Sample Exam Paper With Answers PDF

Sample Exam Paper With Answers PDF

Download as pdf or txt

You might also like

- B Unit-DU Model Test-01 & 02 MCQ, Written SolutionDocument14 pagesB Unit-DU Model Test-01 & 02 MCQ, Written SolutionT Rdtfr100% (2)

- Basic Shop Processes Tools and Equipments: Prepare By: Rekhnor S. MagbanuaDocument25 pagesBasic Shop Processes Tools and Equipments: Prepare By: Rekhnor S. Magbanuarekhnor magbanuaNo ratings yet

- Name (Optional) : - Age: - Gender: - Direction: Put Check ( ) On The Following Spaces Accordingly To Help Assess Our Feasibility Study EntitledDocument2 pagesName (Optional) : - Age: - Gender: - Direction: Put Check ( ) On The Following Spaces Accordingly To Help Assess Our Feasibility Study EntitledJem ValmonteNo ratings yet

- IT 112 (Office Productivity) Course SyllabusDocument6 pagesIT 112 (Office Productivity) Course SyllabusZeroCodeNo ratings yet

- Academic Predictors of The Licensure Examination For Teachers' Performance of The Rizal Technological University Teacher Education GraduatesDocument10 pagesAcademic Predictors of The Licensure Examination For Teachers' Performance of The Rizal Technological University Teacher Education Graduates15-0001No ratings yet

- Surigao Del Sur State University Cantilan Campus The Problem and Its SettingDocument12 pagesSurigao Del Sur State University Cantilan Campus The Problem and Its SettingJose CalipayanNo ratings yet

- Input Output Process: Conceptual FrameworkDocument3 pagesInput Output Process: Conceptual FrameworkWebsenseiNo ratings yet

- I-Arnis Ground Rules (International Tournament 2015)Document7 pagesI-Arnis Ground Rules (International Tournament 2015)Marlon ManaliliNo ratings yet

- Learning Task 6: Using The Approaches, Guidelines, and Types of Data Collection Instruments, Create A DraftDocument6 pagesLearning Task 6: Using The Approaches, Guidelines, and Types of Data Collection Instruments, Create A DraftCath QuartoNo ratings yet

- Communications, Networks, & Cyberthreats: Presented by Satriyo AdhyDocument75 pagesCommunications, Networks, & Cyberthreats: Presented by Satriyo AdhyRatri NugraheniNo ratings yet

- Curriculum VitaeDocument3 pagesCurriculum VitaeZi VillarNo ratings yet

- Web Systems and Technologies 1: 2 Semester - SY 2020-2021Document16 pagesWeb Systems and Technologies 1: 2 Semester - SY 2020-2021Masha RosaNo ratings yet

- College of Criminal Justice Education Course OutlineDocument2 pagesCollege of Criminal Justice Education Course OutlineMichelle Maika PalNo ratings yet

- Registry of Trainings AttendedDocument7 pagesRegistry of Trainings AttendedGifsy Robledo CastroNo ratings yet

- Compliance ChecklistDocument2 pagesCompliance ChecklistMik Oliamot100% (1)

- Chapter 2: MethodologyDocument6 pagesChapter 2: MethodologyRicoco MartinNo ratings yet

- Course Syllabus - Methods of ResearchDocument11 pagesCourse Syllabus - Methods of ResearchmarkNo ratings yet

- By Applying GRESA and Dimensional Analysis. Round Off Your Answers To TWO Decimal Places (50 Points)Document15 pagesBy Applying GRESA and Dimensional Analysis. Round Off Your Answers To TWO Decimal Places (50 Points)Joshua FuentesNo ratings yet

- Gen Math - Q2-M8Document28 pagesGen Math - Q2-M8Jasmine L.No ratings yet

- Assessment of Students Satisfaction of Facility S PDFDocument10 pagesAssessment of Students Satisfaction of Facility S PDFAhou Ania Qouma JejaNo ratings yet

- REPUBLIC ACT 7836 (Philippine Teachers Professionalization Act)Document1 pageREPUBLIC ACT 7836 (Philippine Teachers Professionalization Act)Brent TorresNo ratings yet

- Table 1. Weighted Mean Distribution On Respondents' Assessment On Research UsefulnessDocument3 pagesTable 1. Weighted Mean Distribution On Respondents' Assessment On Research UsefulnessDonita-jane Bangilan CanceranNo ratings yet

- CMO 95 S 2017Document21 pagesCMO 95 S 2017Dexter Jonas M. Lumanglas0% (1)

- Personal ObservationsDocument1 pagePersonal ObservationsAshley Dela CruzNo ratings yet

- EMCORDocument13 pagesEMCORDy Ju Arug AL100% (1)

- Psychology Entrance Examination ReviewerDocument11 pagesPsychology Entrance Examination ReviewerLalyn PasaholNo ratings yet

- Dict Application FormDocument1 pageDict Application FormRaul Gutierrez100% (1)

- Anti Loitering Full PaperDocument37 pagesAnti Loitering Full PaperMa TetNo ratings yet

- The Impact of Technology Integration On Student LearningDocument18 pagesThe Impact of Technology Integration On Student LearningRomsan PiamonteNo ratings yet

- Luna Colleges, Inc.: The Impact of Review Centers On The College Examinee'S ConfidenceDocument26 pagesLuna Colleges, Inc.: The Impact of Review Centers On The College Examinee'S ConfidenceApril Abril SalvadorNo ratings yet

- Level of Awareness of The Selected Stores in Barangay Mercado, Boac, Marinduque On The Republic Act 10909 Otherwise Known As The No Short Changing ActDocument91 pagesLevel of Awareness of The Selected Stores in Barangay Mercado, Boac, Marinduque On The Republic Act 10909 Otherwise Known As The No Short Changing ActSchae Anne Motol100% (2)

- Thesis Format Bukidnon State UniversityDocument11 pagesThesis Format Bukidnon State UniversityNeil Geraldizo DagohoyNo ratings yet

- GTS Survey QuestionnaireDocument5 pagesGTS Survey Questionnairezaizai2192No ratings yet

- Word Doc With Capsu Header FooterDocument4 pagesWord Doc With Capsu Header FooterDan Christian VillacoNo ratings yet

- Narrative ReportDocument7 pagesNarrative ReportAnonymous QBf8WRPpXHNo ratings yet

- OJT DiaryDocument4 pagesOJT Diarybudo akoNo ratings yet

- Daily Time RecordDocument1 pageDaily Time RecordRonald JosephNo ratings yet

- Robert Smith: Service CrewDocument1 pageRobert Smith: Service CrewEricka Rivera SantosNo ratings yet

- Authorization Letter BIDocument1 pageAuthorization Letter BIKaguraNo ratings yet

- Strengths and Weaknesses of A Filipino CharacterDocument36 pagesStrengths and Weaknesses of A Filipino CharacterBryan BalaganNo ratings yet

- Technical Vocational and Livelihood Grade 12Document5 pagesTechnical Vocational and Livelihood Grade 12Jean ChristianNo ratings yet

- Local RRL.Document6 pagesLocal RRL.Denmar BalbonaNo ratings yet

- Tracer Study of Bsba Graduates of Psu by Us 2024Document21 pagesTracer Study of Bsba Graduates of Psu by Us 2024Bobby DabocNo ratings yet

- Principle Brief Description Keywords Quotation As A Prospective Teacher, I WillDocument3 pagesPrinciple Brief Description Keywords Quotation As A Prospective Teacher, I WillVanessa Mae NaveraNo ratings yet

- 200 HoursDocument5 pages200 HoursRegine Del Moro Arinaza0% (1)

- Recommendation Letter TemplateDocument2 pagesRecommendation Letter TemplateCharlyne Mari Flores100% (1)

- Assignment 2 - Normal DistributionDocument2 pagesAssignment 2 - Normal Distributionaldrin rex palacayNo ratings yet

- Security Systems Development Life CycleDocument3 pagesSecurity Systems Development Life Cyclenafis20100% (1)

- Survey Questionnaire On Alumni'S Involvement in School Activities, Projects, Placement Program and Their Perception To CJCDocument3 pagesSurvey Questionnaire On Alumni'S Involvement in School Activities, Projects, Placement Program and Their Perception To CJCAlexie CarvajalNo ratings yet

- MIL (Poem) A Bout Proper Usage of MediaDocument1 pageMIL (Poem) A Bout Proper Usage of MediaWitny LantanoNo ratings yet

- Electronics Repair Shop Business PlanDocument19 pagesElectronics Repair Shop Business PlanJP SacroNo ratings yet

- Syllabus OSH AutomotiveDocument6 pagesSyllabus OSH AutomotiveJonard MamaliasNo ratings yet

- Lesson 1 Assemble Computer HardwareDocument54 pagesLesson 1 Assemble Computer HardwareLeu NameNo ratings yet

- OJT Technical Report 2Document6 pagesOJT Technical Report 2alvin100% (1)

- St. Alexius College Flight SchoolDocument3 pagesSt. Alexius College Flight SchoolErick John Perez SinforosoNo ratings yet

- Solar Power Light Hat Survey Questionnaire REVISEDDocument6 pagesSolar Power Light Hat Survey Questionnaire REVISEDSharmaine OfalsaNo ratings yet

- 3Rd Graduate Research Colloquium Theme: R & D: Going Beyond LimitsDocument8 pages3Rd Graduate Research Colloquium Theme: R & D: Going Beyond LimitsBrian CunalNo ratings yet

- Session 8. CECILIA DEL CASTILLO - Innovations and InitiativesDocument38 pagesSession 8. CECILIA DEL CASTILLO - Innovations and InitiativesADBGADNo ratings yet

- On-The-Job-Training I Isu-Ilagan Auto Care Center City of Ilagan, IsabelaDocument36 pagesOn-The-Job-Training I Isu-Ilagan Auto Care Center City of Ilagan, IsabelaMaria Pina Barbado PonceNo ratings yet

- SCC HymnDocument1 pageSCC HymnCrystal Ann Monsale TadiamonNo ratings yet

- Problem 1.35Document8 pagesProblem 1.35zmm45x7sjtNo ratings yet

- We Create Stock Market ProfessionalsDocument12 pagesWe Create Stock Market Professionalsabhimani5472No ratings yet

- Sample 168 PDFDocument26 pagesSample 168 PDFabhimani5472No ratings yet

- Delisting Candidates111Document6 pagesDelisting Candidates111abhimani5472No ratings yet

- Topic: Finance For Non Finance Executives FACULTY: Mr. J N MamtoraDocument3 pagesTopic: Finance For Non Finance Executives FACULTY: Mr. J N Mamtoraabhimani5472No ratings yet

- Finance - For Non-Finance - ExecutivesDocument4 pagesFinance - For Non-Finance - Executivesabhimani5472No ratings yet

- Finance For Non-Finance Managers: SCDL: Obj Ect IveDocument5 pagesFinance For Non-Finance Managers: SCDL: Obj Ect Iveabhimani5472No ratings yet

- Accredited Finance For Non-Financial Managers: Chartered Management Institute'S SyllabusDocument2 pagesAccredited Finance For Non-Financial Managers: Chartered Management Institute'S Syllabusabhimani5472No ratings yet

- Finance For Non-Finance Personnel 2011Document4 pagesFinance For Non-Finance Personnel 2011abhimani5472No ratings yet

- Institute of Management Technology: Centre For Distance LearningDocument2 pagesInstitute of Management Technology: Centre For Distance Learningabhimani5472No ratings yet

- Finance Question PaperDocument2 pagesFinance Question Paperabhimani5472No ratings yet

- Ininstitute of Management Technology: Centre For Distance LearningDocument2 pagesIninstitute of Management Technology: Centre For Distance Learningabhimani5472No ratings yet

- Institute of Management Technology: Centre For Distance LearningDocument2 pagesInstitute of Management Technology: Centre For Distance Learningabhimani5472No ratings yet

- Institute of Management Technology: Centre For Distance LearningDocument1 pageInstitute of Management Technology: Centre For Distance Learningabhimani5472No ratings yet

- Institute of Management Technology: Centre For Distance LearningDocument2 pagesInstitute of Management Technology: Centre For Distance Learningabhimani5472No ratings yet

- Institute of Management Technology: Centre For Distance LearningDocument1 pageInstitute of Management Technology: Centre For Distance Learningabhimani5472No ratings yet

- Financial Planning - Dec 09Document2 pagesFinancial Planning - Dec 09abhimani5472No ratings yet

- International Finance - Dec 09Document1 pageInternational Finance - Dec 09abhimani5472No ratings yet

- Institute of Management Technology: Centre For Distance LearningDocument1 pageInstitute of Management Technology: Centre For Distance Learningabhimani5472No ratings yet

- Corporate Finance Practice QuestionsDocument11 pagesCorporate Finance Practice Questionsabhimani5472No ratings yet

- Haines C11-Ap-CDocument1 pageHaines C11-Ap-Capi-253587946No ratings yet

- Incubation List GujaratDocument18 pagesIncubation List GujaratT. A. NikitaNo ratings yet

- Social Banking Under NationalisationDocument8 pagesSocial Banking Under NationalisationLiya ShajanNo ratings yet

- Analysis of Pakistan's Cement IndustryDocument57 pagesAnalysis of Pakistan's Cement Industryhasananum100% (2)

- 2024 Mar 21Document7 pages2024 Mar 21Alejandro MufardiniNo ratings yet

- RBI Assistant Prelims Model Question Paper PDF (Set-2)Document33 pagesRBI Assistant Prelims Model Question Paper PDF (Set-2)Stephanie LucasNo ratings yet

- Ta Da Nitesh 01 Feb 2023 Format 1Document2 pagesTa Da Nitesh 01 Feb 2023 Format 1LAXMI courierNo ratings yet

- 3 Market Microstructure (Updated)Document18 pages3 Market Microstructure (Updated)alexxuf624No ratings yet

- 1st Essay Corporate Banking - Caitlynn Hans SetiabudiDocument10 pages1st Essay Corporate Banking - Caitlynn Hans SetiabudicaitlynnsetiabudiNo ratings yet

- Economist 30052019Document121 pagesEconomist 30052019Luis PereiraNo ratings yet

- Madrigal Azevedo/Karina MRS: 04 Mar 2023 11 Mar 2023 Trip To Cancun, MexicoDocument3 pagesMadrigal Azevedo/Karina MRS: 04 Mar 2023 11 Mar 2023 Trip To Cancun, MexicoGinna SofiaNo ratings yet

- Tax: Ot-2,/22-L2 No. T Challanno:: InvoiceDocument1 pageTax: Ot-2,/22-L2 No. T Challanno:: Invoiceomkar daveNo ratings yet

- Economic Policy: Theory And Practice 2nd Edition AgnèS BéNassy-QuéRé download pdfDocument51 pagesEconomic Policy: Theory And Practice 2nd Edition AgnèS BéNassy-QuéRé download pdfobjioarran88100% (2)

- ABC - Psr12 Question PaperDocument6 pagesABC - Psr12 Question PaperManav KhandelwalNo ratings yet

- Make Your Own Recycled BirdhouseDocument3 pagesMake Your Own Recycled BirdhouseKostasNo ratings yet

- ch17 2Document74 pagesch17 2albert cNo ratings yet

- M6 Assignment 1Document3 pagesM6 Assignment 1Lorraine CaliwanNo ratings yet

- Case Study: Lufthansa's Purchase of Boeing 737s: Analysis By: Rajan ThakurDocument16 pagesCase Study: Lufthansa's Purchase of Boeing 737s: Analysis By: Rajan ThakurRajanNo ratings yet

- Business Economics AssignmentDocument14 pagesBusiness Economics AssignmentShivankar sukulNo ratings yet

- Return KpisDocument5 pagesReturn KpisZuka KazalikashviliNo ratings yet

- Angel Broking: Our BusinessDocument4 pagesAngel Broking: Our BusinessHarish Kumar RNo ratings yet

- Full Airdrop Strategy by 0xmoeiDocument2 pagesFull Airdrop Strategy by 0xmoeiJavad AbbasifarNo ratings yet

- Irmaya Safitra - FR Session 1 Practice Assignment - Questions (8th July 2023)Document5 pagesIrmaya Safitra - FR Session 1 Practice Assignment - Questions (8th July 2023)irmaya.safitraNo ratings yet

- Easy Problem Chapter 5Document5 pagesEasy Problem Chapter 5Natally LangfeldtNo ratings yet

- Quiz1-2, Final (AST)Document37 pagesQuiz1-2, Final (AST)Kyla Mae MurphyNo ratings yet

- Argonne National Laboratory Electric Vehicle Battery Manufacturing ReportDocument58 pagesArgonne National Laboratory Electric Vehicle Battery Manufacturing ReportWWMTNo ratings yet

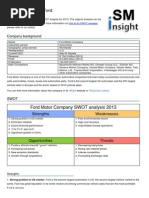

- Ford Swot AnalysisDocument3 pagesFord Swot AnalysisAnkur Anil Nahata100% (1)

- LBO (Leveraged Buyout) Model For Private Equity FirmsDocument2 pagesLBO (Leveraged Buyout) Model For Private Equity FirmsDishant KhanejaNo ratings yet

- EconomicsDocument10 pagesEconomicsFarheen KhanNo ratings yet