0% found this document useful (0 votes)

206 viewsConstant Correlation Model

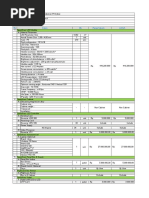

This document describes a constant correlation model for analyzing stock return data. It calculates the correlation between stock returns, computes necessary metrics like average returns and standard deviations, and uses these values to create covariance and expected return matrices. It then calculates efficient portfolios with and without short sales allowed by solving these matrices. The document generates a plot comparing the individual stocks to the efficient portfolios.

Uploaded by

api-285777244Copyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

206 viewsConstant Correlation Model

This document describes a constant correlation model for analyzing stock return data. It calculates the correlation between stock returns, computes necessary metrics like average returns and standard deviations, and uses these values to create covariance and expected return matrices. It then calculates efficient portfolios with and without short sales allowed by solving these matrices. The document generates a plot comparing the individual stocks to the efficient portfolios.

Uploaded by

api-285777244Copyright

© © All Rights Reserved

Available Formats

Download as PDF, TXT or read online on Scribd

/ 3