Internal Credit Risk Rating Model by Badar-E-Munir

Internal Credit Risk Rating Model by Badar-E-Munir

Download as pdf or txt

At a glance

Powered by AI

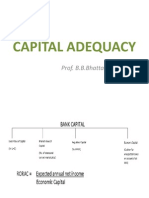

The document discusses developing internal credit risk rating systems using both qualitative and quantitative techniques.

Some credit risk assessment models discussed include heuristic models, qualitative systems, and hybrid forms.

Some credit scoring models discussed include traditional ratio analysis and discriminant analysis.

You might also like

- Low Default Portfolios: A Proposal For Conservative Estimation of Default ProbabilitiesDocument31 pagesLow Default Portfolios: A Proposal For Conservative Estimation of Default ProbabilitiesandreNo ratings yet

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsFrom EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNo ratings yet

- Comparison of Modeling Methods For Loss Given DefaultDocument14 pagesComparison of Modeling Methods For Loss Given DefaultAnnNo ratings yet

- Credit Risk PolicyDocument32 pagesCredit Risk PolicyRajib Ranjan Samal100% (1)

- ICRRS Guidelines - BB - Version 2.0Document25 pagesICRRS Guidelines - BB - Version 2.0Optimistic EyeNo ratings yet

- Guide To Credit Scoring 2000 PDFDocument15 pagesGuide To Credit Scoring 2000 PDFFocus ManNo ratings yet

- Stress TestingDocument32 pagesStress TestingTarikul Islam100% (1)

- Review: Normal DistributionDocument46 pagesReview: Normal DistributionAaron HayyatNo ratings yet

- Reliability Study Sil Evaluation: Calculation NoteDocument5 pagesReliability Study Sil Evaluation: Calculation Notekenoly12392% (12)

- CREDIT RISK GRADING MANUAL BangladeshDocument45 pagesCREDIT RISK GRADING MANUAL BangladeshIstiak Ahmed100% (2)

- Avi Thesis Final Credit Risk Management in Sonali Bank LTDDocument20 pagesAvi Thesis Final Credit Risk Management in Sonali Bank LTDHAFIZA AKTHER KHANAMNo ratings yet

- Credit Risk Grading-Apex TanneryDocument21 pagesCredit Risk Grading-Apex TanneryAbdullahAlNomunNo ratings yet

- Credit Risk Assessment: The New Lending System for Borrowers, Lenders, and InvestorsFrom EverandCredit Risk Assessment: The New Lending System for Borrowers, Lenders, and InvestorsNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- Credit Worthiness: What Is A Corporate Credit RatingDocument23 pagesCredit Worthiness: What Is A Corporate Credit RatingSudarshan ChitlangiaNo ratings yet

- Credit Risk ManagementDocument24 pagesCredit Risk ManagementAl-Imran Bin Khodadad100% (2)

- Credit & Risk PolicyDocument14 pagesCredit & Risk PolicySaran Saru100% (2)

- Basel IiiDocument32 pagesBasel Iiivenkatesh pkNo ratings yet

- ICAAP - DeereDocument12 pagesICAAP - DeereSumiran BansalNo ratings yet

- Excel and Exceed Basel-IIDocument20 pagesExcel and Exceed Basel-IIHaris AliNo ratings yet

- Credit Policy Version 1.2Document157 pagesCredit Policy Version 1.2Amit Singh100% (1)

- Dissertation Main - Risk Management in BanksDocument87 pagesDissertation Main - Risk Management in Banksjesenku100% (1)

- ALCO and Operational Risk Management at Bank of ChinaDocument17 pagesALCO and Operational Risk Management at Bank of ChinaAbrar100% (1)

- Product Development: - Loan Pricing Product Development: - Loan PricingDocument55 pagesProduct Development: - Loan Pricing Product Development: - Loan PricingBriju RebiNo ratings yet

- Capital Adequacy Mms 2011Document121 pagesCapital Adequacy Mms 2011Aishwary KhandelwalNo ratings yet

- Bank-Loan Loss Given DefaultDocument24 pagesBank-Loan Loss Given Defaultvidovdan9852100% (1)

- Implementation of Risk Based SupervisionDocument120 pagesImplementation of Risk Based SupervisionandriNo ratings yet

- Credit Risk Mgmt. at ICICIDocument60 pagesCredit Risk Mgmt. at ICICIRikesh Daliya100% (1)

- Guidance Note On Credit RiskDocument50 pagesGuidance Note On Credit RiskRaj KothariNo ratings yet

- Rbs & Risk Based Internal Audit 22122022Document73 pagesRbs & Risk Based Internal Audit 22122022Sunny Kumar GuptaNo ratings yet

- Credit Policy 2006Document100 pagesCredit Policy 2006natashamalhotraNo ratings yet

- KYC Passing Rate Data Analysis Using Feature Engineering Clustering and Data VisualizationDocument56 pagesKYC Passing Rate Data Analysis Using Feature Engineering Clustering and Data VisualizationSIDDESH SANNA GOWDRUNo ratings yet

- Stress Testing Credit RiskDocument44 pagesStress Testing Credit RiskG117No ratings yet

- Updated Loan Policy To Board 31.03.2012 Sent To Ro & ZoDocument187 pagesUpdated Loan Policy To Board 31.03.2012 Sent To Ro & ZoAbhishek BoseNo ratings yet

- Components of A Sound Credit Risk Management ProgramDocument8 pagesComponents of A Sound Credit Risk Management ProgramArslan AshfaqNo ratings yet

- Credit Policy ManualKASBDocument199 pagesCredit Policy ManualKASBcybersonicpk100% (2)

- Asset Liability ManagementDocument79 pagesAsset Liability ManagementSiddhartha Yadav100% (1)

- Bsp-Credit Risk ManagementDocument69 pagesBsp-Credit Risk Managementjhomar jadulanNo ratings yet

- Credit Risk ModelingDocument4 pagesCredit Risk ModelingmohamedciaNo ratings yet

- Credit Policy GuidelinesDocument4 pagesCredit Policy Guidelinesnazmul099No ratings yet

- Credit Policy - Due Diligence: EpathshalaDocument9 pagesCredit Policy - Due Diligence: EpathshalaAjay Singh Phogat100% (1)

- Strategic Credit Management - IntroductionDocument14 pagesStrategic Credit Management - IntroductionDr VIRUPAKSHA GOUD G50% (2)

- Credit Risk Management-ReportDocument11 pagesCredit Risk Management-ReportNazuk DilNo ratings yet

- Credit Appraisal and Risk Rating at PNBDocument87 pagesCredit Appraisal and Risk Rating at PNBVishnu Soni100% (2)

- Evaluation of Credit RiskDocument16 pagesEvaluation of Credit RiskriskaNo ratings yet

- Axis Bank ORDocument21 pagesAxis Bank ORDas SanghamitraNo ratings yet

- Booklet Toolbox Basel4Document74 pagesBooklet Toolbox Basel4Rahajeng PramestiNo ratings yet

- BankingDocument110 pagesBankingNarcity UzumakiNo ratings yet

- Lehman Brothers ICAAPDocument113 pagesLehman Brothers ICAAPKirill TimoshenkoNo ratings yet

- Credit Risk ManagementDocument3 pagesCredit Risk Managementamrut_bNo ratings yet

- Credit Risk Analysis PDFDocument300 pagesCredit Risk Analysis PDFraj kumarNo ratings yet

- Credit Risk ManagementDocument16 pagesCredit Risk Managementkrishnalohia9No ratings yet

- Asset Liability Management in BanksDocument36 pagesAsset Liability Management in BanksHoàng Trần HữuNo ratings yet

- Overview of Lending Activity: by Dr. Ashok K. DubeyDocument19 pagesOverview of Lending Activity: by Dr. Ashok K. DubeySmitha R AcharyaNo ratings yet

- Loan SyndicationDocument4 pagesLoan SyndicationRalsha DinoopNo ratings yet

- Evaluating Credit Risk and Loan Performance in Online Peer To Peer P2P LendingDocument18 pagesEvaluating Credit Risk and Loan Performance in Online Peer To Peer P2P LendingFUDANI MANISHANo ratings yet

- Model Management Guidance PDFDocument70 pagesModel Management Guidance PDFChen CharlesNo ratings yet

- Ilaap Guidelines1Document20 pagesIlaap Guidelines1geminiNo ratings yet

- Credit Appraisal ProcessDocument43 pagesCredit Appraisal ProcessAbhinav Singh100% (1)

- Financing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesFrom EverandFinancing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesNo ratings yet

- EENG 428 Course DescriptionDocument3 pagesEENG 428 Course DescriptionGrace Anne BedionesNo ratings yet

- STATISTICDocument23 pagesSTATISTICnur ainun arsyadNo ratings yet

- Master Thesis Panteleimon VrachasDocument235 pagesMaster Thesis Panteleimon VrachasqweNo ratings yet

- Accounting For P-DeltaDocument1 pageAccounting For P-DeltademetrisNo ratings yet

- Summative and Performance Test Q1 No.1Document15 pagesSummative and Performance Test Q1 No.1Rosendo AqueNo ratings yet

- JOHOR STPM Mathematics T P3 Trial 2020 QDocument3 pagesJOHOR STPM Mathematics T P3 Trial 2020 QQuah En YaoNo ratings yet

- Current Pillar DesignDocument24 pagesCurrent Pillar DesignjmgumbwaNo ratings yet

- Unit 1 - How To Access The Portal & Assignment - 00Document4 pagesUnit 1 - How To Access The Portal & Assignment - 00MR. DEVASHISH GAUTAMNo ratings yet

- SPWM V/HZ InverterDocument51 pagesSPWM V/HZ InverterLabi BajracharyaNo ratings yet

- Lab Manual 1 Flow Chart Repaired)Document9 pagesLab Manual 1 Flow Chart Repaired)irfan_chand_mianNo ratings yet

- Rms Energy FilterDocument5 pagesRms Energy FilterHimanshu SaxenaNo ratings yet

- Cetol PDFDocument34 pagesCetol PDFpalani100% (1)

- Bibliography On Cyclostationarity: Erchin Serpedin, Flaviu Panduru, Ilkay Sarı, Georgios B. GiannakisDocument71 pagesBibliography On Cyclostationarity: Erchin Serpedin, Flaviu Panduru, Ilkay Sarı, Georgios B. Giannakisbobyys990No ratings yet

- Udacity Homework AnswersDocument8 pagesUdacity Homework Answerseltklmfng100% (1)

- Sarala Birla Public School: Assignment - 1 (2022-23) Class: ViiiDocument2 pagesSarala Birla Public School: Assignment - 1 (2022-23) Class: Viiiramesh kumarNo ratings yet

- InvolutesDocument13 pagesInvolutesjeelaniNo ratings yet

- Horizontal Well PerformanceDocument25 pagesHorizontal Well PerformanceGaurav KunduNo ratings yet

- Roger PenroseDocument10 pagesRoger PenroseRenz MendozaNo ratings yet

- PM FM 5Document2 pagesPM FM 5biloma6323No ratings yet

- Ideal Flow Traffic Analysis: A Case Study On A Campus Road NetworkDocument12 pagesIdeal Flow Traffic Analysis: A Case Study On A Campus Road NetworkDiana SeguiNo ratings yet

- Ge6152 Engineering Graphics Reg2013 QBDocument16 pagesGe6152 Engineering Graphics Reg2013 QBKarthik GanesanNo ratings yet

- Significance of Diagrams and GraphsDocument2 pagesSignificance of Diagrams and GraphsHarsh ThakurNo ratings yet

- Reflection: Saint Michael College Cantilan, Surigao Del SurDocument1 pageReflection: Saint Michael College Cantilan, Surigao Del SurFrancis Miguel PetrosNo ratings yet

- Resonance Class IntermediateDocument3 pagesResonance Class IntermediateSahil KambleNo ratings yet

- Design Challenges of Reciprocal Frame Structures in Architecture 2019Document16 pagesDesign Challenges of Reciprocal Frame Structures in Architecture 2019delaxoNo ratings yet

- Integration in Finite Terms - Maxwell RosenlichtDocument11 pagesIntegration in Finite Terms - Maxwell RosenlichtAshish Kumar100% (1)

- Lecture 10Document76 pagesLecture 10kings accountNo ratings yet

- 2nd COT - Numeracy SkillsDocument3 pages2nd COT - Numeracy SkillsRosie GualvezNo ratings yet