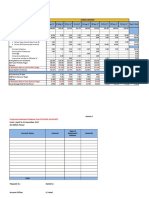

SP500 Valuation

SP500 Valuation

Download as pdf or txt

You might also like

- New General Mathematics For Secondary Schools 1 TG Full PDFDocument60 pagesNew General Mathematics For Secondary Schools 1 TG Full PDFMark Juniel Monzon69% (32)

- Cost and Production ToyataDocument3 pagesCost and Production ToyataJayaraj PoojaryNo ratings yet

- Plantilla para Calcular El Coeficiente K2Document4 pagesPlantilla para Calcular El Coeficiente K2Martin Jesus Maguiña CustodioNo ratings yet

- C19a Rio's SpreadsheetDocument8 pagesC19a Rio's SpreadsheetaluiscgNo ratings yet

- Answer Case Study-Smart CityDocument2 pagesAnswer Case Study-Smart CityRizky Almadinah AgustyNo ratings yet

- Corporate Finance: Class Notes 8Document18 pagesCorporate Finance: Class Notes 8Sakshi VermaNo ratings yet

- Advanced Capital Budgeting 3 HW - Q6Document4 pagesAdvanced Capital Budgeting 3 HW - Q6sairad1999No ratings yet

- International Financial Statistics (IFS)Document14 pagesInternational Financial Statistics (IFS)Muhammad Shahzad Ijaz (Mr. IJ)No ratings yet

- ECON254 Lecture3 Costs-SupplyDocument37 pagesECON254 Lecture3 Costs-SupplyKhalid JassimNo ratings yet

- Per AO Level (Sample Illustrative Template) : Period CoveredDocument3 pagesPer AO Level (Sample Illustrative Template) : Period CoveredAnonymous iScW9lNo ratings yet

- Tugas 6 BaprogDocument12 pagesTugas 6 BaprogAndy FadhilaNo ratings yet

- LabFG - 01 Practia 1Document7 pagesLabFG - 01 Practia 1andresmosqueragunadNo ratings yet

- Advanced Capital Budgeting 3 HW - q7Document3 pagesAdvanced Capital Budgeting 3 HW - q7sairad1999No ratings yet

- Startup Finance ModelDocument88 pagesStartup Finance ModelAbhishek AggarwalNo ratings yet

- Ejercicios Tema 3Document48 pagesEjercicios Tema 3Javier RubiolsNo ratings yet

- Jawaban tugas-BAB II-DISTRIBUSI-editDocument3 pagesJawaban tugas-BAB II-DISTRIBUSI-editSarazara IsaNo ratings yet

- Fronton 1 Tajeo 27N Tajeo 27S Tajeo 50N Tajeo 50S Tajeo 60N Tajeo 60S Tajeo 85N Tajeo 85SDocument5 pagesFronton 1 Tajeo 27N Tajeo 27S Tajeo 50N Tajeo 50S Tajeo 60N Tajeo 60S Tajeo 85N Tajeo 85SDannyElbisCatuntaHuisaNo ratings yet

- Lab ManualDocument6 pagesLab ManualNetsi FikiruNo ratings yet

- ESCOBER - SQ2 - Time Value of MoneyDocument48 pagesESCOBER - SQ2 - Time Value of MoneyNike Jericho EscoberNo ratings yet

- Sage One DF PDFDocument10 pagesSage One DF PDFBskkamNo ratings yet

- Statistics: N Valid Missing Mean Std. Error of Mean Median Mode Std. Deviation Variance Range Minimum Maximum SumDocument2 pagesStatistics: N Valid Missing Mean Std. Error of Mean Median Mode Std. Deviation Variance Range Minimum Maximum SumSiti Nur AfifahNo ratings yet

- UTS Statistika & Propabilitas 2019/2020: Program Studi Teknik Informatika Universitas Bumigora Mataram Ubg Mataram 2019Document7 pagesUTS Statistika & Propabilitas 2019/2020: Program Studi Teknik Informatika Universitas Bumigora Mataram Ubg Mataram 2019RSIA PERMATA HATINo ratings yet

- Batch 2Document1 pageBatch 2TRY11E PRIYADHARSHINI.MNo ratings yet

- Euroland - PlanilhaDocument4 pagesEuroland - PlanilhaIsrael VianaNo ratings yet

- Investment CriteriaDocument15 pagesInvestment CriteriaGOWTHAM K KNo ratings yet

- LINFASDocument25 pagesLINFASNani MulyatiNo ratings yet

- ContohcrossDocument3 pagesContohcrossMakarNo ratings yet

- Reuters ProVestor Plus Company ReportDocument20 pagesReuters ProVestor Plus Company ReportDunes BasherNo ratings yet

- Pws Anak 2Document1 pagePws Anak 2Andi SetiawanNo ratings yet

- Taller Esfuerzos GeostaticosDocument1 pageTaller Esfuerzos GeostaticosNicolas BilbaoNo ratings yet

- Consolidation Result Sheet: XXX Civil Engineering DepartmentDocument1 pageConsolidation Result Sheet: XXX Civil Engineering DepartmentMarshallNo ratings yet

- Construction Report Project ManagementDocument7 pagesConstruction Report Project ManagementTony Valdez100% (1)

- 2021-Risk and Rate of Return 2Document62 pages2021-Risk and Rate of Return 2Nur RofiumNo ratings yet

- Solution Key of Quiz 1 Statistics - Mathematics For Mnagment - Fall - 2021 27032022 034720pmDocument4 pagesSolution Key of Quiz 1 Statistics - Mathematics For Mnagment - Fall - 2021 27032022 034720pmhassanmuzammil217No ratings yet

- Micro Eportfolio Monopoly Spreadsheet Data - SPG 18 - FinalDocument4 pagesMicro Eportfolio Monopoly Spreadsheet Data - SPG 18 - Finalapi-302890540No ratings yet

- Which Project Should You Accept and Why?: Chart TitleDocument7 pagesWhich Project Should You Accept and Why?: Chart Titlesohinidas91No ratings yet

- Capital Budgeting Decisions - Great LakeDocument11 pagesCapital Budgeting Decisions - Great LakeHalsa SNo ratings yet

- 1301Document1 page1301Eric HuangNo ratings yet

- Stable DividendDocument6 pagesStable Dividendanon-821638100% (2)

- Reporter: Kenneth B. Dizon Joseph Kent Paring Carlo GillaDocument7 pagesReporter: Kenneth B. Dizon Joseph Kent Paring Carlo GillaLyceljine C. TañedoNo ratings yet

- Topic: Table of SpecificationsDocument5 pagesTopic: Table of Specificationsprincerojas630No ratings yet

- Batch 1Document1 pageBatch 1TRY11E PRIYADHARSHINI.MNo ratings yet

- 7 Psy Chart XLSDocument34 pages7 Psy Chart XLSlakshminarayananNo ratings yet

- Theory of Costs A ReviewerDocument11 pagesTheory of Costs A ReviewerRina SoNo ratings yet

- Financiero SmuckersDocument9 pagesFinanciero SmuckerserickNo ratings yet

- Soil Boring 1Document239 pagesSoil Boring 1Muhammad Rizki SalmanNo ratings yet

- Ratio Analysis CHARTDocument2 pagesRatio Analysis CHARTSaumay BhargavaNo ratings yet

- FrameDesign DocumentDocument12 pagesFrameDesign Documentlaleska moyaNo ratings yet

- Data Demografi: Statistics Pekerjaan SuamiDocument2 pagesData Demografi: Statistics Pekerjaan SuamiAnonymous EVOIHPYNo ratings yet

- SPSS TabulasiDocument4 pagesSPSS TabulasiFeri DanielNo ratings yet

- 5-Year Budget: Indirect Cost Rates 2014-2016Document10 pages5-Year Budget: Indirect Cost Rates 2014-2016Ch Raheel BhattiNo ratings yet

- Bai 2.xlsx De2Document4 pagesBai 2.xlsx De2letruongkhanhdung096No ratings yet

- Precipitaciones MaximasDocument18 pagesPrecipitaciones MaximasEdison Jerson Ramirez ToledoNo ratings yet

- Kitchen Aid Products, Inc., Manufactures Small Kitchen AppliancesDocument7 pagesKitchen Aid Products, Inc., Manufactures Small Kitchen AppliancesGalina FateevaNo ratings yet

- Faisal Mid Excel GraphsDocument5 pagesFaisal Mid Excel Graphsfasi12No ratings yet

- Business Description: XYZ Website TelephoneDocument8 pagesBusiness Description: XYZ Website TelephoneStock PromotionsNo ratings yet

- Solve Splits Feedback ToolDocument6 pagesSolve Splits Feedback ToolkabyaNo ratings yet

- EWMA Cusum Charts Examples Ch09Document4 pagesEWMA Cusum Charts Examples Ch09Diana RuizNo ratings yet

- Output SPSSDocument76 pagesOutput SPSSmuliadin_74426729No ratings yet

- Analisis Univariat: StatisticsDocument3 pagesAnalisis Univariat: StatisticsNadya ParamithaNo ratings yet

- Data KajianDocument3 pagesData KajianfikririansyahNo ratings yet

- AroundTheWorldIn8Pages Q1 2019 LVDocument41 pagesAroundTheWorldIn8Pages Q1 2019 LVstreettalk700No ratings yet

- Greg Morris - 2017 Economic & Investment Summit Presentation - Questionable PracticesDocument53 pagesGreg Morris - 2017 Economic & Investment Summit Presentation - Questionable Practicesstreettalk700No ratings yet

- GTA Introduction RIA ProDocument7 pagesGTA Introduction RIA Prostreettalk700100% (2)

- EmpDocument6 pagesEmpdpbasicNo ratings yet

- Investor Intelligence Techical Analysis GuideDocument25 pagesInvestor Intelligence Techical Analysis Guidestreettalk700No ratings yet

- Summer Market Outlook & ForecastDocument51 pagesSummer Market Outlook & Forecaststreettalk700No ratings yet

- X-Factor Report 1/28/13 - Will The Market Ever Correct?Document10 pagesX-Factor Report 1/28/13 - Will The Market Ever Correct?streettalk700No ratings yet

- Value Investor Forum Presentation 2015 (Print Version)Document29 pagesValue Investor Forum Presentation 2015 (Print Version)streettalk700No ratings yet

- Companies Paying Dividend SP500 - 2007-2015Document8 pagesCompanies Paying Dividend SP500 - 2007-2015streettalk700No ratings yet

- Psychology of Risk-Behavioral Finance PerspectiveDocument28 pagesPsychology of Risk-Behavioral Finance Perspectivestreettalk700No ratings yet

- Unconventional Policies and Their Effects On Financial Markets PDFDocument36 pagesUnconventional Policies and Their Effects On Financial Markets PDFSoberLookNo ratings yet

- Companies Paying Dividend SP500 - 2007-2015Document8 pagesCompanies Paying Dividend SP500 - 2007-2015streettalk700No ratings yet

- A. Gary Shilling's: InsightDocument4 pagesA. Gary Shilling's: Insightstreettalk700100% (1)

- Lacy Hunt - Hoisington - Quartely Review Q1 2014Document5 pagesLacy Hunt - Hoisington - Quartely Review Q1 2014TREND_7425No ratings yet

- GMO Capital Q4 2012 LetterDocument14 pagesGMO Capital Q4 2012 LetterWall Street WanderlustNo ratings yet

- Understanding The Bear CaseDocument17 pagesUnderstanding The Bear Casestreettalk700No ratings yet

- Cycles and Possible OutcomesDocument6 pagesCycles and Possible Outcomesstreettalk700No ratings yet

- The Great American Non-RecoveryDocument10 pagesThe Great American Non-Recoverystreettalk700No ratings yet

- Valuations Suggest Extremely Overvalued MarketDocument9 pagesValuations Suggest Extremely Overvalued Marketstreettalk700No ratings yet

- A Comparison of The Real-Time Performance of Business Cycle Dating MethodsDocument28 pagesA Comparison of The Real-Time Performance of Business Cycle Dating MethodscaitlynharveyNo ratings yet

- Is US Economic Growth OverDocument25 pagesIs US Economic Growth Overstreettalk700No ratings yet

- Personal Finance Webinar Presentation 11/12/2012 Streettalk AdvsiorsDocument19 pagesPersonal Finance Webinar Presentation 11/12/2012 Streettalk Advsiorsstreettalk700No ratings yet

- Is US Economic Growth OverDocument25 pagesIs US Economic Growth Overstreettalk700No ratings yet

- Stem ProjectDocument16 pagesStem Projectapi-314126399No ratings yet

- The Schools Listed Overleaf Have All Been Authorised by Their Local EducationDocument9 pagesThe Schools Listed Overleaf Have All Been Authorised by Their Local Educationjarienza.gehNo ratings yet

- Second Term Exam Revision Worksheet Islamic Grade 5 2Document13 pagesSecond Term Exam Revision Worksheet Islamic Grade 5 2Asmaa HefziNo ratings yet

- Collective ResponsibilityDocument34 pagesCollective ResponsibilityalbertolecarosNo ratings yet

- 35-Article Text-158-1-10-20220424Document8 pages35-Article Text-158-1-10-20220424kelompok 4 Ekonomi lingkunganNo ratings yet

- Mauritius SDG Investor MapDocument17 pagesMauritius SDG Investor Mapabhay.mathurNo ratings yet

- Check Point Engineer TroubleshootingDocument3 pagesCheck Point Engineer TroubleshootingvikrantageorgeNo ratings yet

- Relevant Contracts TaxDocument11 pagesRelevant Contracts TaxTe KruNo ratings yet

- India - Political Divisions and Physical FeaturesDocument61 pagesIndia - Political Divisions and Physical FeaturesemlynjiteshtNo ratings yet

- Fresher Juice Activation PlanDocument14 pagesFresher Juice Activation PlanMalik Muhammad SufyanNo ratings yet

- EST Brochure JordanDocument2 pagesEST Brochure JordanMahmood ShanaahNo ratings yet

- Redefining The Role of The TeacherDocument4 pagesRedefining The Role of The TeacherJavier DominguezNo ratings yet

- 4a's Approach Lesson Plan.Document2 pages4a's Approach Lesson Plan.Ceraz AbdurahmanNo ratings yet

- Syllabus: International Institute of Professional Studies Davv, IndoreDocument13 pagesSyllabus: International Institute of Professional Studies Davv, IndoreKavish SharmaNo ratings yet

- Checklist A1 Version 1.0Document11 pagesChecklist A1 Version 1.0Renzo Diaz DelgadoNo ratings yet

- RoEnRo - Year - II - Nos - 2-3 - February 2014 - June 2015Document177 pagesRoEnRo - Year - II - Nos - 2-3 - February 2014 - June 2015Gabriela PachiaNo ratings yet

- Sujet BTS Anglais 2022Document4 pagesSujet BTS Anglais 2022MoïsetteNo ratings yet

- Economic Nationalism (DoW) (Self)Document7 pagesEconomic Nationalism (DoW) (Self)Shaurya JeetNo ratings yet

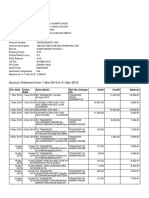

- Account Statement From 1 Mar 2019 To 31 Mar 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Mar 2019 To 31 Mar 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSaurabh SinghNo ratings yet

- Core Mantle Change Impact MineDocument211 pagesCore Mantle Change Impact MineVincent J. CataldiNo ratings yet

- Shell Mex House Pearsons PLC History British Intelligence and OilDocument8 pagesShell Mex House Pearsons PLC History British Intelligence and OilJohn Adam St Gang: Crown ControlNo ratings yet

- Lesson Worksheet: 6.1A MeanDocument7 pagesLesson Worksheet: 6.1A Meanwaiman fuNo ratings yet

- Supply Chain Management-PepsiDocument25 pagesSupply Chain Management-PepsiSusrita Sen98% (48)

- Chapter 2 - Examples - SolutionsDocument11 pagesChapter 2 - Examples - SolutionsAhmed walidNo ratings yet

- Hmda Brochure NeopolisDocument33 pagesHmda Brochure NeopolisJohn SharonNo ratings yet

- Questions On Real Options in Capital BudgetingDocument2 pagesQuestions On Real Options in Capital Budgetingjoelmanoj98No ratings yet

- LacosteDocument21 pagesLacosteSunny SharmaNo ratings yet

- Online PP2Document20 pagesOnline PP2Muhammad HanifNo ratings yet