Assingment - FM - Chestnut

Assingment - FM - Chestnut

Download as docx, pdf, or txt

You might also like

- Study Questions SolutionDocument7 pagesStudy Questions SolutionJessica100% (2)

- Blogging at Bzzagent Case AnalysisDocument6 pagesBlogging at Bzzagent Case AnalysisRavikanth VangalaNo ratings yet

- Tad OMalley Case Analysis Guidelines - Carlos RamosDocument6 pagesTad OMalley Case Analysis Guidelines - Carlos Ramos2202973No ratings yet

- Group6 - Vyaderm PharmaceuticalsDocument7 pagesGroup6 - Vyaderm PharmaceuticalsVaishak AnilNo ratings yet

- MFIN Case Write-UpDocument7 pagesMFIN Case Write-UpUMMUSNUR OZCANNo ratings yet

- Assignment No. - Jaguar HalewoodDocument7 pagesAssignment No. - Jaguar HalewoodChandra Prakash S100% (2)

- Merrill Lynch CaseDocument2 pagesMerrill Lynch CaseHailey Judkins100% (2)

- Kaffee Kostuum - Reco 2Document3 pagesKaffee Kostuum - Reco 2RAGHU MALLEGOWDANo ratings yet

- Stock Up Vs Stock Out - Inventory Management Dilemma at A Moble ClinicDocument9 pagesStock Up Vs Stock Out - Inventory Management Dilemma at A Moble Clinictimesave240100% (1)

- Case 3: BNL StoresDocument16 pagesCase 3: BNL StoresAMBWANI NAREN MAHESHNo ratings yet

- Fie443 2015Document8 pagesFie443 2015jamn1979No ratings yet

- A Study of Cash Management in Banking Sector PDFDocument87 pagesA Study of Cash Management in Banking Sector PDFSakshi JagdaleNo ratings yet

- Morning (6021)Document7 pagesMorning (6021)Twinkle BrownNo ratings yet

- Sun Microsystems Case JasdeepDocument6 pagesSun Microsystems Case JasdeepJasdeep SinghNo ratings yet

- Netflix, Inc.-The Mouse Strikes Back SolutionDocument1 pageNetflix, Inc.-The Mouse Strikes Back SolutionArhamNo ratings yet

- Corp Fin Case 1 NextelDocument5 pagesCorp Fin Case 1 NextelPedro José ZapataNo ratings yet

- Case Study: Midland Energy Resources, IncDocument13 pagesCase Study: Midland Energy Resources, IncMikey MadRatNo ratings yet

- Health Development Corporation Spread Sheet (Sol)Document8 pagesHealth Development Corporation Spread Sheet (Sol)Surya Kant100% (2)

- Vyaderm Caseanalysis PDFDocument6 pagesVyaderm Caseanalysis PDFSahil Azher RashidNo ratings yet

- Zeta MiningDocument2 pagesZeta MiningChandra Prakash SNo ratings yet

- Warren Buffett and GEICO Case StudyDocument18 pagesWarren Buffett and GEICO Case StudyReymond Jude PagcoNo ratings yet

- Chestnut - Ambudheesh, Naina, Shiny, SudhanshuDocument9 pagesChestnut - Ambudheesh, Naina, Shiny, SudhanshuRahul UdainiaNo ratings yet

- Chestnut Foods: Case - 4Document8 pagesChestnut Foods: Case - 4KshitishNo ratings yet

- Sealed Air Corp Case Write Up PDFDocument3 pagesSealed Air Corp Case Write Up PDFRamjiNo ratings yet

- Sampa Video Solution Harvard Case Solution 1Document10 pagesSampa Video Solution Harvard Case Solution 1Héctor SilvaNo ratings yet

- Impairing The Microsoft - Nokia PairingDocument54 pagesImpairing The Microsoft - Nokia Pairingjk kumarNo ratings yet

- AirThread Valuation SheetDocument11 pagesAirThread Valuation SheetAngsuman BhanjdeoNo ratings yet

- Mercury Athletic CaseDocument3 pagesMercury Athletic Casekrishnakumar rNo ratings yet

- M&a Assignment - Syndicate C FINALDocument8 pagesM&a Assignment - Syndicate C FINALNikhil ReddyNo ratings yet

- Kohler Case StudyDocument13 pagesKohler Case StudySambashiva Srisailapathy50% (2)

- Green Bonds - Itau BBA FrameworkDocument36 pagesGreen Bonds - Itau BBA FrameworkAndre d'AlvaNo ratings yet

- Case Study Que of AirthreadDocument1 pageCase Study Que of AirthreadSimran MalhotraNo ratings yet

- Stand-Alone Valuation (Dollars in Millions) : PPG Industries Metric Actual Projected 2011 2012E 2013EDocument4 pagesStand-Alone Valuation (Dollars in Millions) : PPG Industries Metric Actual Projected 2011 2012E 2013EStefanny cardonaNo ratings yet

- Diamond 5 Page Report PDFDocument6 pagesDiamond 5 Page Report PDFSudhanva VasishtNo ratings yet

- Reinventing A Giant Corporation: The Case of Tata SteelDocument16 pagesReinventing A Giant Corporation: The Case of Tata Steel20PGPIB064AKSHAR PANDYANo ratings yet

- Valuation of Airthread Connections Questions TraductionDocument2 pagesValuation of Airthread Connections Questions TraductionNatalia HernandezNo ratings yet

- Mercury Athletic FootwearDocument4 pagesMercury Athletic FootwearAbhishek KumarNo ratings yet

- Case Study of Haidilao (HDL) International Holding Co. LimitedDocument7 pagesCase Study of Haidilao (HDL) International Holding Co. LimitedANH DINH NGOCNo ratings yet

- PGPF - 01 - 017 - CV - Assignment - 5 - Keshav v1Document26 pagesPGPF - 01 - 017 - CV - Assignment - 5 - Keshav v1nidhidNo ratings yet

- Carter LBODocument1 pageCarter LBOEddie KruleNo ratings yet

- New Heritage Doll CompanyDocument4 pagesNew Heritage Doll Companyvenom_ftwNo ratings yet

- Lex Service PLC - Cost of Capital1Document4 pagesLex Service PLC - Cost of Capital1Ravi VatsaNo ratings yet

- Ludhiana City Bus Service-Muhammad Rafeeq-MBA-12577Document4 pagesLudhiana City Bus Service-Muhammad Rafeeq-MBA-12577Muhammad Rafeeq100% (1)

- ATC Case SolutionDocument3 pagesATC Case SolutionAbiNo ratings yet

- Booz Allen Case StudyDocument4 pagesBooz Allen Case StudysmitaNo ratings yet

- Leveraged Recapitalizations and Exchange OffersDocument5 pagesLeveraged Recapitalizations and Exchange OffersAfiaSiddiquiNo ratings yet

- Asahi Exercise Filled in For All - Group 8Document6 pagesAsahi Exercise Filled in For All - Group 8Ritika SharmaNo ratings yet

- Case 5 Midland Energy Case ProjectDocument7 pagesCase 5 Midland Energy Case ProjectCourse HeroNo ratings yet

- Problem Set 2 3 4 Or-2Document5 pagesProblem Set 2 3 4 Or-2Ryan Jeffrey Padua Curbano100% (1)

- Why Is Soft Drink Industry So Profitable?: Barriers To EntryDocument3 pagesWhy Is Soft Drink Industry So Profitable?: Barriers To EntryVenkatesh BoddepalliNo ratings yet

- Fashion - Point SolutionDocument4 pagesFashion - Point SolutionMuhammad JunaidNo ratings yet

- DocxDocument16 pagesDocxDeepika PadukoneNo ratings yet

- Case - Study - Leader As A CoachDocument5 pagesCase - Study - Leader As A Coachjemilart4realNo ratings yet

- Excel Spreadsheet Sampa VideoDocument5 pagesExcel Spreadsheet Sampa VideoFaith AllenNo ratings yet

- Case Nobody Ever DisagreesDocument4 pagesCase Nobody Ever DisagreesChinmay PrustyNo ratings yet

- Glaxo ItaliaDocument11 pagesGlaxo ItaliaLizeth RamirezNo ratings yet

- The Mexico-China Sourcing Game: Teaching Global Dual SourcingDocument8 pagesThe Mexico-China Sourcing Game: Teaching Global Dual SourcingSachin PhadkeNo ratings yet

- Emerging Business Oportunities - Section2 Group 1Document25 pagesEmerging Business Oportunities - Section2 Group 1Rishabh KothariNo ratings yet

- Ow To LAY: Finance Simulation: Capital BudgetingDocument10 pagesOw To LAY: Finance Simulation: Capital BudgetingApoorv GuptaNo ratings yet

- Sealed Air Corporation v1.0Document8 pagesSealed Air Corporation v1.0KshitishNo ratings yet

- FBE 529 Lecture 1 PDFDocument26 pagesFBE 529 Lecture 1 PDFJIAYUN SHENNo ratings yet

- The Acquisition of Consolidated Rail Corporation (A)Document15 pagesThe Acquisition of Consolidated Rail Corporation (A)Neetesh ThakurNo ratings yet

- Session 10 Simulation Questions PDFDocument6 pagesSession 10 Simulation Questions PDFVAIBHAV WADHWA0% (1)

- Equity Insight On ACI Limited (ACI)Document10 pagesEquity Insight On ACI Limited (ACI)mamunakon933No ratings yet

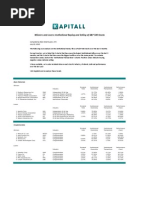

- Winners and Losers - Institutional Buying of SP500 StocksDocument4 pagesWinners and Losers - Institutional Buying of SP500 StocksKapitall ResearchNo ratings yet

- Finalcial Ratio Analysis of Padma Textile MillsDocument25 pagesFinalcial Ratio Analysis of Padma Textile Millsrehan18No ratings yet

- Current Problems Desired State: TechnicalDocument1 pageCurrent Problems Desired State: TechnicalChandra Prakash SNo ratings yet

- Assignment Halewood R2Document4 pagesAssignment Halewood R2Chandra Prakash SNo ratings yet

- Halewood-Current State and The Need For Change?: TechnicalDocument1 pageHalewood-Current State and The Need For Change?: TechnicalChandra Prakash SNo ratings yet

- EOQ Assumptions: EPL Model Relaxes This OneDocument14 pagesEOQ Assumptions: EPL Model Relaxes This OneChandra Prakash SNo ratings yet

- X Residual Plot: Regression StatisticsDocument7 pagesX Residual Plot: Regression StatisticsChandra Prakash SNo ratings yet

- Bank Data Analysis ReportDocument14 pagesBank Data Analysis ReportChandra Prakash SNo ratings yet

- CGT19011 Formatting AssignmentDocument22 pagesCGT19011 Formatting AssignmentChandra Prakash SNo ratings yet

- Security Analysis and Port Folio Management: Question Bank (5years) 2 MarksDocument7 pagesSecurity Analysis and Port Folio Management: Question Bank (5years) 2 MarksVignesh Narayanan100% (1)

- Amalgamation of Companies: Sushil KumarDocument49 pagesAmalgamation of Companies: Sushil KumarSundaramNo ratings yet

- Climate Finance: Engaging The Private SectorDocument32 pagesClimate Finance: Engaging The Private SectorIFC SustainabilityNo ratings yet

- New Microsoft Word DocumentDocument4 pagesNew Microsoft Word Documentමිලන්No ratings yet

- Undergrad Student Investment Banking Resume TemplateDocument3 pagesUndergrad Student Investment Banking Resume TemplateMike MillerNo ratings yet

- Final TaxDocument1 pageFinal TaxEun Ice0% (3)

- JSL ListingDocument267 pagesJSL ListingsudhakarrrrrrNo ratings yet

- Quiz - Consolidated FS Part 2Document3 pagesQuiz - Consolidated FS Part 2skyieNo ratings yet

- Cost of Capital: Courses Offered: Rbi Grade B Sebi Grade A Nabard Grade A Ugc Net/JrfDocument10 pagesCost of Capital: Courses Offered: Rbi Grade B Sebi Grade A Nabard Grade A Ugc Net/JrframNo ratings yet

- Ilovepdf MergedDocument25 pagesIlovepdf Mergedbabysharkdoodoo2808No ratings yet

- Private Equity in India MbaDocument94 pagesPrivate Equity in India MbaHOME 4No ratings yet

- The Business, Tax, and Financial EnvironmentsDocument38 pagesThe Business, Tax, and Financial EnvironmentsNaveed AhmadNo ratings yet

- A Study On DerivativesDocument70 pagesA Study On DerivativesDivya Kakran100% (3)

- Wiley Cash FlowDocument6 pagesWiley Cash FlowkimmynotNo ratings yet

- E-Pioneer Entrepreneur Fund ePEF) : Public (PDocument2 pagesE-Pioneer Entrepreneur Fund ePEF) : Public (Pshairazi sarbiNo ratings yet

- Derivatives Shahid A. ZiaDocument42 pagesDerivatives Shahid A. ZiaAlizay KhanNo ratings yet

- Response To Comments On Sh. Ashish Gupta MemorandumDocument5 pagesResponse To Comments On Sh. Ashish Gupta MemorandumShaurya SinghNo ratings yet

- Maf603 Pya Coc - July 21Document2 pagesMaf603 Pya Coc - July 21WAN MOHAMAD ANAS WAN MOHAMADNo ratings yet

- The Intelligent Investor-FinalDocument25 pagesThe Intelligent Investor-Finalshethiren8832No ratings yet

- ClearStationEducation PDFDocument149 pagesClearStationEducation PDFTookiePieNo ratings yet

- MR ZulfaDocument14 pagesMR ZulfaHalim Pandu LatifahNo ratings yet

- Business Math Term PaperDocument8 pagesBusiness Math Term PaperImraan Deepay HasanNo ratings yet

- 2nd Midterm Quiz Assignment QuestionnaireDocument6 pages2nd Midterm Quiz Assignment QuestionnaireAthena Fatmah AmpuanNo ratings yet

- JPM The J P Morgan View 2022-05-09 4086002Document57 pagesJPM The J P Morgan View 2022-05-09 4086002Kurt ZhangNo ratings yet

- European PDFDocument109 pagesEuropean PDFNuno Couto0% (1)

- Introduction To Retail BankingDocument27 pagesIntroduction To Retail BankingMitesh Dharamwani83% (6)