0% found this document useful (0 votes)

205 viewsChapter 10 Homework Key

The document provides solutions to homework problems involving calculations of project cash flows, payback periods, net present value (NPV), and internal rate of return (IRR). Key details include:

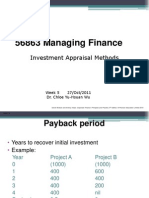

- Problem 1 involves cash flow calculations for a project and computing its payback period, NPV at 12%, and IRR.

- Problem 15 compares two mutually exclusive projects using various methods like payback, NPV, IRR, and equivalent annual annuity (EAA). Project B is preferred by NPV and A is preferred by other methods.

- Problem 23 evaluates two cold storage unit options for a company using NPV, with the $250,000 unit being preferred.

Uploaded by

CedrickBuenaventuraCopyright

© © All Rights Reserved

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

205 viewsChapter 10 Homework Key

The document provides solutions to homework problems involving calculations of project cash flows, payback periods, net present value (NPV), and internal rate of return (IRR). Key details include:

- Problem 1 involves cash flow calculations for a project and computing its payback period, NPV at 12%, and IRR.

- Problem 15 compares two mutually exclusive projects using various methods like payback, NPV, IRR, and equivalent annual annuity (EAA). Project B is preferred by NPV and A is preferred by other methods.

- Problem 23 evaluates two cold storage unit options for a company using NPV, with the $250,000 unit being preferred.

Uploaded by

CedrickBuenaventuraCopyright

© © All Rights Reserved

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 6