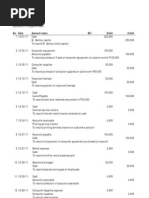

Long Examination Cash Set A

Long Examination Cash Set A

Download as docx, pdf, or txt

You might also like

- The Trend Trader Nick Radge On Demand PDFDocument8 pagesThe Trend Trader Nick Radge On Demand PDFDedi Tri LaksonoNo ratings yet

- Financial AccountingDocument2 pagesFinancial AccountingRakesh Sharma25% (4)

- Docsity Fundamentals of Accounting 1 3Document5 pagesDocsity Fundamentals of Accounting 1 3Timothy Arbues ReyesNo ratings yet

- Accounting Entry TallyDocument50 pagesAccounting Entry TallyHari Narayana100% (2)

- RecvbleDocument24 pagesRecvbleJoseph Salido100% (1)

- Acctng Error 2Document5 pagesAcctng Error 2Kim FloresNo ratings yet

- ch01 Introduction Acounting & BusinessDocument37 pagesch01 Introduction Acounting & Businesskuncoroooo100% (1)

- Practical Accounting 1Document6 pagesPractical Accounting 1glrosaaa c100% (1)

- Page Comprehensive Theories and ProblemsDocument7 pagesPage Comprehensive Theories and Problemsharley_quinn11No ratings yet

- Audit of CashDocument4 pagesAudit of CashandreamrieNo ratings yet

- General Journal SampleDocument2 pagesGeneral Journal SampleBusinessTips.Ph89% (19)

- RAPPLER HOLDINGS CORPORATION'S Accounts Receivable Subsidiary Ledger Shows The FollowingDocument2 pagesRAPPLER HOLDINGS CORPORATION'S Accounts Receivable Subsidiary Ledger Shows The FollowingAlvinDumanggasNo ratings yet

- Karkits Corporation PDFDocument4 pagesKarkits Corporation PDFRachel LeachonNo ratings yet

- MQ 1 Receivables and InventoryDocument4 pagesMQ 1 Receivables and Inventorymarygraceomac100% (2)

- 5 Questions InventoryDocument15 pages5 Questions Inventoryyousef0% (1)

- Far Eastern University - Manila Institute of Accounts, Business and Finance Nicanor Reyes Sr. ST., Sampaloc, Manila Applied AuditingDocument6 pagesFar Eastern University - Manila Institute of Accounts, Business and Finance Nicanor Reyes Sr. ST., Sampaloc, Manila Applied AuditingKenneth A. S. AlabadoNo ratings yet

- Preweek Auditing Problems 2014 PDFDocument41 pagesPreweek Auditing Problems 2014 PDFalellieNo ratings yet

- SA1 Submissions: Standalone AssessmentDocument11 pagesSA1 Submissions: Standalone AssessmentYenNo ratings yet

- Since Accountancy Is A Quota CourseDocument1 pageSince Accountancy Is A Quota Courselindsay boncodinNo ratings yet

- LTCC FormulaDocument2 pagesLTCC FormulaReginald ValenciaNo ratings yet

- Fin Asset at Fair ValueDocument2 pagesFin Asset at Fair ValueLove RosalunaNo ratings yet

- Accounts ReceivablesDocument10 pagesAccounts ReceivablesYenelyn Apistar Cambarijan0% (1)

- PNC MT Examination Finacc 3Document3 pagesPNC MT Examination Finacc 3joevitt delfinadoNo ratings yet

- Final Exam 12 PDF FreeDocument17 pagesFinal Exam 12 PDF FreeEmey CalbayNo ratings yet

- Audit of Cash: Problem No. 1Document4 pagesAudit of Cash: Problem No. 1Kathrina RoxasNo ratings yet

- Chapter 111213Document8 pagesChapter 111213Angel Alejo Acoba0% (1)

- Audit of InventoriesDocument23 pagesAudit of InventoriesMae-shane SagayoNo ratings yet

- Reviewer 1st PB P1 1920Document7 pagesReviewer 1st PB P1 1920Therese AcostaNo ratings yet

- Retained EarningsDocument9 pagesRetained EarningsCamille GarciaNo ratings yet

- The Custodian Is Not Authorized To Cash ChecksDocument3 pagesThe Custodian Is Not Authorized To Cash Checkselsana philipNo ratings yet

- AP AnswerKeyDocument6 pagesAP AnswerKeyRosalie E. Balhag100% (2)

- Ad2 1Document13 pagesAd2 1MarjorieNo ratings yet

- Activity #1Document5 pagesActivity #1Lyka Nicole DoradoNo ratings yet

- Midterm Exam No. 1Document2 pagesMidterm Exam No. 1Anie Martinez100% (1)

- Final Examination in Auditing Principles and Application 1Document8 pagesFinal Examination in Auditing Principles and Application 1Anie Martinez0% (1)

- Afar 12 Franchise Accounting: Straight ProblemsDocument2 pagesAfar 12 Franchise Accounting: Straight ProblemsJem Valmonte100% (1)

- LecDocument12 pagesLecLorenaTuazonNo ratings yet

- Handout No. 3Document6 pagesHandout No. 3Villena Divina VictoriaNo ratings yet

- Bsais 4JDocument18 pagesBsais 4JArjay DeausenNo ratings yet

- Acctg Ats1Document2 pagesAcctg Ats1Christian N MagsinoNo ratings yet

- AR Quiz Page 2Document25 pagesAR Quiz Page 2Xia AlliaNo ratings yet

- Case Carolina-Wilderness-Outfitters-Case-Study PDFDocument8 pagesCase Carolina-Wilderness-Outfitters-Case-Study PDFMira miguelito50% (2)

- Divine Word College of Laoag Vision: 1 Assignment For AE17-Strategic Business Analysis Organizational PerspectiveDocument2 pagesDivine Word College of Laoag Vision: 1 Assignment For AE17-Strategic Business Analysis Organizational PerspectiveKeith Joshua GabiasonNo ratings yet

- Audit-Of Inventory ACHA - KJDocument47 pagesAudit-Of Inventory ACHA - KJKhrisna Joy AchaNo ratings yet

- Quiz 5 Acc 401Document10 pagesQuiz 5 Acc 401EML0% (1)

- Business Combination Module 3Document8 pagesBusiness Combination Module 3TryonNo ratings yet

- 01 PartnershipDocument6 pages01 Partnershipdom baldemorNo ratings yet

- Quiz - Financial Statements With SolutionDocument6 pagesQuiz - Financial Statements With SolutionMary Yvonne AresNo ratings yet

- Partnership Liquidation InstallmentDocument1 pagePartnership Liquidation InstallmentAkira Marantal ValdezNo ratings yet

- Pure ProblemsDocument7 pagesPure Problemschristine anglaNo ratings yet

- DocxDocument33 pagesDocxGray Javier0% (1)

- Finals-Business CombiDocument5 pagesFinals-Business Combijhell de la cruzNo ratings yet

- Unit IA ID. Rematch Unit Drill On Cash and Cash Equivalents Petty Cash Bank Recon Proof of Cash 1Document5 pagesUnit IA ID. Rematch Unit Drill On Cash and Cash Equivalents Petty Cash Bank Recon Proof of Cash 1MARK JHEN SALANGNo ratings yet

- Relevant Provision of The Pfrs For SmeDocument26 pagesRelevant Provision of The Pfrs For SmeTheresa MacasiebNo ratings yet

- MB2 2013 Ap Set ADocument6 pagesMB2 2013 Ap Set AMary Queen Ramos-UmoquitNo ratings yet

- 123Document11 pages123Jandave ApinoNo ratings yet

- Private Nor-for-Profit Entities (NPE) : Colleges and Universities, Hospitals, VHWO and Other NPEDocument44 pagesPrivate Nor-for-Profit Entities (NPE) : Colleges and Universities, Hospitals, VHWO and Other NPEYuvia KeithleyreNo ratings yet

- (Academic Review and Training School, Inc.) 2F & 3F Crème BLDG., Abella ST., Naga City Tel No.: (054) 472-9104 E-Mail: - Inventory (Pas 2)Document10 pages(Academic Review and Training School, Inc.) 2F & 3F Crème BLDG., Abella ST., Naga City Tel No.: (054) 472-9104 E-Mail: - Inventory (Pas 2)Snow TurnerNo ratings yet

- Seatwork Income MaDocument3 pagesSeatwork Income MaJoyce Ann Agdippa Barcelona0% (1)

- Answer The Following With Speed and Accuracy. Solutions Must Be DisclosedDocument4 pagesAnswer The Following With Speed and Accuracy. Solutions Must Be DisclosedUNKNOWNNNo ratings yet

- Auditing ProblemsDocument11 pagesAuditing ProblemslisaNo ratings yet

- 3.3 - Bank Reconciliation and Proof of CashDocument5 pages3.3 - Bank Reconciliation and Proof of CashxxxNo ratings yet

- Problems CCEDocument10 pagesProblems CCERafael Renz DayaoNo ratings yet

- Quiz Module 1 FINALDocument4 pagesQuiz Module 1 FINALeia aieNo ratings yet

- HANDOUT - CASH AND CASH EQUIVALENTS - Inclusions and ExclusionsDocument4 pagesHANDOUT - CASH AND CASH EQUIVALENTS - Inclusions and ExclusionsKAYLA SHANE GONZALESNo ratings yet

- M12 Bade 9418 04 Ch10aDocument16 pagesM12 Bade 9418 04 Ch10aVanny Van Sneidjer100% (2)

- Rikesh - Fix Pay All GR With Today GRDocument54 pagesRikesh - Fix Pay All GR With Today GRsumitsspot-always403260% (5)

- Topic: Depreciation (Cost of Machine) Made by Sir Hyder AliDocument4 pagesTopic: Depreciation (Cost of Machine) Made by Sir Hyder AliHaroon KhatriNo ratings yet

- 7.stpi & SezDocument3 pages7.stpi & SezmercatuzNo ratings yet

- Barangay Full Disclosure Monitoring Form NoDocument1 pageBarangay Full Disclosure Monitoring Form NoOmar Dizon100% (1)

- Chapter 03, Modern Advanced Accounting-Review Q & ExrDocument35 pagesChapter 03, Modern Advanced Accounting-Review Q & Exrrlg481483% (12)

- Bdo Loan FormDocument4 pagesBdo Loan FormChristineNo ratings yet

- Organizational Analysis PaperDocument27 pagesOrganizational Analysis PaperMinghui Wang100% (3)

- Exercise 17.11 SolutionDocument3 pagesExercise 17.11 Solutionraphaelrachel100% (1)

- Creditors Reconciliation QuestionDocument2 pagesCreditors Reconciliation QuestionShweta SinghNo ratings yet

- Chapter 1 - Sample Problem IIDocument1 pageChapter 1 - Sample Problem IINorhanima A. MamarintaNo ratings yet

- Engleza Lucru IndividualDocument2 pagesEngleza Lucru IndividualElena GutcanNo ratings yet

- Income Statement Vertical Analysis TemplateDocument2 pagesIncome Statement Vertical Analysis TemplateArif RahmanNo ratings yet

- Green Delta Mutual Fund: Bank Code Br. Code Bank & Branch NameDocument8 pagesGreen Delta Mutual Fund: Bank Code Br. Code Bank & Branch NameboipagolNo ratings yet

- Attachments To Suhay Cash Position 2021-08-002Document42 pagesAttachments To Suhay Cash Position 2021-08-002Eloiza Lajara RamosNo ratings yet

- Balace SheetDocument4 pagesBalace SheetManoj A GNo ratings yet

- Problem Quizzes 3 4 5Document9 pagesProblem Quizzes 3 4 5Marjorie Palma0% (1)

- Cambridge International General Certificate of Secondary EducationDocument20 pagesCambridge International General Certificate of Secondary EducationSuba ChaluNo ratings yet

- Loan Agreement (Rev. 1339ED7)Document5 pagesLoan Agreement (Rev. 1339ED7)KrisNo ratings yet

- Aplicación de Las Matemáticas FinancierasDocument8 pagesAplicación de Las Matemáticas FinancierasJhonatan GrisalesNo ratings yet

- Control Account NotesDocument2 pagesControl Account NotesNipuni PereraNo ratings yet

- Tybfm Sem6 VcpeDocument47 pagesTybfm Sem6 VcpeLeo Bogosi MotlogelwNo ratings yet

- Sequences and Series Practice QuestionsDocument6 pagesSequences and Series Practice QuestionsjamesNo ratings yet

- People of The Philippines Vs Sandiganbayan and Bienvenido TanDocument2 pagesPeople of The Philippines Vs Sandiganbayan and Bienvenido TanRobyAnneLimbitcoAlbarracin100% (2)

- Variable Costing: A Tool For ManagementDocument34 pagesVariable Costing: A Tool For ManagementSohaib ArifNo ratings yet