TDS Under Section 194C: Press Releases Blog Posts

TDS Under Section 194C: Press Releases Blog Posts

Download as pdf or txt

You might also like

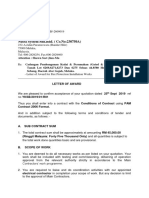

- Letter of Award Nutra System SDN BHDDocument4 pagesLetter of Award Nutra System SDN BHDTun Nazie89% (9)

- Ease of Paying TaxesDocument2 pagesEase of Paying TaxesLET ReviewerNo ratings yet

- RR 13-00Document2 pagesRR 13-00saintkarri100% (2)

- 'Case Study Decision (Prove & State Format) SampleDocument3 pages'Case Study Decision (Prove & State Format) SampleBobbyNichols100% (1)

- New Section 194Q Applicable From 1.7.2021Document14 pagesNew Section 194Q Applicable From 1.7.2021ramanmaharishiNo ratings yet

- Section 194M of Income Tax ActDocument2 pagesSection 194M of Income Tax ActPrabhath Sharma GantiNo ratings yet

- BFT_Minimum-Chargeable-Income_DBDocument1 pageBFT_Minimum-Chargeable-Income_DByeshmmm1234No ratings yet

- Expectations From Union Budget 2016Document8 pagesExpectations From Union Budget 2016Taxmann PublicationNo ratings yet

- NMIMS - Session 4 - Withholding Taxes TDS and TCS On Sale of Goods Software TaxationDocument49 pagesNMIMS - Session 4 - Withholding Taxes TDS and TCS On Sale of Goods Software TaxationSachin KandloorNo ratings yet

- TDS-and-TCS-provisions-under-the-Income-Tax-dt-18-11-2023Document75 pagesTDS-and-TCS-provisions-under-the-Income-Tax-dt-18-11-2023Tom VarrunNo ratings yet

- Finance Act 2024 Tax MeasuresDocument46 pagesFinance Act 2024 Tax Measuresetudiant etudiantsNo ratings yet

- Crowe Tax Handbook 2024Document76 pagesCrowe Tax Handbook 2024muhammadasif9720021No ratings yet

- Original 1732080196 FAME PPT Final 19.11.2024Document57 pagesOriginal 1732080196 FAME PPT Final 19.11.2024cavivekmehra95No ratings yet

- General Principles CasesDocument294 pagesGeneral Principles CasesAnne OcampoNo ratings yet

- BIR Clarification On 8%Document10 pagesBIR Clarification On 8%FABURRITO FOOD GROUP INCNo ratings yet

- All About New TDS Section 194R and Section 194SDocument8 pagesAll About New TDS Section 194R and Section 194SGauravNo ratings yet

- 20238-2000-Implementing Section 34 B of The Tax Code Of20211213-11-1kbooi9Document5 pages20238-2000-Implementing Section 34 B of The Tax Code Of20211213-11-1kbooi9Ramos Claude VinzonNo ratings yet

- Nov 2019Document39 pagesNov 2019amitha g.sNo ratings yet

- Republic Act No. 11976 (EOPT) - Infographics - SGVDocument3 pagesRepublic Act No. 11976 (EOPT) - Infographics - SGVAlbert SantiagoNo ratings yet

- All About New TDS Section 194R and Section 194S - Taxguru - inDocument7 pagesAll About New TDS Section 194R and Section 194S - Taxguru - inParag Jain DugarNo ratings yet

- Cleartax in s Steps Claim Interest Home Loan DeductionDocument6 pagesCleartax in s Steps Claim Interest Home Loan DeductionmohangboxNo ratings yet

- Charlwin Lee Cup NFJPIA NCR Taxation Questions Elimination RoundDocument26 pagesCharlwin Lee Cup NFJPIA NCR Taxation Questions Elimination RoundKenneth RobledoNo ratings yet

- RR No. 13-2000 - Interest RegulationsDocument7 pagesRR No. 13-2000 - Interest RegulationsHershey GabiNo ratings yet

- Interest Expense - RR No. 13-00Document8 pagesInterest Expense - RR No. 13-00美流No ratings yet

- Tax RTP 2019 PDFDocument40 pagesTax RTP 2019 PDFvenkateshNo ratings yet

- 195r-Circular No 12 2022Document7 pages195r-Circular No 12 2022DEVA1985No ratings yet

- Direct Tax Proposals 2019 (No. 2) - 1Document16 pagesDirect Tax Proposals 2019 (No. 2) - 1Namita Agarwal KediaNo ratings yet

- GNGDRHPDEC142024_20241214122739-112-191Document80 pagesGNGDRHPDEC142024_20241214122739-112-191Sahil GuptaNo ratings yet

- Overview of Input Tax Credit: CMA Arindam GoswamiDocument4 pagesOverview of Input Tax Credit: CMA Arindam Goswamiharshadaphandge165No ratings yet

- 53993bos43369interrtpmay19 p4 PDFDocument40 pages53993bos43369interrtpmay19 p4 PDFsaurabh feteNo ratings yet

- Tds Amendements Via Finance Bill 2020Document12 pagesTds Amendements Via Finance Bill 2020ABHISHEKNo ratings yet

- RMC No. 77-2021Document38 pagesRMC No. 77-2021Mike Ferdinand SantosNo ratings yet

- A Brief On Finance Act 2023Document54 pagesA Brief On Finance Act 2023osman.siddiquiNo ratings yet

- 195 Paper With PhotoDocument29 pages195 Paper With Photogrover_deepak18No ratings yet

- Tax Alert-Further Details Released On Omnibus Law Tax TreatmentsDocument18 pagesTax Alert-Further Details Released On Omnibus Law Tax Treatmentsadrianarby27No ratings yet

- Rmo 08-2017 PDFDocument34 pagesRmo 08-2017 PDFJill b.No ratings yet

- Mzalendo Trust Analysis of The Finance Bill 2023 CQMBHGNDocument16 pagesMzalendo Trust Analysis of The Finance Bill 2023 CQMBHGNRaoNo ratings yet

- Taxflash: New Foreign Tax Credit RulesDocument6 pagesTaxflash: New Foreign Tax Credit RulesKojiro FuumaNo ratings yet

- 6 ItcDocument114 pages6 ItcRAUNAQ SHARMANo ratings yet

- B4 Nov MSDocument13 pagesB4 Nov MSCerealis FelicianNo ratings yet

- Shri Paresh Parekh, Chartered Accountants, Partner, Ernst & Young Pvt. LTDDocument46 pagesShri Paresh Parekh, Chartered Accountants, Partner, Ernst & Young Pvt. LTDSridharRaoNo ratings yet

- Circulars/Notifications: Legal UpdateDocument14 pagesCirculars/Notifications: Legal UpdateAnupam BaliNo ratings yet

- Tds GuidelineDocument23 pagesTds GuidelineYash BhayaniNo ratings yet

- 2019 To 2015 TAX BAR Q ADocument87 pages2019 To 2015 TAX BAR Q AJade Ligan EliabNo ratings yet

- INCOMETX PPT(1)Document13 pagesINCOMETX PPT(1)Ankit SinghNo ratings yet

- OL 4 - BLT Study Text Suppliment 2021 - On New Tax AmmendmentsDocument28 pagesOL 4 - BLT Study Text Suppliment 2021 - On New Tax Ammendmentshte19031No ratings yet

- Input Tax Credit: Cma Bibhudatta SarangiDocument3 pagesInput Tax Credit: Cma Bibhudatta SarangihanumanthaiahgowdaNo ratings yet

- Section 194R of Income Tax Act 1961Document5 pagesSection 194R of Income Tax Act 1961madhubhatNo ratings yet

- DT Alert - CBDT Issues Guidelines For Removal of Difficulties On New Withholding Provision On Payment of BusinessDocument9 pagesDT Alert - CBDT Issues Guidelines For Removal of Difficulties On New Withholding Provision On Payment of BusinessGanesh G GageNo ratings yet

- Economic Update 17th May-1Document2 pagesEconomic Update 17th May-1mNo ratings yet

- Ey Budget 2023 Technology SectorDocument6 pagesEy Budget 2023 Technology SectorAditya BajoriaNo ratings yet

- Tax Alert Amend Act 2018Document4 pagesTax Alert Amend Act 2018Vos TeeNo ratings yet

- CIR vs. CA - G.R. No. 125355 (Digest)Document7 pagesCIR vs. CA - G.R. No. 125355 (Digest)Karen Gina DupraNo ratings yet

- Advance Learning On TDS Under Section 194-I and 194-C: MeaningDocument52 pagesAdvance Learning On TDS Under Section 194-I and 194-C: MeaningTejTejuNo ratings yet

- Circular No 12 2022Document7 pagesCircular No 12 2022shantXNo ratings yet

- 195 BCA PresentationDocument36 pages195 BCA PresentationCA Sagar WaghNo ratings yet

- BIR Updates Issue No. 2Document2 pagesBIR Updates Issue No. 2Jy GoNo ratings yet

- An Analysis On Applicability of Reverse Charge Mechanism Under GST On Reimbursement of Expats Salary Outside IndiaDocument3 pagesAn Analysis On Applicability of Reverse Charge Mechanism Under GST On Reimbursement of Expats Salary Outside Indiasanjana sethNo ratings yet

- Circular 17 2020Document4 pagesCircular 17 2020Moneylife FoundationNo ratings yet

- 5891suggested Answer Tax PL March-April2024Document20 pages5891suggested Answer Tax PL March-April2024Raziur RahmanNo ratings yet

- Income Compilation Tax ReviewDocument13 pagesIncome Compilation Tax ReviewJosiebethAzueloNo ratings yet

- 07 07 2021Document9 pages07 07 2021Balu Mahendra SusarlaNo ratings yet

- GORT46Document3 pagesGORT46Balu Mahendra SusarlaNo ratings yet

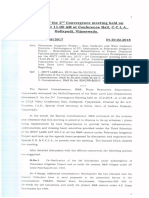

- 1st State Convengence MeetingDocument12 pages1st State Convengence MeetingBalu Mahendra SusarlaNo ratings yet

- Board Election Nomination FormDocument4 pagesBoard Election Nomination FormBalu Mahendra SusarlaNo ratings yet

- 2nd State Convengence MeetingDocument8 pages2nd State Convengence MeetingBalu Mahendra SusarlaNo ratings yet

- Iit 5th RoundDocument26 pagesIit 5th RoundBalu Mahendra SusarlaNo ratings yet

- CEA Reimbursement FormatDocument4 pagesCEA Reimbursement FormatBalu Mahendra SusarlaNo ratings yet

- DA GoDocument6 pagesDA GoBalu Mahendra SusarlaNo ratings yet

- 685Document4 pages685Balu Mahendra SusarlaNo ratings yet

- CMRFDocument2 pagesCMRFBalu Mahendra SusarlaNo ratings yet

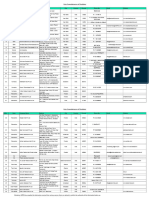

- S O U T H C E N T R A L: List of LIC Offices For Servicing of PMJDY ClaimDocument23 pagesS O U T H C E N T R A L: List of LIC Offices For Servicing of PMJDY ClaimBalu Mahendra SusarlaNo ratings yet

- 07 - Chapter 2 PDFDocument58 pages07 - Chapter 2 PDFBalu Mahendra SusarlaNo ratings yet

- 2017hou RT4Document1 page2017hou RT4Balu Mahendra SusarlaNo ratings yet

- Government of Andhra PradeshDocument2 pagesGovernment of Andhra PradeshBalu Mahendra SusarlaNo ratings yet

- 2017se RT84Document1 page2017se RT84Balu Mahendra SusarlaNo ratings yet

- Volume VII 1 PDFDocument322 pagesVolume VII 1 PDFBalu Mahendra SusarlaNo ratings yet

- 2018maud RT1047 PDFDocument2 pages2018maud RT1047 PDFBalu Mahendra SusarlaNo ratings yet

- 2016HMF RT268Document1 page2016HMF RT268Balu Mahendra SusarlaNo ratings yet

- Annual Rep 2007 08Document444 pagesAnnual Rep 2007 08maurya111No ratings yet

- I Puc-Business Studies-2017-18 SECTION-E (Practical Oriented Questions and Answers:)Document5 pagesI Puc-Business Studies-2017-18 SECTION-E (Practical Oriented Questions and Answers:)Vikas R Gaddale88% (26)

- The Entrepreneurial Mind AY2022 2023 BEED I PIAGET Final ExaminationDocument9 pagesThe Entrepreneurial Mind AY2022 2023 BEED I PIAGET Final ExaminationRyan SulivasNo ratings yet

- State: ODISHA: T. of India Evelopment VelopmentDocument51 pagesState: ODISHA: T. of India Evelopment Velopmentnpbehera143No ratings yet

- Gipsy Kings Medley - Trumpet in BB 1.0Document3 pagesGipsy Kings Medley - Trumpet in BB 1.0Settimio SavioliNo ratings yet

- Havells CSR IA 2021-20Document7 pagesHavells CSR IA 2021-20Anuja GupteNo ratings yet

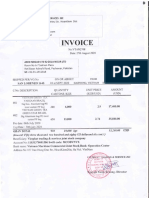

- JioMart Invoice 16664559950435989A 1Document2 pagesJioMart Invoice 16664559950435989A 1saurabhbisht1996No ratings yet

- Percentage of An Amount Calculator PDFDocument11 pagesPercentage of An Amount Calculator PDFDivaNo ratings yet

- M, Zoro: in The United Bankruptcy Court The District Delaware in Mervyn'S Holdings, (KG) JointlyDocument4 pagesM, Zoro: in The United Bankruptcy Court The District Delaware in Mervyn'S Holdings, (KG) JointlyChapter 11 DocketsNo ratings yet

- List of Vantilators Manufacturers 13.04.2020Document2 pagesList of Vantilators Manufacturers 13.04.2020uniquecalibrationservicesNo ratings yet

- OSP#16078878Document6 pagesOSP#16078878Guhanadh PadarthyNo ratings yet

- Economic Impact of Covid-19 in The Philippines: Fact File 2020Document26 pagesEconomic Impact of Covid-19 in The Philippines: Fact File 2020Girlee Jhene CadeliñaNo ratings yet

- Sample Business Registration FormDocument4 pagesSample Business Registration FormErwin De RamaNo ratings yet

- Job Sharing N FlexitimeDocument12 pagesJob Sharing N FlexitimeahmadnaimzaidNo ratings yet

- Analysis of Competitiveness of Azerbaijan Persimmon Export in The International MarketDocument6 pagesAnalysis of Competitiveness of Azerbaijan Persimmon Export in The International MarketInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Indian Forest Service: Gradation ListDocument16 pagesIndian Forest Service: Gradation Listhiteshrajput2142No ratings yet

- Pop IntroDocument8 pagesPop IntroSaurabh MundraNo ratings yet

- Cashflow Income Statement Rat RaceDocument1 pageCashflow Income Statement Rat RaceWerner van LoonNo ratings yet

- Chapter 15 Closing Case OverviewDocument14 pagesChapter 15 Closing Case OverviewNitish BhardwajNo ratings yet

- InvoiceDocument1 pageInvoiceNgọc BộpNo ratings yet

- Ratio Analysis Report Atlas Battery LTDDocument8 pagesRatio Analysis Report Atlas Battery LTDAnushayNo ratings yet

- BIT INFO NEPAL - Economics - ECO155-2078Document2 pagesBIT INFO NEPAL - Economics - ECO155-2078meropriyaaNo ratings yet

- Mip Package 01 - Offshore Gosp-4 Development: Piping Support Standard - CommonDocument296 pagesMip Package 01 - Offshore Gosp-4 Development: Piping Support Standard - CommonHariharan MNo ratings yet

- American Investor May 2011Document19 pagesAmerican Investor May 2011American Chamber of Commerce in Poland, Kraków Branch / Amerykańska Izba Handlowa w Polsce. Oddział w KrakowieNo ratings yet

- Backtesting of USD JPYDocument45 pagesBacktesting of USD JPYKoustav S MandalNo ratings yet

- Final Presentation TelenorDocument52 pagesFinal Presentation TelenorMuhammad USMAN100% (11)

- Questions OnlyDocument4 pagesQuestions Onlyapi-529669983No ratings yet

- Pest Analysis For AustraliaDocument6 pagesPest Analysis For AustraliaTarun UraiyaNo ratings yet