0% found this document useful (0 votes)

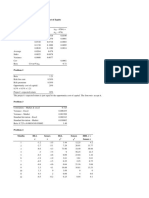

33 viewsCell Name Original Value Final Value: Target Cell (Min) $E$11 Portfolio Risk Risk2 0.10533666855 0.1053366685

The document appears to be an Excel output report containing information about portfolio optimization. It includes the target portfolio risk of 0.1053366685, the original and final weights of two assets, portfolio constraints, sensitivity analysis results and limits testing. The report examines adjusting weights to minimize risk while meeting return and constraint requirements.

Uploaded by

protonkartikCopyright

© Attribution Non-Commercial (BY-NC)

Available Formats

Download as XLSX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

33 viewsCell Name Original Value Final Value: Target Cell (Min) $E$11 Portfolio Risk Risk2 0.10533666855 0.1053366685

The document appears to be an Excel output report containing information about portfolio optimization. It includes the target portfolio risk of 0.1053366685, the original and final weights of two assets, portfolio constraints, sensitivity analysis results and limits testing. The report examines adjusting weights to minimize risk while meeting return and constraint requirements.

Uploaded by

protonkartikCopyright

© Attribution Non-Commercial (BY-NC)

Available Formats

Download as XLSX, PDF, TXT or read online on Scribd

/ 10