0% found this document useful (0 votes)

48 viewsFinal Report

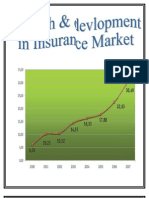

United India Insurance Company Ltd. is one of India's largest insurance companies formed after nationalization in 1972. It was incorporated in 1938 and grew significantly after absorbing several other insurers post-nationalization. Today it has over 18,000 employees across 1,340 offices providing insurance to over 1 crore policyholders. In recent years the company has focused on retail, MSME, and rural insurance segments. For the first half of FY2011-12, United India's profit rose over 50% and premium collection grew 27%, exceeding industry growth. The company was also entrusted to implement a new health insurance scheme for Tamil Nadu covering 1.34 crore families.

Uploaded by

Selva KumarCopyright

© © All Rights Reserved

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

48 viewsFinal Report

United India Insurance Company Ltd. is one of India's largest insurance companies formed after nationalization in 1972. It was incorporated in 1938 and grew significantly after absorbing several other insurers post-nationalization. Today it has over 18,000 employees across 1,340 offices providing insurance to over 1 crore policyholders. In recent years the company has focused on retail, MSME, and rural insurance segments. For the first half of FY2011-12, United India's profit rose over 50% and premium collection grew 27%, exceeding industry growth. The company was also entrusted to implement a new health insurance scheme for Tamil Nadu covering 1.34 crore families.

Uploaded by

Selva KumarCopyright

© © All Rights Reserved

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 31