January from -13.5 in December. Weekly Debt Report

Retail Research

Debt Market Update

contd

Economic Calendar:

Weekly Debt Report

Retail Research

Debt Market Update

contd

US Dollar Vs Indian Rupee

Relationship among policy rates and benchmarks

The US dollar appreciated against the rupee by 0.48% for the week ended 31st January 2014. The rupee fell on worries of foreign outflows as the US Federal Reserve further cut its monetary stimulus while government data showed that fiscal deficit in the first three quarters inched closer to the budgeted target for the year. The rupee closed largely flat on the week, following a sharp fall in the previous week, which was its worst since the week it hit a record low at the end of August.

The RBI surprised the market by hiking 25 bps in Repo rate at its Third Quarter Review of Monetary Policy for 2013-14 especially to bring down inflation by a substantial margin. Essence of the Patel Committee report has found its place in the RBI's objectives. However, higher rates can make the currency more attractive for foreign investors, too much tightening can dent economic growth, eroding confidence, and in turn hit stocks.

WPI Inflation (YoY)

Wholesale inflation declined to a five-month low of 6.16% in December.

Inflation in food articles was 13.68% in Dec as against 19.93% in the preceding month, according to the WPI data released. Inflation in Nov was 7.52% and in Oct, it was revised upward to 7.24% from 7%.

Weekly Debt Report

Deposit vs. Advance Growth (YoY)%

Deposit growth in the banking system continued to outpace non-food credit

growth in the banking system, according to latest data from the Reserve Bank of India (RBI). For the fortnight ended January 10, deposits grew by 15.56% year-on-year to Rs.7,549,039 crore. Non-food credit growth for the fortnight improved marginally from the previous fortnight to 15.02% y-o-y to Rs.56,76,215.

Retail Research

10

Debt Market Update

contd

Money Stock (M3) (YoY) (%)

Corporate Spread vs. 10Y G Sec Yield

Money Supply M3 in India increased to 92847.75 INR Billion in January of

2014 from 92063.80 INR Billion in December of 2013. Money Supply M3 in India is reported by the Reserve Bank of India. Money Supply M3 in India averaged 14758.59 INR Billion from 1972 until 2014, reaching an all time high of 92847.75 INR Billion in January of 2014.

Foreign Exchange Reserves (mn of USD)

Net injection through LAF window (Crs. Rs)

Indias fiscal deficit reached $82 bn during April-December, or 95.2% of the

full year target, compared with 78.8% a year earlier.

Weekly Debt Report

Corporate bond Yields saw a rise during last week. The one year AAA credit spreads rose by 3 basis points while 5 year spread rose by 2 basis points.

The systemic liquidity in the banking system saw marginally improved compared to the last week due to government spending. The net infusion from the LAF window was a daily average of Rs. 34,347 crore for last week (Rs. 36,660 crore in previous week). The inter bank call rates hovered around 8.35% levels on Friday. The CBLO rates were positioned at 8% level.

Retail Research

11

Debt Market Update

MFs net investment in Debt (Rs Crs):

Certificates of Deposit (%)

Mutual funds had been net buyers in December month to the tune of Rs. 40,882 crore while they have remained net buyers in the January month to the tune of Rs. 43,115 crore.

FIIs net investment in Debt (Rs Crs):

Commercial Paper (%)

FII bought net of Rs. 9,696 crore during December month while they have bought debt securities in January to the net of Rs. 12,665 crore.

Weekly Debt Report

CD rates saw inching up in the last one week period. The CD rates hovered around 9.7% level (as per the latest data) (one year CD).

Rates of Commercial papers also traded higher in the last one week. The CP rates are hovering around 10.15% level (one year maturity CP).

Retail Research

12

Debt Market Update

Analyst: Dhuraivel Gunasekaran.

HDFC Securities Limited, I Think Techno Campus, Bulding B, Alpha, Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone (022) 30753400 Fax: (022) 30753435 Disclaimer: Mutual Fund investments are subject to risk. Past performance is no guarantee for future performance. This document has been prepared by HDFC Securities Limited and is meant for sole use by the recipient and not for circulation. This document is not to be reported or copied or made available to others. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. The information contained herein is from sources believed reliable. We do not represent that it is accurate or complete and it should not be relied upon as such. We may have from time to time positions or options on, and buy and sell securities referred to herein. We may from time to time solicit from, or perform investment banking, or other services for, any company mentioned in this document. This report is intended for non-Institutional Clients Weekly Debt Report