US Fed FOMC Press Conference 18 September 2013 No Taper

US Fed FOMC Press Conference 18 September 2013 No Taper

Download as pdf or txt

You might also like

- Eclipse Download and Installation InstructionsDocument15 pagesEclipse Download and Installation InstructionsPrem KumarNo ratings yet

- Eli Lilly FinalDocument30 pagesEli Lilly FinalKarthik K Janardhanan0% (1)

- AMS 48 - 2000-n - D0114354 - 055 - 00Document116 pagesAMS 48 - 2000-n - D0114354 - 055 - 00wanhall100% (1)

- Fomc Pres Conf 20130918Document7 pagesFomc Pres Conf 20130918helmuthNo ratings yet

- Yellen TestimonyDocument7 pagesYellen TestimonyZerohedgeNo ratings yet

- SystemDocument8 pagesSystempathanfor786No ratings yet

- Fomc Pres Conf 20141217Document23 pagesFomc Pres Conf 20141217JoseLastNo ratings yet

- FOMCpresconf 20230614Document5 pagesFOMCpresconf 20230614Jhony SmithYTNo ratings yet

- Fomc Pres Conf 20160615Document21 pagesFomc Pres Conf 20160615petere056No ratings yet

- FOMCpresconf 20230503Document25 pagesFOMCpresconf 20230503Edi SaputraNo ratings yet

- Transcript of Chair Powell's Press Conference Opening Statement March 20, 2024Document4 pagesTranscript of Chair Powell's Press Conference Opening Statement March 20, 2024andre.torresNo ratings yet

- Yellen HHDocument7 pagesYellen HHZerohedgeNo ratings yet

- FOMC Word For Word Changes. 05.01.13Document2 pagesFOMC Word For Word Changes. 05.01.13Pensford FinancialNo ratings yet

- Fed TalkDocument2 pagesFed TalkTelegraphUKNo ratings yet

- FOMCpresconf 20220615Document27 pagesFOMCpresconf 20220615S CNo ratings yet

- Transcript of Chairman Bernanke's Press Conference April 25, 2012Document23 pagesTranscript of Chairman Bernanke's Press Conference April 25, 2012CoolidgeLowNo ratings yet

- Comptabilité Tle G3 Et G2Document24 pagesComptabilité Tle G3 Et G2albertvalk2.0No ratings yet

- FOMC Word For Word Changes 03.20.13Document2 pagesFOMC Word For Word Changes 03.20.13Pensford FinancialNo ratings yet

- FOMC Redline MarchDocument2 pagesFOMC Redline MarchZerohedgeNo ratings yet

- Fomc Pres Conf 20231101Document26 pagesFomc Pres Conf 20231101Quynh Le Thi NhuNo ratings yet

- FOMCpresconf 20220316Document26 pagesFOMCpresconf 20220316marchmtetNo ratings yet

- Oct FOMC RedlineDocument2 pagesOct FOMC RedlineZerohedgeNo ratings yet

- Fomc Pres Conf 20241218Document27 pagesFomc Pres Conf 20241218Yoniwo Edward TsemiNo ratings yet

- Fomc Pres Conf 20240501Document4 pagesFomc Pres Conf 20240501gustavo.kahilNo ratings yet

- The Market's Shocking Shock at The Fed's Non-Taper Shock: Economic ResearchDocument9 pagesThe Market's Shocking Shock at The Fed's Non-Taper Shock: Economic Researchapi-227433089No ratings yet

- PowellDocument4 pagesPowellandre.torres.dinheiramaNo ratings yet

- Fomc StatmentDocument1 pageFomc Statmentapi-280585983No ratings yet

- monetary-policy-summary-and-minutes-november-2024Document9 pagesmonetary-policy-summary-and-minutes-november-2024parsaNo ratings yet

- FOMCpresconf 20240501Document26 pagesFOMCpresconf 20240501David SimõesNo ratings yet

- Tassi BCE 17.10.2024 IngDocument6 pagesTassi BCE 17.10.2024 IngMaurizio VetereNo ratings yet

- Press Release: For Release at 2:00 P.M. EDTDocument2 pagesPress Release: For Release at 2:00 P.M. EDTTREND_7425No ratings yet

- December 17, 2014 Compared With October 29, 2014 Jeremie Cohen-SettonDocument3 pagesDecember 17, 2014 Compared With October 29, 2014 Jeremie Cohen-Settonapi-273992067No ratings yet

- Transcript of Chair Powell's Press Conference May 4, 2022Document24 pagesTranscript of Chair Powell's Press Conference May 4, 2022Learning的生活No ratings yet

- Fed 09212011Document2 pagesFed 09212011andrewbloggerNo ratings yet

- ResconfDocument4 pagesResconfgothurded24No ratings yet

- Fed SideDocument1 pageFed Sideannawitkowski88No ratings yet

- Macro Economics and Business Environment Assignment: Submitted To: Dr. C.S. AdhikariDocument8 pagesMacro Economics and Business Environment Assignment: Submitted To: Dr. C.S. Adhikarigaurav880No ratings yet

- Fomc Pres Conf 20241107Document22 pagesFomc Pres Conf 20241107sushilaoswal8378No ratings yet

- FOMC Rate Decision 04.25.12Document1 pageFOMC Rate Decision 04.25.12Pensford FinancialNo ratings yet

- Fomc Pres Conf 20241107Document23 pagesFomc Pres Conf 20241107Anyaji ChukwudiebubeNo ratings yet

- Fomc Pres Conf 20220727Document4 pagesFomc Pres Conf 20220727Jessica A. BotelhoNo ratings yet

- Critical Analysis GROUP-2Document6 pagesCritical Analysis GROUP-2Angelo MagtibayNo ratings yet

- Minutes Feb 2017Document12 pagesMinutes Feb 2017mahajanomicsNo ratings yet

- Jerome Powell's Written TestimonyDocument5 pagesJerome Powell's Written TestimonyTim MooreNo ratings yet

- FOMC Side by Side 11022011Document2 pagesFOMC Side by Side 11022011andrewbloggerNo ratings yet

- Federal Reserve Issues FOMC Statement: ShareDocument2 pagesFederal Reserve Issues FOMC Statement: ShareTREND_7425No ratings yet

- Monetary Policy Summary: Publication Date: 3 August 2017Document3 pagesMonetary Policy Summary: Publication Date: 3 August 2017TraderNo ratings yet

- Powell 20180717 ADocument6 pagesPowell 20180717 AZerohedgeNo ratings yet

- First Quarter Review of Monetary Policy 2012-13 Press Statement by Dr. D. SubbaraoDocument5 pagesFirst Quarter Review of Monetary Policy 2012-13 Press Statement by Dr. D. SubbaraoUttam AuddyNo ratings yet

- Monetary PolicyDocument18 pagesMonetary PolicyAnimNo ratings yet

- Monitory-Policy-Strategy, Case Study - RBADocument9 pagesMonitory-Policy-Strategy, Case Study - RBAoutbox175No ratings yet

- Paydata LTD - Do Inflation Expectations Currently Pose A Risk To The EconomyDocument2 pagesPaydata LTD - Do Inflation Expectations Currently Pose A Risk To The EconomyBenjamin RamirezNo ratings yet

- Fed Side by Side 20120125Document3 pagesFed Side by Side 20120125andrewbloggerNo ratings yet

- FED-POWEL-FOMCpresconf20240131Document4 pagesFED-POWEL-FOMCpresconf202401314200ethNo ratings yet

- Monetary20160316a1 PDFDocument3 pagesMonetary20160316a1 PDFHarissalamNo ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEandrewbloggerNo ratings yet

- Powell 20230621 ADocument5 pagesPowell 20230621 ADaily Caller News FoundationNo ratings yet

- A New Chapter For The FOMC Monetary Policy FramewDocument2 pagesA New Chapter For The FOMC Monetary Policy FramewsheeginNo ratings yet

- FOMCpresconf 20221102Document23 pagesFOMCpresconf 20221102Nava PourtaghiNo ratings yet

- Bce Introductory StatementDocument3 pagesBce Introductory StatementPietro ScarpaNo ratings yet

- KBC Flash - FOMC Statement: No Hints About TaperingDocument3 pagesKBC Flash - FOMC Statement: No Hints About TaperingKBC EconomicsNo ratings yet

- FOMC RedLineDocument2 pagesFOMC RedLineEduardo VinanteNo ratings yet

- Transparency in Financial Reporting: A concise comparison of IFRS and US GAAPFrom EverandTransparency in Financial Reporting: A concise comparison of IFRS and US GAAPRating: 4.5 out of 5 stars4.5/5 (3)

- MSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Document4 pagesMSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Jhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

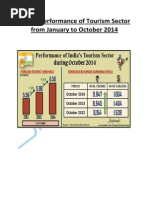

- India's Tourism Sector Performance For January and October 2014Document15 pagesIndia's Tourism Sector Performance For January and October 2014Jhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- India's Import and Export Update For September and December 2014Document16 pagesIndia's Import and Export Update For September and December 2014Jhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- India Tax Collection From April To November 2014Document11 pagesIndia Tax Collection From April To November 2014Jhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- Indian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Document5 pagesIndian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Jhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- India's Crude Oil and Natural Gas Production For Month of April, May and June 2014Document6 pagesIndia's Crude Oil and Natural Gas Production For Month of April, May and June 2014Jhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- India's Index of 8 Core Industry Performance For May 2014Document5 pagesIndia's Index of 8 Core Industry Performance For May 2014Jhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- Guidelines Format For JOURNAL OF MINERAL Processing and Engineering (20 PT, Bold)Document2 pagesGuidelines Format For JOURNAL OF MINERAL Processing and Engineering (20 PT, Bold)ikamelyaastutiNo ratings yet

- Assist Gas For Laser Cutting: For Internal Use OnlyDocument8 pagesAssist Gas For Laser Cutting: For Internal Use OnlymansoorlatifNo ratings yet

- Typical Soil Resistivity ValuesDocument5 pagesTypical Soil Resistivity ValueseduardoNo ratings yet

- Signal Degradation in Optical FibersDocument5 pagesSignal Degradation in Optical FibersijeteeditorNo ratings yet

- Interface Mass TraDocument26 pagesInterface Mass TraWahid AliNo ratings yet

- SGI Bulletin August 2013 1Document5 pagesSGI Bulletin August 2013 1Dumegã KokutseNo ratings yet

- Argumentative EssayDocument4 pagesArgumentative Essayapi-403488027No ratings yet

- Basf ProductsDocument2 pagesBasf ProductsequinoxoneNo ratings yet

- American Animation at First World WarDocument16 pagesAmerican Animation at First World WarSylwia KaliszNo ratings yet

- BIOLOGY EX 4Document15 pagesBIOLOGY EX 4micromaxsudaNo ratings yet

- Chapter 5 Motorola R56!09!01 05 Internal Grounding & BondingDocument72 pagesChapter 5 Motorola R56!09!01 05 Internal Grounding & BondingAnonymous V6y1QL6hn100% (1)

- Demand PagingDocument3 pagesDemand Pagingopbitu855No ratings yet

- Salaries - Rock Falls, East Coloma SD 12Document2 pagesSalaries - Rock Falls, East Coloma SD 12saukvalleynewsNo ratings yet

- Air Ground CSV SelectableDocument93 pagesAir Ground CSV SelectableNgan NguyenNo ratings yet

- Adobe Scan 25 Sep 2023Document6 pagesAdobe Scan 25 Sep 2023Linh LêNo ratings yet

- Book of Space 7th Edition NealDocument49 pagesBook of Space 7th Edition NealbuzycorryNo ratings yet

- lc3 IntroDocument17 pageslc3 IntroJustine Rome ArdepuelaNo ratings yet

- Python Prog pbl1Document11 pagesPython Prog pbl1SAI PRANEETHNo ratings yet

- M L A S: Topic: The Language of MathematicsDocument15 pagesM L A S: Topic: The Language of MathematicsRosen Anthony100% (1)

- Thermodynamics Multiple Choice Questions and AnswersDocument21 pagesThermodynamics Multiple Choice Questions and AnswersPadmavathi C50% (2)

- Dokumen - Tips Descriptive Comparative Historical LinguisticsDocument20 pagesDokumen - Tips Descriptive Comparative Historical LinguisticsSmt 355No ratings yet

- Strength and of Pond Ash ConcreteDocument29 pagesStrength and of Pond Ash ConcreteNaveed BNo ratings yet

- Lte Arch. and AifDocument14 pagesLte Arch. and AifMohsin AshrafNo ratings yet

- Manual Xbox 360 Slim 4gb PDFDocument78 pagesManual Xbox 360 Slim 4gb PDFodali batistaNo ratings yet

- Reflection Paper 1Document1 pageReflection Paper 1elizabeth clare yabutNo ratings yet

- Chapter 1 The Problem and Its BackgroundDocument7 pagesChapter 1 The Problem and Its BackgroundMr Dampha50% (2)