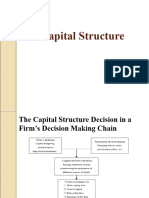

Capital Structure: Definition: Capital Structure Is The Mix of Financial Securities Used To Finance The Firm

Capital Structure: Definition: Capital Structure Is The Mix of Financial Securities Used To Finance The Firm

Download as docx, pdf, or txt

You might also like

- Memorandum of AgreementDocument4 pagesMemorandum of AgreementAldrinmarkquintana80% (10)

- Vantiv Worldpay Confidential Information Memorandum Sep 7Document49 pagesVantiv Worldpay Confidential Information Memorandum Sep 7AlexNo ratings yet

- Capital Structure and LeverageDocument31 pagesCapital Structure and Leveragealokshri25No ratings yet

- Financial Management:: Firms and The Financial MarketDocument54 pagesFinancial Management:: Firms and The Financial Marketsiti aubreyNo ratings yet

- FM S5 Capitalstructure TheoriesDocument36 pagesFM S5 Capitalstructure TheoriesSunny RajoraNo ratings yet

- FM Sheet 4 (JUHI RAJWANI)Document8 pagesFM Sheet 4 (JUHI RAJWANI)Mukesh SinghNo ratings yet

- Financial Management: 1st Theory of Capital StructureDocument7 pagesFinancial Management: 1st Theory of Capital StructureYash AgarwalNo ratings yet

- 1Document5 pages1Pradip AwariNo ratings yet

- Capital StructureDocument55 pagesCapital Structurekartik avhadNo ratings yet

- FM Capital Structure TheoryDocument6 pagesFM Capital Structure Theoryjabeenbegum916No ratings yet

- FM Unit 2Document24 pagesFM Unit 2KarishmaNo ratings yet

- FinanceDocument6 pagesFinanceshrestharupesh808No ratings yet

- Capital StructureDocument4 pagesCapital StructureAdeem Ashrafi100% (2)

- Capital Structure DecisionDocument10 pagesCapital Structure DecisionMunni FoyshalNo ratings yet

- Capital Structure TheoryDocument10 pagesCapital Structure TheoryMd. Nazmul Kabir100% (1)

- Chapter 2 - CompleteDocument29 pagesChapter 2 - Completemohsin razaNo ratings yet

- What Does Capital Structure Mean?Document4 pagesWhat Does Capital Structure Mean?anaqshabbirNo ratings yet

- Capital StructureDocument23 pagesCapital StructureDrishti BhushanNo ratings yet

- Capital Structure Planning: Unit: 3Document46 pagesCapital Structure Planning: Unit: 3Shaifali ChauhanNo ratings yet

- Capital Structure and Firm ValueDocument39 pagesCapital Structure and Firm ValueIndrajeet KoleNo ratings yet

- BBACO302 FMRA ModuleDocument33 pagesBBACO302 FMRA Modulepriyanka.barman.10.aNo ratings yet

- Cost of CapitalDocument16 pagesCost of CapitalBabar AdeebNo ratings yet

- CH 5Document10 pagesCH 5malo baNo ratings yet

- Capital Structure Decision Is Important For A Firm BecauseDocument9 pagesCapital Structure Decision Is Important For A Firm BecauseAditya RathiNo ratings yet

- Mba NotesDocument12 pagesMba NotesSrishtiNo ratings yet

- Capital Structure Theory and PolicyDocument11 pagesCapital Structure Theory and PolicypreetiNo ratings yet

- Capital Structure: Meaning of Capital Structure Theories of Capital StructureDocument21 pagesCapital Structure: Meaning of Capital Structure Theories of Capital Structureashanil07No ratings yet

- Corp Finance Group One Course Work (Final)Document27 pagesCorp Finance Group One Course Work (Final)jonas sserumagaNo ratings yet

- Cost of CapitalDocument13 pagesCost of CapitalManvendra ShahiNo ratings yet

- Our ProjectDocument7 pagesOur ProjectYoussef samirNo ratings yet

- Unit 3rd Financial Management BBA 4thDocument18 pagesUnit 3rd Financial Management BBA 4thYashfeen FalakNo ratings yet

- Mba Corporate FinanceDocument13 pagesMba Corporate FinanceAbhishek chandegraNo ratings yet

- FM THEORYDocument17 pagesFM THEORYaryank281103No ratings yet

- Capital Structure TheoriesDocument26 pagesCapital Structure Theoriesprajii100% (1)

- Cap Stru and Div DeciDocument19 pagesCap Stru and Div DecimuddiniNo ratings yet

- Financial ManagementDocument8 pagesFinancial Managementpankaj91834No ratings yet

- Notes of Corporate Finance: BBA 8th SemesterDocument10 pagesNotes of Corporate Finance: BBA 8th SemesterÀmc ChaudharyNo ratings yet

- InvestopidiaDocument18 pagesInvestopidiatinasoni11No ratings yet

- Unit Iv: Financing DecisionsDocument11 pagesUnit Iv: Financing DecisionsAR Ananth Rohith BhatNo ratings yet

- Capital StructureDocument28 pagesCapital Structureluvnica6348No ratings yet

- Advance Financial ManagementDocument62 pagesAdvance Financial ManagementKaneNo ratings yet

- Corporate Finance: Capital Structure in ISPAT IndustriesDocument28 pagesCorporate Finance: Capital Structure in ISPAT IndustriesGautam KhantwalNo ratings yet

- Hypothetical Capital Structure and Cost of Capital of Mahindra Finance Services LTDDocument25 pagesHypothetical Capital Structure and Cost of Capital of Mahindra Finance Services LTDlovels_agrawal6313No ratings yet

- Chapter 18 - ShanaDocument8 pagesChapter 18 - ShanaHanz SadiaNo ratings yet

- Financial ManagementDocument25 pagesFinancial ManagementNespinNo ratings yet

- Chaitanya Chemicals - Capital Structure - 2018Document82 pagesChaitanya Chemicals - Capital Structure - 2018maheshfbNo ratings yet

- CF Assignment - Capital Structure - FreshDocument3 pagesCF Assignment - Capital Structure - Freshganesh gowthamNo ratings yet

- Capital StructureDocument4 pagesCapital Structureharish chandraNo ratings yet

- Capitasl Expenditure (Final Project)Document42 pagesCapitasl Expenditure (Final Project)nikhil_jbp100% (1)

- Capital Structure: Meaning and Theories Presented by Namrata Deb 1 PGDBMDocument20 pagesCapital Structure: Meaning and Theories Presented by Namrata Deb 1 PGDBMDhiraj SharmaNo ratings yet

- Study MaterialDocument17 pagesStudy MaterialRohit KumarNo ratings yet

- Corporate Finance - Unit 3 NotesDocument6 pagesCorporate Finance - Unit 3 Notesfatimafirdaus147No ratings yet

- University of Central Punjab: F 2020 Course Title: Financial Strategy Course Code: IVA5833Document8 pagesUniversity of Central Punjab: F 2020 Course Title: Financial Strategy Course Code: IVA5833Ayesha HamidNo ratings yet

- Advanced Financial ManagementDocument23 pagesAdvanced Financial ManagementDhaval Lagwankar75% (4)

- LONG QUESTIONSDocument12 pagesLONG QUESTIONSnancymcdonie1204No ratings yet

- A Study On Capital Structure in Sri Pathi Paper and Boards Pvt. LTD., SivakasiDocument69 pagesA Study On Capital Structure in Sri Pathi Paper and Boards Pvt. LTD., SivakasiGold Gold50% (4)

- FM Capital StructureDocument5 pagesFM Capital Structuremugojulius671No ratings yet

- Capital Structure: Compiled To Fulfill The Duties of Financial Management Courses Lecturer: Prof. Dr. Isti Fadah, M.SiDocument10 pagesCapital Structure: Compiled To Fulfill The Duties of Financial Management Courses Lecturer: Prof. Dr. Isti Fadah, M.SiGaluh DewandaruNo ratings yet

- Financial Mmanagement II -Chapter 1Document49 pagesFinancial Mmanagement II -Chapter 1zelalemabirhamNo ratings yet

- Analytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationFrom EverandAnalytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Mutual FundDocument20 pagesMutual FundArun Nair100% (1)

- Bancassurance: An Indian PerspectiveDocument17 pagesBancassurance: An Indian Perspectivealmeidabrijet100% (1)

- Cash ManageentDocument6 pagesCash ManageentArun NairNo ratings yet

- Management of Sick IndustriesDocument15 pagesManagement of Sick IndustriesArun NairNo ratings yet

- Financial Accounting Mock Test PaperDocument7 pagesFinancial Accounting Mock Test PaperBharathFrnzbookNo ratings yet

- Payment of Gratuity As Per UAE Labour Law: Konkan TimesDocument4 pagesPayment of Gratuity As Per UAE Labour Law: Konkan TimesAdarsh SvNo ratings yet

- Notice: Grants and Cooperative Agreements Availability, Etc.: Rural Industrialization Loan and Grant Program Compliance Certification RequestsDocument2 pagesNotice: Grants and Cooperative Agreements Availability, Etc.: Rural Industrialization Loan and Grant Program Compliance Certification RequestsJustia.comNo ratings yet

- Spa Psslai and AfpslaiDocument1 pageSpa Psslai and Afpslaijci028No ratings yet

- Audit ChecklistDocument46 pagesAudit ChecklistCA Gourav Jashnani67% (3)

- Chapter 18, Modern Advanced Accounting-Review Q & ExrDocument23 pagesChapter 18, Modern Advanced Accounting-Review Q & Exrrlg4814100% (3)

- General Questions: View AnswerDocument4 pagesGeneral Questions: View AnswerVINAY MISHRANo ratings yet

- Agency PaperDocument13 pagesAgency Paperapi-272668024No ratings yet

- Annuities Practice Problem Set 2: Future Value of An AnnuityDocument2 pagesAnnuities Practice Problem Set 2: Future Value of An AnnuityJeric Marasigan EnriquezNo ratings yet

- CFO or Treasurer or Project Manager or ConsultantDocument3 pagesCFO or Treasurer or Project Manager or Consultantapi-121384723No ratings yet

- Keynote SpeechDocument21 pagesKeynote SpeechADBI EventsNo ratings yet

- RPMS AHGElumbaringDocument4 pagesRPMS AHGElumbaringHomil Homil HomilNo ratings yet

- Word Formation Prov VDocument4 pagesWord Formation Prov VAnonymous BF9P5gWINo ratings yet

- Acco 420 Final Coursepack CoursepacAplusDocument51 pagesAcco 420 Final Coursepack CoursepacAplusApril MayNo ratings yet

- Chapter 13 - Weighing Net Present Value and Other Capital Budgeting Criteria QuestionsDocument21 pagesChapter 13 - Weighing Net Present Value and Other Capital Budgeting Criteria QuestionsAhmad RahhalNo ratings yet

- ISAS Working Paper: Capital Account Convertibility in India: Revisiting The DebateDocument27 pagesISAS Working Paper: Capital Account Convertibility in India: Revisiting The DebateHitesh DiyoraNo ratings yet

- Medel vs. CA (299 Scra 481)Document6 pagesMedel vs. CA (299 Scra 481)mgbautistallaNo ratings yet

- Metropolitan Fabrics v. Prosperity Credit DIGEST Art 1391Document2 pagesMetropolitan Fabrics v. Prosperity Credit DIGEST Art 1391kooch100% (1)

- Report of Mrunali S. LilhareDocument2 pagesReport of Mrunali S. LilhareShashank KUmar Rai BhadurNo ratings yet

- Photo Developing and Printing DigitalDocument28 pagesPhoto Developing and Printing DigitalKashif SaeedNo ratings yet

- A Study On Factors Influencing of Women Policyholder's Investment Decision Towards Life Insurance Corporation of India Policies in ChennaiDocument6 pagesA Study On Factors Influencing of Women Policyholder's Investment Decision Towards Life Insurance Corporation of India Policies in ChennaiarcherselevatorsNo ratings yet

- MT China Great Wall of Debt PDFDocument34 pagesMT China Great Wall of Debt PDFBhairavi UvachaNo ratings yet

- 8 Lagrimas V CaDocument4 pages8 Lagrimas V CaMary Joy GorospeNo ratings yet

- Savant BrochureDocument2 pagesSavant BrochurebamapcomNo ratings yet

- 7 Principal Instrument of TransferDocument8 pages7 Principal Instrument of TransferAudrey Vivian50% (2)

- Venu 42 ReportDocument64 pagesVenu 42 ReportSubbaRaoNo ratings yet

- 19th Annual ReportDocument84 pages19th Annual ReportLochan KhanalNo ratings yet