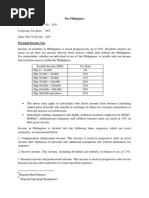

Corporate Taxes

Corporate Taxes

Download as docx, pdf, or txt

You might also like

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4.5 out of 5 stars4.5/5 (6)

- 1555746455PRIYA GAUR - Offer Letter - 20190420 - 131706Document4 pages1555746455PRIYA GAUR - Offer Letter - 20190420 - 131706Priya Gaur33% (3)

- View in Online Reader: Text Size +-RecommendDocument7 pagesView in Online Reader: Text Size +-RecommendRhea Mae AmitNo ratings yet

- Business Tax Laws in The PhilippinesDocument12 pagesBusiness Tax Laws in The PhilippinesEthel Joi Manalac MendozaNo ratings yet

- Philippines TaxDocument3 pagesPhilippines TaxerickjaoNo ratings yet

- Philippines 1Document12 pagesPhilippines 1Tegar AkiraNo ratings yet

- 02 Corporate Income TaxDocument10 pages02 Corporate Income TaxbajujuNo ratings yet

- Taxation and Fiscal RegulationsDocument9 pagesTaxation and Fiscal RegulationsAparna SinghNo ratings yet

- The Philippines Income TaxDocument8 pagesThe Philippines Income TaxmendozaivanrichmondNo ratings yet

- Tax Module 01Document7 pagesTax Module 01ktchiu29No ratings yet

- Categories of Income and Tax RatesDocument5 pagesCategories of Income and Tax RatesRonel CacheroNo ratings yet

- Philippines Tax RatesDocument7 pagesPhilippines Tax RatesRonel CacheroNo ratings yet

- Taxation in The PhilippinesDocument7 pagesTaxation in The Philippinesjohnamoc2No ratings yet

- Lecture Notes - Atty Steve Part 1Document9 pagesLecture Notes - Atty Steve Part 1Tesia MandaloNo ratings yet

- Taxation ProjectDocument14 pagesTaxation ProjectrahulkoduvanNo ratings yet

- Philippines Tax RatesDocument7 pagesPhilippines Tax RatesJL GEN0% (1)

- TAXES - HandoutDocument2 pagesTAXES - HandoutYzah CariagaNo ratings yet

- Taxation of CorporationsDocument78 pagesTaxation of CorporationsGlory Mhay67% (12)

- Philippines Income Tax RatesDocument6 pagesPhilippines Income Tax RatesKristina AngelieNo ratings yet

- TaxationDocument3 pagesTaxationErwin MacaspacNo ratings yet

- KPMG - Indonesian TaxDocument13 pagesKPMG - Indonesian Taxbang bebetNo ratings yet

- Guinea Tax 2Document6 pagesGuinea Tax 2Onur KopanNo ratings yet

- MBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 1Document23 pagesMBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 1Jesse Rielle CarasNo ratings yet

- Tax Reform For Acceleration and Inclusion LawDocument28 pagesTax Reform For Acceleration and Inclusion LawGloriosa SzeNo ratings yet

- A Guide To Taxation in The PhilippinesDocument5 pagesA Guide To Taxation in The PhilippinesNathaniel MartinezNo ratings yet

- Tax Types and RatesDocument9 pagesTax Types and Ratesattah4789No ratings yet

- TAXATIONDocument4 pagesTAXATIONkryshaacedoNo ratings yet

- Gambia Tax Guide 2016 17Document11 pagesGambia Tax Guide 2016 17joebeqNo ratings yet

- Percentage TaxDocument4 pagesPercentage TaxPATRICK JAMES BALOGBOG ROSARIONo ratings yet

- TaxDocument26 pagesTaxParticia CorveraNo ratings yet

- Taxation in The PhilippinesDocument54 pagesTaxation in The PhilippinesChristine Angela LigutomNo ratings yet

- Investing in Africa Angola: Page - 1Document9 pagesInvesting in Africa Angola: Page - 1odongochrisNo ratings yet

- Inward 22Document44 pagesInward 22CSBNo ratings yet

- Other Local TaxesDocument25 pagesOther Local Taxesjoankristel19lNo ratings yet

- HumRes TaxDocument3 pagesHumRes TaxJob Noel BernardoNo ratings yet

- Corporation As A TaxpayerDocument27 pagesCorporation As A TaxpayerBSA-2C John Dominic Mia100% (1)

- 3 Income Tax ConceptsDocument37 pages3 Income Tax ConceptsRommel Espinocilla Jr.No ratings yet

- Classification of Taxes: A. Domestic CorporationDocument5 pagesClassification of Taxes: A. Domestic CorporationWenjunNo ratings yet

- Perpajakan SingapurDocument22 pagesPerpajakan SingapurDio PatraNo ratings yet

- Tax StructureDocument23 pagesTax StructureAsif Rasool ChannaNo ratings yet

- Philippine TaxationDocument7 pagesPhilippine TaxationJayson Aquino SantiagoNo ratings yet

- Canvas Activity 2Document10 pagesCanvas Activity 2Micol VillaflorNo ratings yet

- Create Act: Corporate Recovery & Tax Incentives For EnterprisesDocument6 pagesCreate Act: Corporate Recovery & Tax Incentives For EnterprisesDanica RamosNo ratings yet

- 3.2 Business Profit TaxDocument49 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- Legal M e M o R A N D U MDocument3 pagesLegal M e M o R A N D U MmyrahjNo ratings yet

- Sri Lanka 2018 PDFDocument24 pagesSri Lanka 2018 PDFSoofi AthamNo ratings yet

- Income Taxation in The PhilippinesDocument4 pagesIncome Taxation in The PhilippinesjenxxacadsNo ratings yet

- Corporate Income Taxes and Tax RatesDocument38 pagesCorporate Income Taxes and Tax RatesShaheen ShahNo ratings yet

- Philippine TaxationDocument2 pagesPhilippine TaxationeyyosunshineeNo ratings yet

- Income Tax Table - NIRCDocument6 pagesIncome Tax Table - NIRCgoateneo1bigfightNo ratings yet

- Module 1: Income Tax PrinciplesDocument18 pagesModule 1: Income Tax PrinciplesJun MagallonNo ratings yet

- Income Taxation Finals - CompressDocument9 pagesIncome Taxation Finals - CompressElaiza RegaladoNo ratings yet

- Philippines Corporate Summary 1Document21 pagesPhilippines Corporate Summary 1BTS ArmyNo ratings yet

- Business TaxationDocument10 pagesBusiness TaxationImman AgdonNo ratings yet

- Tax On Corporation MaterialsDocument18 pagesTax On Corporation Materialsjdy managbanagNo ratings yet

- Taxation of CorporationsDocument26 pagesTaxation of CorporationsjolinaNo ratings yet

- Tax On Corporation - NotesDocument9 pagesTax On Corporation - NotesMervidelleNo ratings yet

- Types of Taxes in The PhilippinesDocument4 pagesTypes of Taxes in The PhilippinesRieva Jean Pacina100% (1)

- Some Digested CasesDocument23 pagesSome Digested CasesfranNo ratings yet

- Brain Tumor FactsDocument1 pageBrain Tumor FactsfranNo ratings yet

- Rumbaua v. Rumbaua, G.R. No. 166738Document1 pageRumbaua v. Rumbaua, G.R. No. 166738franNo ratings yet

- Admissibility: Dui/Dwi Wet Reckless Driving Bad CheckDocument2 pagesAdmissibility: Dui/Dwi Wet Reckless Driving Bad CheckfranNo ratings yet

- 3 Soldiers KilledDocument2 pages3 Soldiers KilledfranNo ratings yet

- 7 NPAs Killed in MT ProvDocument1 page7 NPAs Killed in MT ProvfranNo ratings yet

- The Seven Natural Wonders of The PhilippinesDocument8 pagesThe Seven Natural Wonders of The PhilippinesfranNo ratings yet

- Bc Technology Group Limited BC 科 技 集 團 有 限 公 司: Placing Of New Shares Under General MandateDocument10 pagesBc Technology Group Limited BC 科 技 集 團 有 限 公 司: Placing Of New Shares Under General MandateForkLogNo ratings yet

- PT Global Kapital Investama BerjangkaDocument66 pagesPT Global Kapital Investama BerjangkajhonxracNo ratings yet

- BAI TradeFinance AllDocument27 pagesBAI TradeFinance AllRajatNo ratings yet

- Documentary Stamp TaxDocument2 pagesDocumentary Stamp TaxJoAnne Yaptinchay ClaudioNo ratings yet

- Executive SummaryDocument41 pagesExecutive SummaryArchana SinghNo ratings yet

- Financing Options in The Oil and Gas IndustryDocument31 pagesFinancing Options in The Oil and Gas IndustryRuna JullyNo ratings yet

- Contract Terms - Hotel TurnkeyDocument5 pagesContract Terms - Hotel TurnkeySunil KatariaNo ratings yet

- Undertaking To Change Corporate NameDocument1 pageUndertaking To Change Corporate NameMeynard MagsinoNo ratings yet

- Depository SystemDocument38 pagesDepository SystemNavin RaoNo ratings yet

- Branch Inward Stamp & Authorised Signatory With Stamp CPU Inward Stamp & Authorised Signatory With StampDocument12 pagesBranch Inward Stamp & Authorised Signatory With Stamp CPU Inward Stamp & Authorised Signatory With Stampgoutham LNo ratings yet

- PreferenceSharesDocument1 pagePreferenceSharesTiso Blackstar GroupNo ratings yet

- As ISO 10002-2006 Customer Satisfaction - Guidelines For Complaints Handling in Organizations (ISO 10002-2004Document10 pagesAs ISO 10002-2006 Customer Satisfaction - Guidelines For Complaints Handling in Organizations (ISO 10002-2004SAI Global - APAC0% (2)

- R Fong PaulDocument9 pagesR Fong PaulCalWonkNo ratings yet

- Ratio Analysis of WiproDocument7 pagesRatio Analysis of Wiprosandeepl4720% (2)

- Affidavit in Support of Summons-Affidavits-Affidavits Under Companies Act ADocument2 pagesAffidavit in Support of Summons-Affidavits-Affidavits Under Companies Act ACDRSNo ratings yet

- Written MATH SolutionDocument10 pagesWritten MATH SolutionUttam GolderNo ratings yet

- Oil and Gas Asset Backed SecuritizationsDocument9 pagesOil and Gas Asset Backed SecuritizationsCDNo ratings yet

- Bank Alpha Inventory Aaa Rated 15 Year Zero Coupon Bonds Fac Chapter 15 Problem 9qp Solution 9781259717772 ExcDocument1 pageBank Alpha Inventory Aaa Rated 15 Year Zero Coupon Bonds Fac Chapter 15 Problem 9qp Solution 9781259717772 ExcArihant patilNo ratings yet

- Sales InvoiceDocument4 pagesSales InvoiceMakoderohNo ratings yet

- FIN 400 Course SylDocument4 pagesFIN 400 Course SylShebelle ColoradoNo ratings yet

- Position PaperDocument7 pagesPosition Papermarian_kris_bayona_santos100% (1)

- Letter of Offer Clean Version PDFDocument52 pagesLetter of Offer Clean Version PDFCreddy Pradeep BNo ratings yet

- Shareholder Activism India 130090Document22 pagesShareholder Activism India 130090Snehil AdityaNo ratings yet

- 2019 Li Mock B-Am-Solutions PDFDocument62 pages2019 Li Mock B-Am-Solutions PDFLucky Sky100% (2)

- Chap 8 Lecture NoteDocument4 pagesChap 8 Lecture NoteCloudSpireNo ratings yet

- KK 2 Years Itr and CoiDocument71 pagesKK 2 Years Itr and Coisunil jadhavNo ratings yet

- Understanding The Drivers of ReturnsDocument2 pagesUnderstanding The Drivers of ReturnsSamir JainNo ratings yet

- Bba 402 PDFDocument2 pagesBba 402 PDFarmaanNo ratings yet

- GoldDocument25 pagesGoldarun1417100% (1)