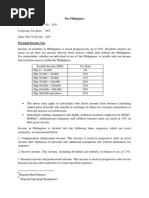

Canvas Activity 2

Canvas Activity 2

Download as docx, pdf, or txt

You might also like

- Villaroel vs. Estrada DigestDocument2 pagesVillaroel vs. Estrada DigestKattNo ratings yet

- Philippines Corporate Summary 1Document21 pagesPhilippines Corporate Summary 1BTS ArmyNo ratings yet

- Corporate Taxes in The PhilippinesDocument2 pagesCorporate Taxes in The PhilippinesAike SadjailNo ratings yet

- Lecture Notes - Atty Steve Part 1Document9 pagesLecture Notes - Atty Steve Part 1Tesia MandaloNo ratings yet

- Philippine Corporate TaxDocument3 pagesPhilippine Corporate TaxRaymond FaeldoñaNo ratings yet

- Philippines TaxDocument3 pagesPhilippines TaxerickjaoNo ratings yet

- Income From Foreign Currency TransactionsDocument2 pagesIncome From Foreign Currency TransactionsMeghan Kaye LiwenNo ratings yet

- Philippines Income Tax RatesDocument6 pagesPhilippines Income Tax RatesKristina AngelieNo ratings yet

- Lecture-Corporate-Income-Tax 2Document5 pagesLecture-Corporate-Income-Tax 2Ragelli Mae NatalarayNo ratings yet

- MODULE 6 PREFERENTIAL TAX RATES of CORPORATIONSDocument9 pagesMODULE 6 PREFERENTIAL TAX RATES of CORPORATIONSangclaire47No ratings yet

- Philippines Tax RatesDocument7 pagesPhilippines Tax RatesJL GEN0% (1)

- Philippines Tax RatesDocument7 pagesPhilippines Tax RatesRonel CacheroNo ratings yet

- Categories of Income and Tax RatesDocument5 pagesCategories of Income and Tax RatesRonel CacheroNo ratings yet

- Section 28 Create LawDocument26 pagesSection 28 Create LawsasanllidoalfredaNo ratings yet

- Tax On Corporation MaterialsDocument18 pagesTax On Corporation Materialsjdy managbanagNo ratings yet

- Bullet Notes 3 - Taxation of CorporationsDocument3 pagesBullet Notes 3 - Taxation of CorporationsDaisy ContinenteNo ratings yet

- Taxation in The PhilippinesDocument7 pagesTaxation in The Philippinesjohnamoc2No ratings yet

- CorporationsDocument5 pagesCorporationsathenaenchantraNo ratings yet

- Philippines 1Document12 pagesPhilippines 1Tegar AkiraNo ratings yet

- Income Taxation Finals - CompressDocument9 pagesIncome Taxation Finals - CompressElaiza RegaladoNo ratings yet

- Discussion Income TaxDocument7 pagesDiscussion Income TaxAljay LabugaNo ratings yet

- Discussion Income TaxDocument7 pagesDiscussion Income TaxAljay LabugaNo ratings yet

- Resident and Foreign CorporationDocument4 pagesResident and Foreign CorporationIris Grace Culata0% (1)

- Sec. 2 of The Corporation Code of The Philippines. Batas Blg. 68Document6 pagesSec. 2 of The Corporation Code of The Philippines. Batas Blg. 68jetotheloNo ratings yet

- 02 Corporate Income TaxDocument10 pages02 Corporate Income TaxbajujuNo ratings yet

- Vii. Tax On Corporations A. Domestic CorporationsDocument4 pagesVii. Tax On Corporations A. Domestic CorporationsRina TravelsNo ratings yet

- Domestic Corporations Not Subject To MCITDocument3 pagesDomestic Corporations Not Subject To MCITMeghan Kaye LiwenNo ratings yet

- TaxDocument26 pagesTaxParticia CorveraNo ratings yet

- Business Tax 1 LectureDocument4 pagesBusiness Tax 1 LectureJasmine LimNo ratings yet

- Classification of Taxes: A. Domestic CorporationDocument5 pagesClassification of Taxes: A. Domestic CorporationWenjunNo ratings yet

- Tax On Corporation - NotesDocument9 pagesTax On Corporation - NotesMervidelleNo ratings yet

- W11 Module 9 PPT Income Tax On CorporationsDocument32 pagesW11 Module 9 PPT Income Tax On Corporationscathleendfa13No ratings yet

- Legal M e M o R A N D U MDocument3 pagesLegal M e M o R A N D U MmyrahjNo ratings yet

- The Philippines Income TaxDocument8 pagesThe Philippines Income TaxmendozaivanrichmondNo ratings yet

- Business Tax Laws in The PhilippinesDocument12 pagesBusiness Tax Laws in The PhilippinesEthel Joi Manalac MendozaNo ratings yet

- Income Tax PresentationDocument22 pagesIncome Tax PresentationItchigo KorusakiNo ratings yet

- Tax On CorporationsDocument6 pagesTax On CorporationsJumen Gamaru TamayoNo ratings yet

- Sir Lectures Final TaxDocument12 pagesSir Lectures Final TaxCrystal KateNo ratings yet

- View in Online Reader: Text Size +-RecommendDocument7 pagesView in Online Reader: Text Size +-RecommendRhea Mae AmitNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document29 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Corporate Income TaxationDocument39 pagesCorporate Income TaxationVinz G. VizNo ratings yet

- TaxationDocument3 pagesTaxationPearl Jazmine M. MirandaNo ratings yet

- Income Taxes For CorporationsDocument35 pagesIncome Taxes For CorporationsKurt SoriaoNo ratings yet

- MCL - TAX.106 - Income Taxation of Individuals CorporationsDocument58 pagesMCL - TAX.106 - Income Taxation of Individuals CorporationsKim TividadNo ratings yet

- Income Tax On CorporationDocument4 pagesIncome Tax On CorporationNikolai DanielovichNo ratings yet

- Taxation of CorporationsDocument26 pagesTaxation of CorporationsjolinaNo ratings yet

- A Guide To Taxation in The PhilippinesDocument5 pagesA Guide To Taxation in The PhilippinesNathaniel MartinezNo ratings yet

- TAXATIONDocument31 pagesTAXATIONRocel DomingoNo ratings yet

- TAXATION TRUE OR FALSE TEST BANK - CorporationsDocument3 pagesTAXATION TRUE OR FALSE TEST BANK - CorporationsMagbanu Andrea JoneleNo ratings yet

- DTTL Tax Philippineshighlights 2019Document4 pagesDTTL Tax Philippineshighlights 2019Ivy BuentiempoNo ratings yet

- Income Tax On CorporationDocument54 pagesIncome Tax On CorporationJamielene Tan100% (1)

- TAXATIONDocument16 pagesTAXATIONcanolea94No ratings yet

- Faqs - Create LawDocument13 pagesFaqs - Create LawMichy De GuzmanNo ratings yet

- Changes Due To CREATE Law Corporate Income Tax (CIT) Reforms Under CREATE ActDocument7 pagesChanges Due To CREATE Law Corporate Income Tax (CIT) Reforms Under CREATE ActYietNo ratings yet

- HumRes TaxDocument3 pagesHumRes TaxJob Noel BernardoNo ratings yet

- Lecture 3 - Income Taxation (Corporate)Document8 pagesLecture 3 - Income Taxation (Corporate)Lovenia Magpatoc50% (2)

- Nonresident Citizen Philippines TaxationDocument5 pagesNonresident Citizen Philippines TaxationJM GapisaNo ratings yet

- Income Tax On CorporationDocument53 pagesIncome Tax On CorporationLyka Mae Palarca IrangNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- FOADocument257 pagesFOAjayavermamaNo ratings yet

- Lanbank vs. FastechDocument14 pagesLanbank vs. FastechDANICA ECHAGUENo ratings yet

- Chapter-4 - PROJECT EVALUATION AND ANALYSISDocument121 pagesChapter-4 - PROJECT EVALUATION AND ANALYSISnuhaminNo ratings yet

- Chapter 2 INTEREST RATE DETERMINATION AND STRUCTUREDocument1 pageChapter 2 INTEREST RATE DETERMINATION AND STRUCTUREBrandon LumibaoNo ratings yet

- CAPITAL STRUCTURE Ultratech 2018Document75 pagesCAPITAL STRUCTURE Ultratech 2018jeevanNo ratings yet

- DDM Model (Revised)Document5 pagesDDM Model (Revised)Tran UyenNo ratings yet

- Engineering Economics, Chapter 8Document23 pagesEngineering Economics, Chapter 8Bach Le NguyenNo ratings yet

- Cibn 2020 TimetableDocument1 pageCibn 2020 TimetableAromasodun Omobolanle IswatNo ratings yet

- Tender Misc 2011 12docDocument3 pagesTender Misc 2011 12dockamran_kngNo ratings yet

- Intermediate Accounting Vol.2 Chapter 22Document59 pagesIntermediate Accounting Vol.2 Chapter 22Ahmad Obaidat67% (3)

- Uncitral Model LawDocument3 pagesUncitral Model Lawyalini tholgappianNo ratings yet

- BPI v. Spouses Santiago GR No. 169116 28 March 2007 FactsDocument3 pagesBPI v. Spouses Santiago GR No. 169116 28 March 2007 FactsAleli BucuNo ratings yet

- Balance Sheet Owner's Equity Statemen T Income Stateme NT Statement of Cash FlowsDocument2 pagesBalance Sheet Owner's Equity Statemen T Income Stateme NT Statement of Cash FlowsSesmaNo ratings yet

- Skkc3343 Assignment 1-2019Document2 pagesSkkc3343 Assignment 1-2019Yi Wen Yap100% (1)

- Affidavit of ObligationDocument2 pagesAffidavit of Obligationsomebody991122No ratings yet

- Your Reservation: Ibis Bangkok SathornDocument3 pagesYour Reservation: Ibis Bangkok SathornBusyBoy PriyamNo ratings yet

- Tadepalligudem: Phone No:08818-220219Document2 pagesTadepalligudem: Phone No:08818-220219Surya thotaNo ratings yet

- Correction - Multiple Choice Questions On Micro FinanceDocument2 pagesCorrection - Multiple Choice Questions On Micro Financesushmanthqrewrer86% (21)

- 2307Document3 pages2307Anonymous yCFuth7BL80% (1)

- PNB Ze Lo Mastercard - App Form OnePager - Jan2020 1Document9 pagesPNB Ze Lo Mastercard - App Form OnePager - Jan2020 1Crypto ManiacNo ratings yet

- CHATIME Franchise Application FormDocument6 pagesCHATIME Franchise Application Formvpolanit1576No ratings yet

- Muthoot Finance Ltd.Document8 pagesMuthoot Finance Ltd.Hrithik Saxena100% (1)

- Group Members Muskan Ayesha Hameed Rabita Qayoom Anum KhanDocument17 pagesGroup Members Muskan Ayesha Hameed Rabita Qayoom Anum KhanRabita QayoomNo ratings yet

- Rem145r8 MDocument3 pagesRem145r8 MBrijesh Pratap SinghNo ratings yet

- Chapter 3 BOND VALUATIONDocument2 pagesChapter 3 BOND VALUATIONBrandon LumibaoNo ratings yet

- The Microfinance Industry in IndiaDocument3 pagesThe Microfinance Industry in IndiaPrashant Upashi SonuNo ratings yet

- Chapter-1: Introduction of Merchant BankingDocument47 pagesChapter-1: Introduction of Merchant BankingKritika IyerNo ratings yet

- Orchid Hotel-An IntroductionDocument1 pageOrchid Hotel-An IntroductionSai VasudevanNo ratings yet

- Unit 7 E-Tutor PresentationDocument18 pagesUnit 7 E-Tutor PresentationKatrina EustaceNo ratings yet