Chapter 7 Workout Sheet

Chapter 7 Workout Sheet

Download as docx, pdf, or txt

You might also like

- Essentials of Investments 12th Edition Zvi Bodie Alex Kane Alan J Marcus 2Document35 pagesEssentials of Investments 12th Edition Zvi Bodie Alex Kane Alan J Marcus 2reyaelcharifNo ratings yet

- Particulars MSFT 3 Year 5 Year 10 Year 30 YearDocument2 pagesParticulars MSFT 3 Year 5 Year 10 Year 30 YearAsad BilalNo ratings yet

- Bubble and Bee Lecture TemplateDocument2 pagesBubble and Bee Lecture TemplateMavin JeraldNo ratings yet

- Dyson V15 Detect User ManualDocument14 pagesDyson V15 Detect User ManualXiaoyu HuangNo ratings yet

- BOEING 7e7Document5 pagesBOEING 7e7EVA Rental AdminNo ratings yet

- Question BankDocument3 pagesQuestion BankDivya P Gadaria100% (1)

- A Simple Guide To Registering A Corporation in The PhilippinesDocument5 pagesA Simple Guide To Registering A Corporation in The PhilippinesAike SadjailNo ratings yet

- Radent Case QuestionsDocument2 pagesRadent Case QuestionsmahieNo ratings yet

- This Study Resource WasDocument9 pagesThis Study Resource WasVishalNo ratings yet

- Mother - Please Speak Out: Income Statement For The Year Ended March 31, 2019 ($000s) Net Sales 100,000Document3 pagesMother - Please Speak Out: Income Statement For The Year Ended March 31, 2019 ($000s) Net Sales 100,000Jayash Kaushal0% (2)

- Section A - Group DDocument6 pagesSection A - Group DAbhishek Verma100% (1)

- C19a Rio's SpreadsheetDocument8 pagesC19a Rio's SpreadsheetaluiscgNo ratings yet

- Lease and Sales & LeasebackDocument4 pagesLease and Sales & LeasebackSandeep Agrawal100% (1)

- Intrinsic Stock Value FCFF On JNJ StockDocument6 pagesIntrinsic Stock Value FCFF On JNJ Stockviettuan91No ratings yet

- Super 8 Motel Guelph - Excel Model To Use For The Write-UpDocument11 pagesSuper 8 Motel Guelph - Excel Model To Use For The Write-UpNarinderNo ratings yet

- General Mills PillsburyDocument8 pagesGeneral Mills PillsburyteenabansalNo ratings yet

- Case: Flash Memory, Inc. (4232)Document1 pageCase: Flash Memory, Inc. (4232)陳子奕No ratings yet

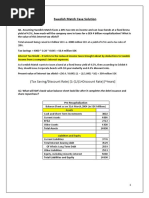

- Swedish Match Case SolutionDocument5 pagesSwedish Match Case SolutionKaran AggarwalNo ratings yet

- Case 32 - CPK AssignmentDocument9 pagesCase 32 - CPK AssignmentEli JohnsonNo ratings yet

- Shapiro CHAPTER 6 SolutionsDocument10 pagesShapiro CHAPTER 6 SolutionsjzdoogNo ratings yet

- Palmer Limited Case StudyDocument9 pagesPalmer Limited Case StudyPrashil Raj MehtaNo ratings yet

- Flash Memory Case Study Solution PDF FreeDocument8 pagesFlash Memory Case Study Solution PDF FreeBreda RunNo ratings yet

- PROG8520 - Week 10 - SlidesDocument96 pagesPROG8520 - Week 10 - Slidessimran sidhuNo ratings yet

- 5037asd8876 HKDADocument4 pages5037asd8876 HKDAdaedric13100% (1)

- PROG8520 - Week 9 - SlidesDocument43 pagesPROG8520 - Week 9 - Slidessimran sidhuNo ratings yet

- Bacia de CamposDocument7 pagesBacia de CampospoisonboxNo ratings yet

- ITC Financial ModelDocument75 pagesITC Financial ModelANH PHAM QUYNHNo ratings yet

- Mercury Athletic FootwearDocument4 pagesMercury Athletic FootwearAbhishek KumarNo ratings yet

- Case 5: Merger Analysis Computer Concepts/computechDocument9 pagesCase 5: Merger Analysis Computer Concepts/computechLouis De MoffartsNo ratings yet

- M&a Assignment - Syndicate C FINALDocument8 pagesM&a Assignment - Syndicate C FINALNikhil ReddyNo ratings yet

- Sampa Video Solution Harvard Case Solution 1Document10 pagesSampa Video Solution Harvard Case Solution 1Héctor SilvaNo ratings yet

- Case Study 2Document21 pagesCase Study 2karimNo ratings yet

- Current Ratio: Current Liabilities Quick Ratio: Current LiabilitiesDocument4 pagesCurrent Ratio: Current Liabilities Quick Ratio: Current LiabilitiesAdityaSharmaNo ratings yet

- Case 35 Deluxe CorporationDocument16 pagesCase 35 Deluxe CorporationSajjad Ahmad100% (1)

- Hello GunaDocument10 pagesHello GunaMajed Abou AlkhirNo ratings yet

- Mercury Athletic QuestionsDocument1 pageMercury Athletic QuestionsRazi UllahNo ratings yet

- FM Unit 2 Tutorial - Finanacial Statement Analysis Revised 2019Document4 pagesFM Unit 2 Tutorial - Finanacial Statement Analysis Revised 2019Tanice WhyteNo ratings yet

- Air Thread ConnectionsDocument31 pagesAir Thread ConnectionsJasdeep SinghNo ratings yet

- Boston Chicken CaseDocument7 pagesBoston Chicken CaseDji YangNo ratings yet

- Section B Group 4 Assignment BNL StoresDocument3 pagesSection B Group 4 Assignment BNL StoresMohit VermaNo ratings yet

- UVA-F-1264: Printicomm's Proposed Acquisition of Digitech: Negotiating Price and Form of PaymentDocument14 pagesUVA-F-1264: Printicomm's Proposed Acquisition of Digitech: Negotiating Price and Form of PaymentKumarNo ratings yet

- BBBY S CaseDocument4 pagesBBBY S CaseKarina Taype NunuraNo ratings yet

- Hilton 13e SM Ch07Document72 pagesHilton 13e SM Ch07tttNo ratings yet

- Airthread Acquisition Operating AssumptionsDocument27 pagesAirthread Acquisition Operating AssumptionsnidhidNo ratings yet

- Mercury Athletic CaseDocument3 pagesMercury Athletic Casekrishnakumar rNo ratings yet

- Tata Corus Acquisition and M&ADocument16 pagesTata Corus Acquisition and M&ASaurabh PaliwalNo ratings yet

- DeltaDocument5 pagesDeltahajarzamriNo ratings yet

- Nagornov Super Project CaseDocument3 pagesNagornov Super Project Casetbsssilva100% (1)

- AppleDocument12 pagesAppleVeni GuptaNo ratings yet

- Seagate NewDocument22 pagesSeagate NewKaran VasheeNo ratings yet

- Final AssignmentDocument15 pagesFinal AssignmentUttam DwaNo ratings yet

- Sampa VideoDocument24 pagesSampa VideodoiNo ratings yet

- Flash MemoryDocument8 pagesFlash Memoryranjitd07No ratings yet

- BNL StoresDocument4 pagesBNL Storesshanul gawshindeNo ratings yet

- Projected Balance Sheet: Enter Your Company Name HereDocument1 pageProjected Balance Sheet: Enter Your Company Name Herehim009No ratings yet

- Case 32Document6 pagesCase 32patelnayan22No ratings yet

- Total 621 1749 2544 3300Document6 pagesTotal 621 1749 2544 3300Anupam ChaplotNo ratings yet

- Analisis Super ProjectDocument4 pagesAnalisis Super Projectrcatherineb50% (2)

- 7 - Exotic OptionsDocument39 pages7 - Exotic OptionsAman Kumar SharanNo ratings yet

- Foreign Currency Derivatives and Swaps: QuestionsDocument6 pagesForeign Currency Derivatives and Swaps: QuestionsCarl AzizNo ratings yet

- Derivatives Lecture Notes 1 Part ADocument13 pagesDerivatives Lecture Notes 1 Part Aradhika kumarfNo ratings yet

- Introduction To OptionsDocument9 pagesIntroduction To OptionsKumar NarayananNo ratings yet

- Photo by Sam Ang-SamDocument6 pagesPhoto by Sam Ang-Samanh sy tranNo ratings yet

- Of Information: Anti-Bribery Corruption Candidate Disclosure QuestionsDocument2 pagesOf Information: Anti-Bribery Corruption Candidate Disclosure Questionsanh sy tranNo ratings yet

- JP Comments Andy Fall Social Media Posts5Document5 pagesJP Comments Andy Fall Social Media Posts5anh sy tranNo ratings yet

- Post of Nakatani Gong Orchestra Followed The Master Plan Post 1 (First Intro About Artist Biography)Document5 pagesPost of Nakatani Gong Orchestra Followed The Master Plan Post 1 (First Intro About Artist Biography)anh sy tranNo ratings yet

- FB Shareholder Lawsuit Pretrail Brief UNSEALEDDocument93 pagesFB Shareholder Lawsuit Pretrail Brief UNSEALEDAlex HeathNo ratings yet

- Assignment On Sarbanes Oaxley Act 10Document5 pagesAssignment On Sarbanes Oaxley Act 10Haris MunirNo ratings yet

- Corporate Governance and Director Accountability: An Institutional Comparative PerspectiveDocument15 pagesCorporate Governance and Director Accountability: An Institutional Comparative PerspectiveGHANSHYAMNo ratings yet

- TakeoversDocument9 pagesTakeoversiamfromajmer100% (1)

- Standard Operating Procedure For The Stock Markets BusinessDocument3 pagesStandard Operating Procedure For The Stock Markets Businessankit sinhaNo ratings yet

- Ordinary Share CapitalDocument7 pagesOrdinary Share CapitalKenneth RonoNo ratings yet

- OMI (Actiuni ETF) Tabel de Specificatii - 121020 PDFDocument81 pagesOMI (Actiuni ETF) Tabel de Specificatii - 121020 PDFCiprian AndriciNo ratings yet

- Kinds of PartnershipDocument4 pagesKinds of PartnershipIrvinne Heather Chua GoNo ratings yet

- عرض و تحليل القوائم الماليةDocument16 pagesعرض و تحليل القوائم الماليةRym BoucheritNo ratings yet

- AOI Group 1 Edited 4Document23 pagesAOI Group 1 Edited 4Kat RANo ratings yet

- Unit 5: Company LawDocument4 pagesUnit 5: Company LawDiệp Quỳnh TrầnNo ratings yet

- NG NOCLARDocument2 pagesNG NOCLARKathleen MarcialNo ratings yet

- 201.06 Accounting For Insurance Companies (IAS-1, IfRS-4)Document6 pages201.06 Accounting For Insurance Companies (IAS-1, IfRS-4)Biplob K. SannyasiNo ratings yet

- Mergers and Acquisitions The Evolving Indian Landscape PDFDocument52 pagesMergers and Acquisitions The Evolving Indian Landscape PDFAmitmil MbbsNo ratings yet

- G.R. No. L-45911 - Gokongwei, Jr. v. Securities and ExchangeDocument46 pagesG.R. No. L-45911 - Gokongwei, Jr. v. Securities and ExchangeKaren Gina DupraNo ratings yet

- Articles of PartnershipDocument17 pagesArticles of PartnershipMarycor100% (1)

- Annual Report DSSA 2018 PDFDocument320 pagesAnnual Report DSSA 2018 PDFSudarmadi DmaNo ratings yet

- Chapter 03 Common Takeover Tactics and DefensesDocument18 pagesChapter 03 Common Takeover Tactics and DefensesMohsin GNo ratings yet

- U.S. GAAP vs. IFRS: Impairment of Long-Lived Assets: Prepared byDocument8 pagesU.S. GAAP vs. IFRS: Impairment of Long-Lived Assets: Prepared byChoi TeumeNo ratings yet

- CACYP15 BDocument68 pagesCACYP15 BJoan PinedaNo ratings yet

- Intiland Development Annual Report 2016 Company Profile Indonesia Investments PDFDocument448 pagesIntiland Development Annual Report 2016 Company Profile Indonesia Investments PDFRelawan Commandcenter112No ratings yet

- Chapter Wise Checklist of Company LawDocument17 pagesChapter Wise Checklist of Company LawNitesh Raj SinhaNo ratings yet

- Limited Liability Partnership - Wikipedia PDFDocument51 pagesLimited Liability Partnership - Wikipedia PDFNAVAMY MRNo ratings yet

- HagagaDocument27 pagesHagagaKyla de SilvaNo ratings yet

- Company Law ProjectDocument28 pagesCompany Law ProjectpushpanjaliNo ratings yet

- Corporate Law: By, Sanjana S Bhat 1812033Document16 pagesCorporate Law: By, Sanjana S Bhat 1812033Sanjana BhatNo ratings yet

- Financial Regulation PrimerDocument8 pagesFinancial Regulation Primeraxsinn9016No ratings yet

- IJNRD2212031Document7 pagesIJNRD2212031Romak Roy ChowdhuryNo ratings yet