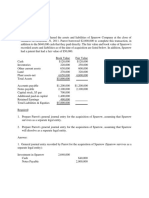

Problem Ch.14

Problem Ch.14

Download as docx, pdf, or txt

You might also like

- Soal 1 (LO3 10%) : Tugas Personal Ke-2 Week 7Document16 pagesSoal 1 (LO3 10%) : Tugas Personal Ke-2 Week 7Nadilla Nur100% (2)

- Tugas Personal 1 - Diaz Hesron Deo Simorangkir - 2602202526Document6 pagesTugas Personal 1 - Diaz Hesron Deo Simorangkir - 2602202526Diaz Hesron Deo SimorangkirNo ratings yet

- Ex Ch.17Document3 pagesEx Ch.17kenny 322016048No ratings yet

- SolutionDocument6 pagesSolutionJhazzie Dolor100% (1)

- M&A CaseDocument5 pagesM&A CaseRashleen AroraNo ratings yet

- CH 14Document2 pagesCH 14tigger5191100% (1)

- Homework Ch2Document33 pagesHomework Ch2Keith Joanne SantiagoNo ratings yet

- Problem 5-4Document3 pagesProblem 5-4Diata Ian100% (4)

- Problem 1 Current Liability Entries and Adjustments: InstructionsDocument6 pagesProblem 1 Current Liability Entries and Adjustments: Instructionsbeeeeee100% (1)

- 5.1 Multiple Choice Questions: Chapter 5 Intercompany Profit Transactions - InventoriesDocument36 pages5.1 Multiple Choice Questions: Chapter 5 Intercompany Profit Transactions - InventoriesGaith1 AldaajahNo ratings yet

- Tugas Kel 3 (P14.2, P14.4)Document7 pagesTugas Kel 3 (P14.2, P14.4)Alexandra AmadeaNo ratings yet

- Bab 14Document4 pagesBab 14tutykaykay67% (3)

- Toy World - ExhibitsDocument9 pagesToy World - Exhibitsakhilkrishnan007No ratings yet

- Jawaban BE15 - AKMDocument3 pagesJawaban BE15 - AKMMazz BadruezNo ratings yet

- E21.4 (LO 2, 4) (Lessee Entries, Unguaranteed Residual Value) Assume That OnDocument3 pagesE21.4 (LO 2, 4) (Lessee Entries, Unguaranteed Residual Value) Assume That OnWarmthx0% (1)

- P2 41 2 42 SolutionsDocument3 pagesP2 41 2 42 SolutionsMarjorie PalmaNo ratings yet

- Week1 SolutionsDocument14 pagesWeek1 SolutionsM Mustafa100% (1)

- Ex Ch.15Document2 pagesEx Ch.15kenny 322016048No ratings yet

- 302 CH 14 Class ProblemsDocument7 pages302 CH 14 Class ProblemsBettie Sanchez100% (1)

- ACCT550 Homework Week 6Document6 pagesACCT550 Homework Week 6Natasha DeclanNo ratings yet

- Tugas AKM II Minggu 10 E24.2 Dan E24.3 - Clarissa Nastania (441354)Document2 pagesTugas AKM II Minggu 10 E24.2 Dan E24.3 - Clarissa Nastania (441354)Clarissa NastaniaNo ratings yet

- CH 04Document26 pagesCH 04Ahmed Al EkamNo ratings yet

- Problem 14-10Document2 pagesProblem 14-10annisaNo ratings yet

- Unit 6 Essay Assignment Corporate Framework On Strategic Auditing Dolores Bell 3.31.19Document13 pagesUnit 6 Essay Assignment Corporate Framework On Strategic Auditing Dolores Bell 3.31.19JaunNo ratings yet

- Acct 2101 Exam 1 Study GuideDocument3 pagesAcct 2101 Exam 1 Study GuideDavid Lee100% (1)

- AKM - Kelompok 5Document8 pagesAKM - Kelompok 5lailafitriyani100% (1)

- Week13 SolutionsDocument14 pagesWeek13 SolutionsRian Rorres100% (1)

- DocxDocument21 pagesDocxIzzy BNo ratings yet

- Exe Ch.13Document4 pagesExe Ch.13kenny 3220160480% (1)

- Akuntansi KeuanganDocument11 pagesAkuntansi KeuanganDyan NoviaNo ratings yet

- IFRS 15 - Exercises (Kieso)Document10 pagesIFRS 15 - Exercises (Kieso)Iris Claire GamadNo ratings yet

- BINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Document3 pagesBINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Audrey NataliaNo ratings yet

- Chapter 11Document33 pagesChapter 11Mahmoud Abu ShamlehNo ratings yet

- Exercise 21Document3 pagesExercise 21Ruth UtamiNo ratings yet

- Tugas 1 AklDocument3 pagesTugas 1 Akledit andraeNo ratings yet

- Bab 3 Chapter 12 PDFDocument4 pagesBab 3 Chapter 12 PDFGrifyn IfyNo ratings yet

- CH 14 MCDocument38 pagesCH 14 MCElaine Lingx100% (1)

- E22-6 (LO 2) Accounting Changes-DepreciationDocument6 pagesE22-6 (LO 2) Accounting Changes-DepreciationRiana DeztianiNo ratings yet

- Individual Assignments 2Document8 pagesIndividual Assignments 2Arista Yuliana SariNo ratings yet

- Soal Chapter 17Document6 pagesSoal Chapter 17Baiq Melaty Sepsa WindiNo ratings yet

- CH 06Document50 pagesCH 06Dr-Bahaaeddin Alareeni100% (1)

- Tugas Kelompok Ke-3 Week 8: Soal 1 (LO3 10%)Document6 pagesTugas Kelompok Ke-3 Week 8: Soal 1 (LO3 10%)Samuel Jose RizalNo ratings yet

- TaufiqAlInsanSiahaan - Tugas Akuntansi Keuangan Menengah 1Document6 pagesTaufiqAlInsanSiahaan - Tugas Akuntansi Keuangan Menengah 1taufiq al insanNo ratings yet

- CH 18 20 AKMDocument121 pagesCH 18 20 AKMDewanto Kusumo100% (1)

- Total Excess of Cost Over Book Value Acquired $4,000,000Document5 pagesTotal Excess of Cost Over Book Value Acquired $4,000,000SAHRINDA YUNIAWATINo ratings yet

- 2311 Acct6131039 Lhfa TK1-W3-S4-R2 Team8Document8 pages2311 Acct6131039 Lhfa TK1-W3-S4-R2 Team8Nadilla NurNo ratings yet

- Intermediate Accounting: E13-1. (Statement of Financial Position Classification) How Would Each of The FollowingDocument6 pagesIntermediate Accounting: E13-1. (Statement of Financial Position Classification) How Would Each of The FollowingFria Mae Aycardo AbellanoNo ratings yet

- 13 2Document2 pages13 2Evelyn Roldan100% (8)

- CH 8Document13 pagesCH 8doc nurfatkhiyahNo ratings yet

- Fix Asset&Intangible AssetDocument7 pagesFix Asset&Intangible AssetAdinda0% (1)

- CH 14Document39 pagesCH 14Iris MaNo ratings yet

- Tugas CH 8 Dan 9Document13 pagesTugas CH 8 Dan 9muhammad alfariziNo ratings yet

- Preliminary ComputationsDocument3 pagesPreliminary ComputationsFarrell DmNo ratings yet

- Advance Acc P2Document7 pagesAdvance Acc P2Putri anjjarwatiNo ratings yet

- Lucky Carrot : Show Transcribed Image TextDocument2 pagesLucky Carrot : Show Transcribed Image TextAchmad RizalNo ratings yet

- Tugas Audit Fix Bener Semua PDFDocument19 pagesTugas Audit Fix Bener Semua PDF「絆笑」HodaeNo ratings yet

- Tugas AKM III - Week 2Document10 pagesTugas AKM III - Week 2Rifda Amalia100% (1)

- 1 Chapter 1 Partnership FormationDocument16 pages1 Chapter 1 Partnership FormationJymldy EnclnNo ratings yet

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 pagesNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarNo ratings yet

- Soal Ujian AK1Document126 pagesSoal Ujian AK1tyasardyraNo ratings yet

- Ch14 Suggested HWDocument21 pagesCh14 Suggested HWLalangelaNo ratings yet

- Chapter 14Document37 pagesChapter 14ReineNo ratings yet

- Liabilities Part 2 TutorialDocument3 pagesLiabilities Part 2 TutorialSalma HazemNo ratings yet

- Ch14 Required QuestionsDocument31 pagesCh14 Required QuestionsMaha M. Al-MasriNo ratings yet

- AP Municipal Budget ManualDocument65 pagesAP Municipal Budget ManualSAtya GAndhiNo ratings yet

- Annual Report: The Year in ReviewDocument42 pagesAnnual Report: The Year in ReviewSabina MunteanuNo ratings yet

- Investor Presentation-10-04-2019 - Hyundai SteelDocument33 pagesInvestor Presentation-10-04-2019 - Hyundai SteelVishad VatsNo ratings yet

- DLFDocument6 pagesDLFShubham TyagiNo ratings yet

- Bank Islam Malaysia Handbook PDFDocument130 pagesBank Islam Malaysia Handbook PDFReza HaryohatmodjoNo ratings yet

- Fedwire Funds Transfer SystemseminarDocument17 pagesFedwire Funds Transfer SystemseminarVijai RaghavanNo ratings yet

- The American Marketing Association Defines A Brand As ADocument12 pagesThe American Marketing Association Defines A Brand As AVish LalzareNo ratings yet

- Retirement Planning With AnnuitiesDocument11 pagesRetirement Planning With Annuitiesapi-246909910No ratings yet

- AE 19 Chapter I Lecture Notes PDFDocument11 pagesAE 19 Chapter I Lecture Notes PDFJhomel Domingo GalvezNo ratings yet

- Acco 20233 Income Tax Chapter 5Document18 pagesAcco 20233 Income Tax Chapter 5Kia Mae PALOMARNo ratings yet

- Project 200Document3 pagesProject 200Mayur ShahNo ratings yet

- FINANCIAL LIABILITY AT AMORTIZED COSTS - Bonds Payable-Compound Fin Instruments-Debt Restructuring (20231016164208)Document3 pagesFINANCIAL LIABILITY AT AMORTIZED COSTS - Bonds Payable-Compound Fin Instruments-Debt Restructuring (20231016164208)ocampojohnoliver1901182No ratings yet

- Sa 402 PDFDocument26 pagesSa 402 PDFWael AshajiNo ratings yet

- Australian Sharemarket: TablesDocument17 pagesAustralian Sharemarket: TablesallegreNo ratings yet

- Efficycle 2018-Marketing Presentation FormatDocument4 pagesEfficycle 2018-Marketing Presentation FormatSimranpreet SinghNo ratings yet

- Chapter 1-Fundamentals of Financial AccountingDocument11 pagesChapter 1-Fundamentals of Financial AccountingBlezzher Marsie ValerioNo ratings yet

- DRHP Home First FinanceDocument357 pagesDRHP Home First FinanceHarsh KediaNo ratings yet

- SRM School of Management SRM University International Finance MBN 664 Lesson PlanDocument5 pagesSRM School of Management SRM University International Finance MBN 664 Lesson Plankanagaraj176No ratings yet

- Instruction For Trust Account: Sogotrade New Account ContactDocument10 pagesInstruction For Trust Account: Sogotrade New Account ContactVasishtha TeeluckdharryNo ratings yet

- CR Pocket NoteDocument166 pagesCR Pocket NoteLaffin Ebi Laffin100% (1)

- International Journal of Business and Management Invention (IJBMI)Document10 pagesInternational Journal of Business and Management Invention (IJBMI)inventionjournalsNo ratings yet

- 200 Business IdeasDocument258 pages200 Business Ideaskwoshaba pidson88% (8)

- Rapurapu Case Report PDFDocument64 pagesRapurapu Case Report PDFAlfonso Miguel RomeroNo ratings yet

- An Analysis of Gains To Acquiring Firm S Shareholders The Special Case of REITsDocument10 pagesAn Analysis of Gains To Acquiring Firm S Shareholders The Special Case of REITsZhang PeilinNo ratings yet

- Cost Accounting Vol-IDocument48 pagesCost Accounting Vol-ImanoNo ratings yet

- Financial Management Assignment 2Document24 pagesFinancial Management Assignment 2Rohan AhujaNo ratings yet