SME - An Indian Perspective

SME - An Indian Perspective

Download as doc, pdf, or txt

You might also like

- How To Read French Financial Statements PDFDocument4 pagesHow To Read French Financial Statements PDFJazzi SehrawatNo ratings yet

- MSMEs Project ReportDocument10 pagesMSMEs Project ReportVishal Goyal82% (11)

- M8 RevisionDocument204 pagesM8 RevisionjulydiaNo ratings yet

- Factors Affecting Business Strategy FormulationDocument16 pagesFactors Affecting Business Strategy FormulationKegan ピーター Wong100% (8)

- Title Investigation Report (Tir)Document6 pagesTitle Investigation Report (Tir)surendragiria100% (1)

- Electronica Finance Limited: Designing The Future of Micro, Small, and Medium EnterprisesDocument11 pagesElectronica Finance Limited: Designing The Future of Micro, Small, and Medium EnterprisesSamadarshi SiddharthaNo ratings yet

- Small and Medium Enterprises in India: Emerging Paradigm and Role For Chartered AccountantsDocument5 pagesSmall and Medium Enterprises in India: Emerging Paradigm and Role For Chartered AccountantsvikrantdifferentNo ratings yet

- Credit Rating For Small & Medium EnterprisesDocument47 pagesCredit Rating For Small & Medium EnterprisesKunal ThakurNo ratings yet

- MSMEDocument6 pagesMSMEkhagesh100% (1)

- Challenges of Financing Small Scale Business Enterprises in NigeriaDocument66 pagesChallenges of Financing Small Scale Business Enterprises in NigeriaShaguolo O. Joseph100% (3)

- Module 5 B and C IEGSDocument11 pagesModule 5 B and C IEGSRiddhima KarkeraNo ratings yet

- Main Problems Faced by Small Scale Industry in India Are Described BelowDocument7 pagesMain Problems Faced by Small Scale Industry in India Are Described BelowPrashant Madhukar KambleNo ratings yet

- MSMEs Project ReportDocument11 pagesMSMEs Project ReportAnkita GoyalNo ratings yet

- Indian Business Environment: Ibs BDocument17 pagesIndian Business Environment: Ibs BSangeetha K SNo ratings yet

- Working Capital FinanceDocument54 pagesWorking Capital FinanceAnkur RazdanNo ratings yet

- Swot Analysis of The Manufacturing and Service IndustryDocument15 pagesSwot Analysis of The Manufacturing and Service Industrypramita160775% (8)

- The Gujarat Vision:: Making Msmes Globally CompetitiveDocument52 pagesThe Gujarat Vision:: Making Msmes Globally CompetitivedivyangkvyasNo ratings yet

- Problems of Micro and Small EnterprisesDocument4 pagesProblems of Micro and Small EnterprisesMeenakshi AnilNo ratings yet

- Unit-1 The Micro-Small and Medium Enterprises (Msmes) Are Small Sized Entities, Defined inDocument36 pagesUnit-1 The Micro-Small and Medium Enterprises (Msmes) Are Small Sized Entities, Defined inBhaskaran BalamuraliNo ratings yet

- Monograph On Micro, Small and Medium Enterprises (Msmes) : The Institute of Cost & Works Accountants of IndiaDocument21 pagesMonograph On Micro, Small and Medium Enterprises (Msmes) : The Institute of Cost & Works Accountants of IndiaSsNo ratings yet

- MSME Issues and Challenges 1Document7 pagesMSME Issues and Challenges 1Rashmi Ranjan PanigrahiNo ratings yet

- Small and Medium Enterprises Financial ProblemsDocument4 pagesSmall and Medium Enterprises Financial ProblemsSaleh RehmanNo ratings yet

- Benchmarking: Practices and Tools For Achieving International Standards in Banking Sector To Overcome The Economic CrisisDocument29 pagesBenchmarking: Practices and Tools For Achieving International Standards in Banking Sector To Overcome The Economic Crisissadik953No ratings yet

- The Banking Sector Today Compares Favour Ably With Banking Sectors in The Region On Metrics Like GrowthDocument10 pagesThe Banking Sector Today Compares Favour Ably With Banking Sectors in The Region On Metrics Like GrowthbistamasterNo ratings yet

- Service Quality of Public Sector Banks To SME Customers: An Empirical Study in The Indian ContextDocument24 pagesService Quality of Public Sector Banks To SME Customers: An Empirical Study in The Indian Contextvikas_chourasiaNo ratings yet

- Problems of Managing Small Scale Business in The Rural AreaDocument48 pagesProblems of Managing Small Scale Business in The Rural Areakritika soniNo ratings yet

- Sme'S Past, Present & FutureDocument109 pagesSme'S Past, Present & Futureqwertyuiop_6421100% (2)

- Introduction To The IndustryDocument18 pagesIntroduction To The Industrynikunjsih sodhaNo ratings yet

- Banking On SME GrowthDocument34 pagesBanking On SME GrowthYuresh NadishanNo ratings yet

- MSME Strategic Action PlanDocument27 pagesMSME Strategic Action PlanRakesh SinghNo ratings yet

- Commercial Bank Credit and Its Contributions On Saheed WorkDocument5 pagesCommercial Bank Credit and Its Contributions On Saheed WorkFawazNo ratings yet

- Final PrintDocument24 pagesFinal PrintSwapnil AmbawadeNo ratings yet

- 5b) IndustryDocument26 pages5b) IndustrySHIVANSH BANSALNo ratings yet

- Problems of SMEDocument16 pagesProblems of SMEsamy7541No ratings yet

- Small Scale IndustriesDocument28 pagesSmall Scale IndustriesMohit Gupta25% (4)

- MSME SummaryDocument3 pagesMSME SummaryVashistaNo ratings yet

- Indian Retail Banking Industry: An AnalysisDocument13 pagesIndian Retail Banking Industry: An AnalysisAman SaxenaNo ratings yet

- Presentation On MSME'sDocument19 pagesPresentation On MSME'sKunal PuriNo ratings yet

- What Are MSME Its RoleDocument8 pagesWhat Are MSME Its RoleNeet 720No ratings yet

- IBE Unit 2-2Document47 pagesIBE Unit 2-2bhagyashripande321No ratings yet

- Indian Banking SectorDocument5 pagesIndian Banking Sector2612010No ratings yet

- National Manufacturing Policy CARE 041111Document5 pagesNational Manufacturing Policy CARE 041111Aashima GroverNo ratings yet

- Prateek Rest FinalDocument130 pagesPrateek Rest FinalPrateek Singh SidhuNo ratings yet

- International EconomicsDocument18 pagesInternational Economicsms_1226No ratings yet

- ExportDevFin FinalprojectRepoDocument117 pagesExportDevFin FinalprojectRepoSaikiran CheguriNo ratings yet

- Gbnews - Ch-Micro and Small Enterprises in Ethiopia Access To Credit Challenges and SolutionsDocument6 pagesGbnews - Ch-Micro and Small Enterprises in Ethiopia Access To Credit Challenges and Solutionsetebark h/michaleNo ratings yet

- Principles of Marketing Term Project Module 2Document16 pagesPrinciples of Marketing Term Project Module 2Palize QaziNo ratings yet

- SWOT Analysis of Banking IndustryDocument13 pagesSWOT Analysis of Banking IndustryApoorv94% (18)

- Lect 02 Multinational CorporationsDocument32 pagesLect 02 Multinational Corporationsdoninh2k4No ratings yet

- Help WalaDocument36 pagesHelp WalaPratikshya KarkiNo ratings yet

- MSMEDocument12 pagesMSMEVarun Tandon50% (2)

- MSMEs in IndiaDocument3 pagesMSMEs in IndianiyanmiloNo ratings yet

- Small and Medium EnterprisesDocument18 pagesSmall and Medium EnterprisesravishekramdevmailNo ratings yet

- Booster SectorsDocument5 pagesBooster SectorsNina Hooper0% (1)

- Role of SMEs Export Growth in BangladeshDocument19 pagesRole of SMEs Export Growth in BangladeshAsad ZamanNo ratings yet

- What Are The Challenges Likely To Be Encountered by The FirmsDocument6 pagesWhat Are The Challenges Likely To Be Encountered by The FirmsPallavi SaxenaNo ratings yet

- 01-G20 Joint Action Plan On SME FinancingDocument14 pages01-G20 Joint Action Plan On SME FinancingOumema AL AZHARNo ratings yet

- Address by DG RBIDocument8 pagesAddress by DG RBIHimanshu RanjanNo ratings yet

- Enhancing Competitiveness in Small Developing States: Approaches, Tools and PoliciesFrom EverandEnhancing Competitiveness in Small Developing States: Approaches, Tools and PoliciesNo ratings yet

- Public Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesFrom EverandPublic Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesNo ratings yet

- Toward Inclusive Access to Trade Finance: Lessons from the Trade Finance Gaps, Growth, and Jobs SurveyFrom EverandToward Inclusive Access to Trade Finance: Lessons from the Trade Finance Gaps, Growth, and Jobs SurveyNo ratings yet

- Somaliland: Private Sector-Led Growth and Transformation StrategyFrom EverandSomaliland: Private Sector-Led Growth and Transformation StrategyNo ratings yet

- Energy Project FinanceDocument6 pagesEnergy Project Financesurendragiria50% (2)

- Economic Survey 2009-10 MaharashtraDocument240 pagesEconomic Survey 2009-10 MaharashtrasurendragiriaNo ratings yet

- Economy Update - 2010Document15 pagesEconomy Update - 2010surendragiriaNo ratings yet

- Modern Portfolio Theory, Capital Market Theory, and Asset Pricing ModelsDocument33 pagesModern Portfolio Theory, Capital Market Theory, and Asset Pricing ModelsvamshidharNo ratings yet

- Balance Sheet Ratio Analysis FormulaDocument9 pagesBalance Sheet Ratio Analysis FormulaAbu Jahid100% (1)

- Audit Delay and Timeliness KuwaitDocument19 pagesAudit Delay and Timeliness KuwaitRivan Akbar SNo ratings yet

- Title IV - Value Added TaxDocument2 pagesTitle IV - Value Added TaxJennifer WilliamsNo ratings yet

- I. Statement of Financial Position (SFP)Document10 pagesI. Statement of Financial Position (SFP)Justin David SanducoNo ratings yet

- Guru Jambheshwar University of Science & Technology Hisar (Haryana)Document1 pageGuru Jambheshwar University of Science & Technology Hisar (Haryana)Sonu VermaNo ratings yet

- Prob 2-1: Mayberry Personal Receivers: Original Situation: Income Statement ($ Thousands) 2001 2002 2003Document8 pagesProb 2-1: Mayberry Personal Receivers: Original Situation: Income Statement ($ Thousands) 2001 2002 2003Ankit AgarwalNo ratings yet

- Brgy Maguikay, Mandaue City-BtDocument1 pageBrgy Maguikay, Mandaue City-BtHenry Kahal Orio Jr.No ratings yet

- ByjuDocument4 pagesByjuAakash ParmarNo ratings yet

- Global Legal Compliance Manager in Houston TX Resume Jill Burns-SuskiDocument3 pagesGlobal Legal Compliance Manager in Houston TX Resume Jill Burns-SuskiJill Burns SuskiNo ratings yet

- TQ in Financial Management (Pre-Final)Document8 pagesTQ in Financial Management (Pre-Final)Christine LealNo ratings yet

- National Spot Exchange Limited Scam Financial Management (HSM 404) Case Study (Cash Market Scams)Document40 pagesNational Spot Exchange Limited Scam Financial Management (HSM 404) Case Study (Cash Market Scams)Vardaan Bajaj100% (1)

- Cost of Capital Investment Firm's Objective of Wealth MaximizationDocument12 pagesCost of Capital Investment Firm's Objective of Wealth MaximizationDharani DharanNo ratings yet

- JSW Ispat Ar 2010-11Document106 pagesJSW Ispat Ar 2010-11Ashish KohaleNo ratings yet

- Study On Call Money & Commercial Paper MarketDocument28 pagesStudy On Call Money & Commercial Paper MarketVarun Puri100% (2)

- Hero Motohcorp LTDDocument6 pagesHero Motohcorp LTDJani KrunalNo ratings yet

- Leverage AnalysisDocument18 pagesLeverage Analysisiqbal irfaniNo ratings yet

- Comparative Financial StatementDocument25 pagesComparative Financial StatementharikrishnaNo ratings yet

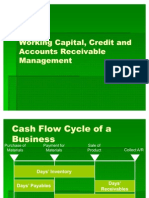

- Working Capital, Credit and Accounts Receivable ManagementDocument31 pagesWorking Capital, Credit and Accounts Receivable ManagementAnkit Agarwal100% (1)

- Barclays POINT BrochureDocument6 pagesBarclays POINT BrochureQilong ZhangNo ratings yet

- Cir V RufinoDocument2 pagesCir V RufinoNico NuñezNo ratings yet

- Asset Impairment - 18ADocument24 pagesAsset Impairment - 18ALinh Dang Thi ThuyNo ratings yet

- The Customer Satisfaction at Citi Bank Project Report Mba MarketingDocument38 pagesThe Customer Satisfaction at Citi Bank Project Report Mba MarketingBabasab Patil (Karrisatte)No ratings yet

- Article TDIndicators - Market Technician No 56 PDFDocument16 pagesArticle TDIndicators - Market Technician No 56 PDFlluuukNo ratings yet

- Sec Vs Unviersal Right FieldDocument3 pagesSec Vs Unviersal Right FieldThameenah ArahNo ratings yet

- Ap4 DerecognitionDocument18 pagesAp4 Derecognitioncheezhen5047No ratings yet

- Business Combination - AcquisitionDocument16 pagesBusiness Combination - AcquisitionAries Gonzales CaraganNo ratings yet

- Client Master List: National Securities Depository LimitedDocument2 pagesClient Master List: National Securities Depository LimitedNavjot SinghNo ratings yet