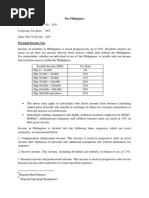

Categories of Income and Tax Rates

Categories of Income and Tax Rates

Download as docx, pdf, or txt

You might also like

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4.5 out of 5 stars4.5/5 (6)

- Clinical Evaluation Report SampleDocument12 pagesClinical Evaluation Report Sampleibrahim kademogluNo ratings yet

- Utility Requirements, Project Scheduling, & Total Project CostsDocument8 pagesUtility Requirements, Project Scheduling, & Total Project CostsRonel CacheroNo ratings yet

- TVL Animation q1 m2Document13 pagesTVL Animation q1 m2Jayson Paul Dalisay DatinguinooNo ratings yet

- ST Joseph of CupertinoDocument1 pageST Joseph of CupertinoJNMGNo ratings yet

- Philippines Tax RatesDocument7 pagesPhilippines Tax RatesRonel CacheroNo ratings yet

- Philippines Income Tax RatesDocument6 pagesPhilippines Income Tax RatesKristina AngelieNo ratings yet

- Philippines Tax RatesDocument7 pagesPhilippines Tax RatesJL GEN0% (1)

- Philippines 1Document12 pagesPhilippines 1Tegar AkiraNo ratings yet

- Philippines TaxDocument3 pagesPhilippines TaxerickjaoNo ratings yet

- Corporate Taxes in The PhilippinesDocument2 pagesCorporate Taxes in The PhilippinesAike SadjailNo ratings yet

- Tax On CorporationsDocument6 pagesTax On CorporationsJumen Gamaru TamayoNo ratings yet

- Lecture Notes - Atty Steve Part 1Document9 pagesLecture Notes - Atty Steve Part 1Tesia MandaloNo ratings yet

- View in Online Reader: Text Size +-RecommendDocument7 pagesView in Online Reader: Text Size +-RecommendRhea Mae AmitNo ratings yet

- The Philippines Income TaxDocument8 pagesThe Philippines Income TaxmendozaivanrichmondNo ratings yet

- Taxation in The PhilippinesDocument7 pagesTaxation in The Philippinesjohnamoc2No ratings yet

- Business Tax Laws in The PhilippinesDocument12 pagesBusiness Tax Laws in The PhilippinesEthel Joi Manalac MendozaNo ratings yet

- Income Taxation Finals - CompressDocument9 pagesIncome Taxation Finals - CompressElaiza RegaladoNo ratings yet

- JWLSG Tax 1Document2 pagesJWLSG Tax 1Guevarra AngeloNo ratings yet

- Philippine Corporate TaxDocument3 pagesPhilippine Corporate TaxRaymond FaeldoñaNo ratings yet

- Canvas Activity 2Document10 pagesCanvas Activity 2Micol VillaflorNo ratings yet

- TaxationDocument3 pagesTaxationErwin MacaspacNo ratings yet

- Income Tax and Ethiopia Tax SystemDocument9 pagesIncome Tax and Ethiopia Tax Systemayele asefaNo ratings yet

- Corporate Income TaxationDocument39 pagesCorporate Income TaxationVinz G. VizNo ratings yet

- DTTL Tax Philippineshighlights 2019Document4 pagesDTTL Tax Philippineshighlights 2019Ivy BuentiempoNo ratings yet

- Tax Rates Table NaizaDocument11 pagesTax Rates Table NaizaBINAYAO NAIZA MAENo ratings yet

- 3 Income Tax ConceptsDocument37 pages3 Income Tax ConceptsRommel Espinocilla Jr.No ratings yet

- Income TaxationDocument32 pagesIncome TaxationkarlNo ratings yet

- Income Tax On Individuals Part 2Document22 pagesIncome Tax On Individuals Part 2mmhNo ratings yet

- TAXATIONDocument16 pagesTAXATIONcanolea94No ratings yet

- Income Tax PanamaDocument106 pagesIncome Tax PanamaScribdTranslationsNo ratings yet

- 02 Corporate Income TaxDocument10 pages02 Corporate Income TaxbajujuNo ratings yet

- Doing Business Brazil Deloitte Corporate Taxation Indirect TaxesDocument18 pagesDoing Business Brazil Deloitte Corporate Taxation Indirect TaxesGiulia CamposNo ratings yet

- Different Kinds of Taxes in The PhilippinesDocument4 pagesDifferent Kinds of Taxes in The PhilippinesJUDADRIEL MADRIDANONo ratings yet

- A Guide To Taxation in The PhilippinesDocument5 pagesA Guide To Taxation in The PhilippinesNathaniel MartinezNo ratings yet

- Taxes That Affect ForeignersDocument4 pagesTaxes That Affect ForeignersasiajcvrNo ratings yet

- tAX LESSON B .Document10 pagestAX LESSON B .intramuramazingNo ratings yet

- The Philippines TaxesDocument3 pagesThe Philippines TaxesPearl Jazmine M. MirandaNo ratings yet

- Tax Nirc Sec 27 - 31Document8 pagesTax Nirc Sec 27 - 31Loren MandaNo ratings yet

- International Tax: Philippines Highlights 2017Document4 pagesInternational Tax: Philippines Highlights 2017Tony MorganNo ratings yet

- Axsdaqgasdgasdg 123123 Aeasdfw SadgDocument6 pagesAxsdaqgasdgasdg 123123 Aeasdfw SadgMark LimNo ratings yet

- Bullet Notes 3 - Taxation of CorporationsDocument3 pagesBullet Notes 3 - Taxation of CorporationsDaisy ContinenteNo ratings yet

- TAXATION TRUE OR FALSE TEST BANK - CorporationsDocument3 pagesTAXATION TRUE OR FALSE TEST BANK - CorporationsMagbanu Andrea JoneleNo ratings yet

- 3.2 Business Profit TaxDocument49 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- NT - Items of Gross Income 0510 - Income TaxDocument7 pagesNT - Items of Gross Income 0510 - Income TaxElizah PorcadoNo ratings yet

- Taxation Reviewer 2022Document2 pagesTaxation Reviewer 2022Saclao John Mark GalangNo ratings yet

- TRUE OR FALSE (p.179,180)Document2 pagesTRUE OR FALSE (p.179,180)Aberin GalenzogaNo ratings yet

- FABM2 Week 12 13 AsynchDocument8 pagesFABM2 Week 12 13 AsynchKhaira PeraltaNo ratings yet

- Income TaxDocument32 pagesIncome TaxAeiaNo ratings yet

- Who Are Required To Pay Income Tax in The Philippines? (Section 23 of The National Internal Revenue Code (NIRC) of 1997)Document3 pagesWho Are Required To Pay Income Tax in The Philippines? (Section 23 of The National Internal Revenue Code (NIRC) of 1997)Kristine Ann CarandangNo ratings yet

- Corporate TaxesDocument6 pagesCorporate TaxesfranNo ratings yet

- Income TaxationDocument3 pagesIncome Taxationm.bagnas.488669No ratings yet

- MODULE 6 PREFERENTIAL TAX RATES of CORPORATIONSDocument9 pagesMODULE 6 PREFERENTIAL TAX RATES of CORPORATIONSangclaire47No ratings yet

- Classification of Taxes: A. Domestic CorporationDocument5 pagesClassification of Taxes: A. Domestic CorporationWenjunNo ratings yet

- Income and Business TaxationDocument8 pagesIncome and Business TaxationAs AsNo ratings yet

- Philippines Corporate Summary 1Document21 pagesPhilippines Corporate Summary 1BTS ArmyNo ratings yet

- Taxation Structure in PakistanDocument8 pagesTaxation Structure in PakistanIkra MalikNo ratings yet

- Guinea Tax 2Document6 pagesGuinea Tax 2Onur KopanNo ratings yet

- TAX by MamalateoDocument38 pagesTAX by MamalateoTheresa Montales0% (1)

- Module 1: Income Tax PrinciplesDocument18 pagesModule 1: Income Tax PrinciplesJun MagallonNo ratings yet

- Highlights of The CREATE LawDocument3 pagesHighlights of The CREATE LawChristine Rufher FajotaNo ratings yet

- Corporation As A TaxpayerDocument27 pagesCorporation As A TaxpayerBSA-2C John Dominic Mia100% (1)

- 1040 Exam Prep - Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep - Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- Polytechnic University of The Philippines College of AccountancyDocument11 pagesPolytechnic University of The Philippines College of AccountancyRonel CacheroNo ratings yet

- Good Governance and Corporate Social Responsibility: Peter DruckerDocument6 pagesGood Governance and Corporate Social Responsibility: Peter DruckerRonel CacheroNo ratings yet

- Financial Markets: Financial Market Is A Place Where Individuals and Organizations Wanting To Borrow Funds AreDocument2 pagesFinancial Markets: Financial Market Is A Place Where Individuals and Organizations Wanting To Borrow Funds AreRonel CacheroNo ratings yet

- Cost On A Short-Run Fixed Cost, Variable Cost and Total CostDocument1 pageCost On A Short-Run Fixed Cost, Variable Cost and Total CostRonel CacheroNo ratings yet

- Property Rights: Economics - Ronel E. CacheroDocument1 pageProperty Rights: Economics - Ronel E. CacheroRonel CacheroNo ratings yet

- 3 Process and Capacity DesignDocument3 pages3 Process and Capacity DesignRonel Cachero100% (2)

- 8.4 Selecting What To Benchmark - 8.5 Understanding Present Performance Selecting What To BenchmarkDocument2 pages8.4 Selecting What To Benchmark - 8.5 Understanding Present Performance Selecting What To BenchmarkRonel CacheroNo ratings yet

- An Introduction To Dispute ResolutionDocument21 pagesAn Introduction To Dispute ResolutionDilan De Silva100% (3)

- Philippine Coconut Produccers Federation vs. RepublicDocument8 pagesPhilippine Coconut Produccers Federation vs. RepublicJaneKarlaCansanaNo ratings yet

- MAN Energy Compressors To Support Carbon Capture in NetherlandsDocument2 pagesMAN Energy Compressors To Support Carbon Capture in Netherlandsli xianNo ratings yet

- Design of A High Speed Rail Arch Bridge Over The Alcántara Reservoir (Spain)Document8 pagesDesign of A High Speed Rail Arch Bridge Over The Alcántara Reservoir (Spain)cocodrilopopNo ratings yet

- PO CSIR CIMFR DhanbadDocument2 pagesPO CSIR CIMFR DhanbadB.C. C.L.No ratings yet

- RFP For Endpoint Email and Web SecurityDocument69 pagesRFP For Endpoint Email and Web SecurityDinesh GaikwadNo ratings yet

- Fletcher - Ohio Highway Patrol ReportDocument29 pagesFletcher - Ohio Highway Patrol ReportThe Columbus DispatchNo ratings yet

- Food Is What People and Animals Eat To SurviveDocument3 pagesFood Is What People and Animals Eat To SurviveNatasha HamiltonNo ratings yet

- Ucc Foreclosure Slide ShowDocument60 pagesUcc Foreclosure Slide ShowTHEYDONTWIN100% (3)

- Saudi Cement Industry - A Fundamental AnalysisDocument16 pagesSaudi Cement Industry - A Fundamental AnalysisHarshit SinghNo ratings yet

- Lisa Kleypas BooksDocument6 pagesLisa Kleypas BooksAna-Maria ŢurcanuNo ratings yet

- For Career Talk PDFDocument3 pagesFor Career Talk PDFKenette Diane CantubaNo ratings yet

- How "Good Design" Failed Us - The New YorkerDocument4 pagesHow "Good Design" Failed Us - The New YorkerPenélope PlazaNo ratings yet

- 2014-15 Douglas County Secured Assessment RollDocument97 pages2014-15 Douglas County Secured Assessment RollcvalleytimesNo ratings yet

- Adjudication Manual: (Fourth Edition)Document80 pagesAdjudication Manual: (Fourth Edition)Khukan Das100% (1)

- Vocabluary Intermediate4 PDFDocument3 pagesVocabluary Intermediate4 PDFOlga KohnoNo ratings yet

- 3 - Cash Larceny 2015Document28 pages3 - Cash Larceny 2015Mel LissaNo ratings yet

- Village Kurwa BackgroundDocument7 pagesVillage Kurwa BackgroundDeependra NigamNo ratings yet

- Days of The WeekDocument1 pageDays of The WeekNatalia Nogueira BasaloNo ratings yet

- Second Term Test A Reading Comprehension: Read The Text Carefully and Answer The QuestionsDocument3 pagesSecond Term Test A Reading Comprehension: Read The Text Carefully and Answer The QuestionsChahida GraciasNo ratings yet

- Ethics Lesson 9Document3 pagesEthics Lesson 9adsaster201No ratings yet

- List of AdverbsDocument1 pageList of Adverbsapi-233625001No ratings yet

- Chapter 2 Digital Business ModelsDocument45 pagesChapter 2 Digital Business ModelsYaY CoverNo ratings yet

- Shakti Mishra - CVDocument1 pageShakti Mishra - CVchamp.jaisNo ratings yet

- Fmod LicenseDocument1 pageFmod LicenseMicu Constantin-SebastianNo ratings yet

- S T S - Group-ScienceDocument4 pagesS T S - Group-ScienceEmmanuel PaladaNo ratings yet

- UntitledDocument33 pagesUntitledhimanshu143goel0% (1)